dYdX策略设计范例

应不少用户需求,最近FMZ平台支持了dYdX这个去中心化交易所。有策略的小伙伴们可以愉快的挖矿dYdX了。正好很久以前就想写一个随机交易策略,赚钱亏钱无所谓目的是练练手顺便教学一下策略设计。所以接下来我们一起来设计一个随机交易所策略,策略绩效好坏不用在意,我们权且来学习策略设计。

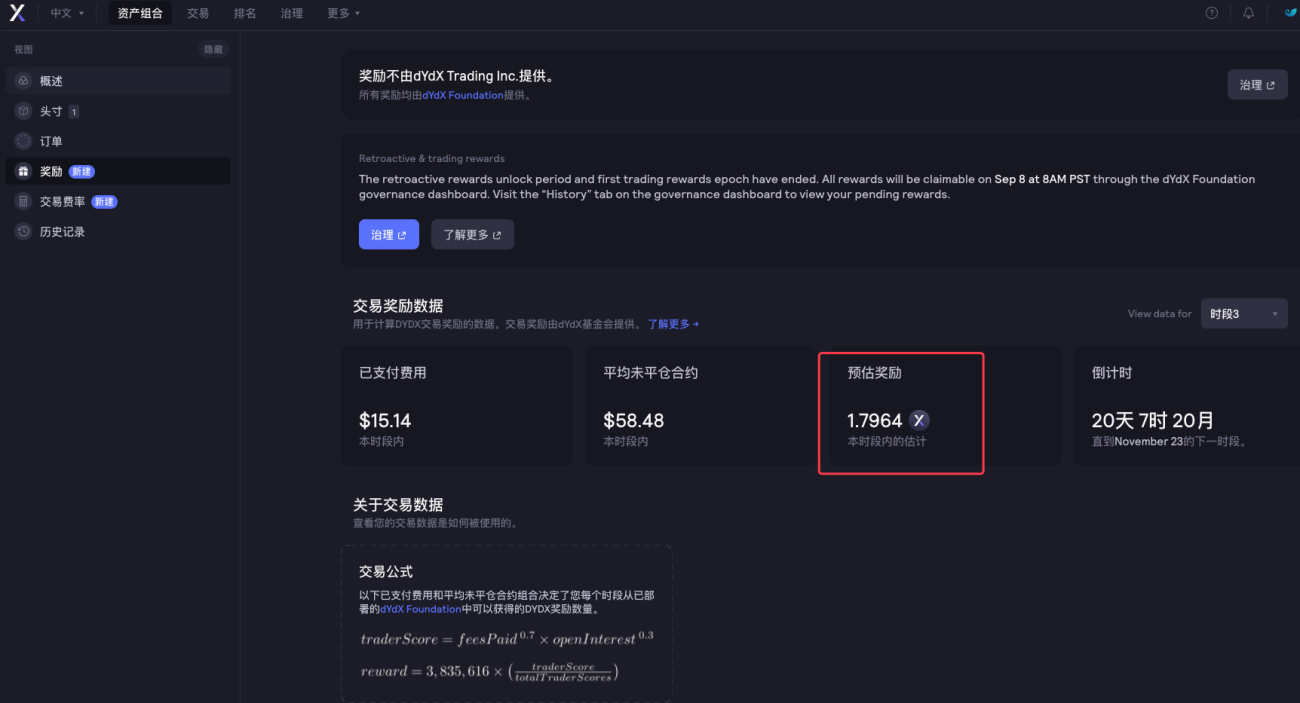

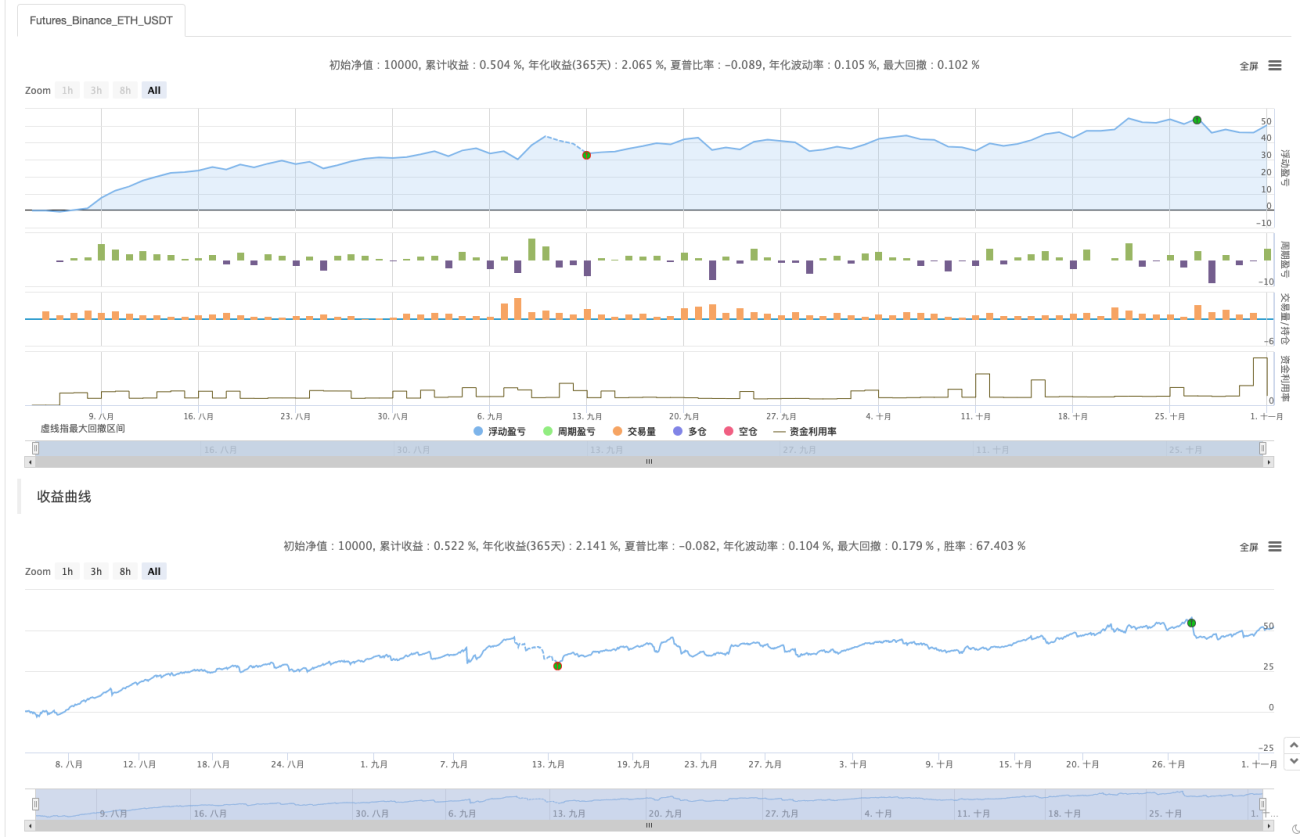

先来晒一波挖矿

本篇的策略挖矿截图。

有好的挖矿策略思路的小伙伴也欢迎留言哇!

随机交易策略设计

我们来“胡思乱想”一通!计划设计一个不看指标、不看价格随机下单的策略,下单无非就是做多、做空而已,堵的都是概率。那我们就用随机数1~100来确定多空。

做多条件:随机数1~50。

做空条件:随机数51~100。

多空都是50个数。接下来我们来思考下如何平仓,既然是赌那么就必须要有个输赢标准。那么在交易中我们就设定固定止盈、止损来作为输赢标准吧。止盈了就是赢,止损了就是输。至于这个止盈止损多少合适,这个其实就是影响盈亏比了,哦对!还影响胜率!(这样设计策略有效么?能保证是个正向的数学期望么?先干了再说!反正是学习、研究!)

交易并不是无成本的,有滑点、手续费等因素足以把我们的随机交易胜率拉向小于50%那一边了。想到这里继续怎么设计呢?

不如设计个倍数加仓吧,既然是赌那么连续10次8次随机交易都输的概率应该不会很大。所以我想设计第一笔交易下单量很小,能多小就多小。然后如果赌输了,就增加下单量继续随机下单。

OK了,策略就设计这么简单就行了。

设计源码:

var openPrice = 0

var ratio = 1

var totalEq = null

var nowEq = null

function cancelAll() {

while (1) {

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

break

}

for (var i = 0 ; i < orders.length ; i++) {

exchange.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

Sleep(500)

}

}

function main() {

if (isReset) {

_G(null)

LogReset(1)

LogProfitReset()

LogVacuum()

Log("重置所有数据", "#FF0000")

}

exchange.SetContractType(ct)

var initPos = _C(exchange.GetPosition)

if (initPos.length != 0) {

throw "策略启动时有持仓!"

}

exchange.SetPrecision(pricePrecision, amountPrecision)

Log("设置精度", pricePrecision, amountPrecision)

if (!IsVirtual()) {

var recoverTotalEq = _G("totalEq")

if (!recoverTotalEq) {

var currTotalEq = _C(exchange.GetAccount).Balance // equity

if (currTotalEq) {

totalEq = currTotalEq

_G("totalEq", currTotalEq)

} else {

throw "获取初始权益失败"

}

} else {

totalEq = recoverTotalEq

}

} else {

totalEq = _C(exchange.GetAccount).Balance

}

while (1) {

if (openPrice == 0) {

// 更新账户信息,计算收益

var nowAcc = _C(exchange.GetAccount)

nowEq = IsVirtual() ? nowAcc.Balance : nowAcc.Balance // equity

LogProfit(nowEq - totalEq, nowAcc)

var direction = Math.floor((Math.random()*100)+1) // 1~50 , 51~100

var depth = _C(exchange.GetDepth)

if (depth.Asks.length <= 2 || depth.Bids.length <= 2) {

Sleep(1000)

continue

}

if (direction > 50) {

// long

openPrice = depth.Bids[1].Price

exchange.SetDirection("buy")

exchange.Buy(Math.abs(openPrice) + slidePrice, amount * ratio)

} else {

// short

openPrice = -depth.Asks[1].Price

exchange.SetDirection("sell")

exchange.Sell(Math.abs(openPrice) - slidePrice, amount * ratio)

}

Log("下", direction > 50 ? "买单" : "卖单", ",价格:", Math.abs(openPrice))

continue

}

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

var pos = _C(exchange.GetPosition)

if (pos.length == 0) {

openPrice = 0

continue

}

// 平仓检测

while (1) {

var depth = _C(exchange.GetDepth)

if (depth.Asks.length <= 2 || depth.Bids.length <= 2) {

Sleep(1000)

continue

}

var stopLossPrice = openPrice > 0 ? Math.abs(openPrice) - stopLoss : Math.abs(openPrice) + stopLoss

var stopProfitPrice = openPrice > 0 ? Math.abs(openPrice) + stopProfit : Math.abs(openPrice) - stopProfit

var winOrLoss = 0 // 1 win , -1 loss

// 画线

$.PlotLine("bid", depth.Bids[0].Price)

$.PlotLine("ask", depth.Asks[0].Price)

// 止损

if (openPrice > 0 && depth.Bids[0].Price < stopLossPrice) {

exchange.SetDirection("closebuy")

exchange.Sell(depth.Bids[0].Price - slidePrice, pos[0].Amount)

winOrLoss = -1

} else if (openPrice < 0 && depth.Asks[0].Price > stopLossPrice) {

exchange.SetDirection("closesell")

exchange.Buy(depth.Asks[0].Price + slidePrice, pos[0].Amount)

winOrLoss = -1

}

// 止盈

if (openPrice > 0 && depth.Bids[0].Price > stopProfitPrice) {

exchange.SetDirection("closebuy")

exchange.Sell(depth.Bids[0].Price - slidePrice, pos[0].Amount)

winOrLoss = 1

} else if (openPrice < 0 && depth.Asks[0].Price < stopProfitPrice) {

exchange.SetDirection("closesell")

exchange.Buy(depth.Asks[0].Price + slidePrice, pos[0].Amount)

winOrLoss = 1

}

// 检测挂单

Sleep(2000)

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

pos = _C(exchange.GetPosition)

if (pos.length == 0) {

if (winOrLoss == -1) {

ratio++

} else if (winOrLoss == 1) {

ratio = 1

}

break

}

} else {

// 撤销挂单

cancelAll()

Sleep(2000)

pos = _C(exchange.GetPosition)

// 撤销后更新持仓,需要再次检查

if (pos.length == 0) {

if (winOrLoss == -1) {

ratio++

} else if (winOrLoss == 1) {

ratio = 1

}

break

}

}

var tbl = {

"type" : "table",

"title" : "info",

"cols" : ["totalEq", "nowEq", "openPrice", "bid1Price", "ask1Price", "ratio", "pos.length"],

"rows" : [],

}

tbl.rows.push([totalEq, nowEq, Math.abs(openPrice), depth.Bids[0].Price, depth.Asks[0].Price, ratio, pos.length])

tbl.rows.push(["pos", "type", "amount", "price", "--", "--", "--"])

for (var j = 0 ; j < pos.length ; j++) {

tbl.rows.push([j, pos[j].Type, pos[j].Amount, pos[j].Price, "--", "--", "--"])

}

LogStatus(_D(), "\n", "`" + JSON.stringify(tbl) + "`")

}

} else {

// 撤销挂单

// 重置openPrice

cancelAll()

openPrice = 0

}

Sleep(1000)

}

}

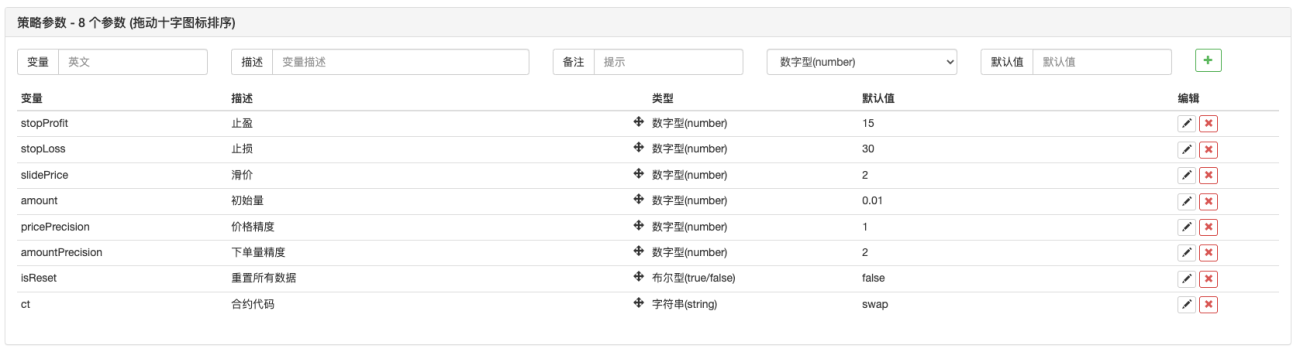

策略参数:

哦对!策略需要起个名字,就叫“猜大小 (dYdX版)”吧。

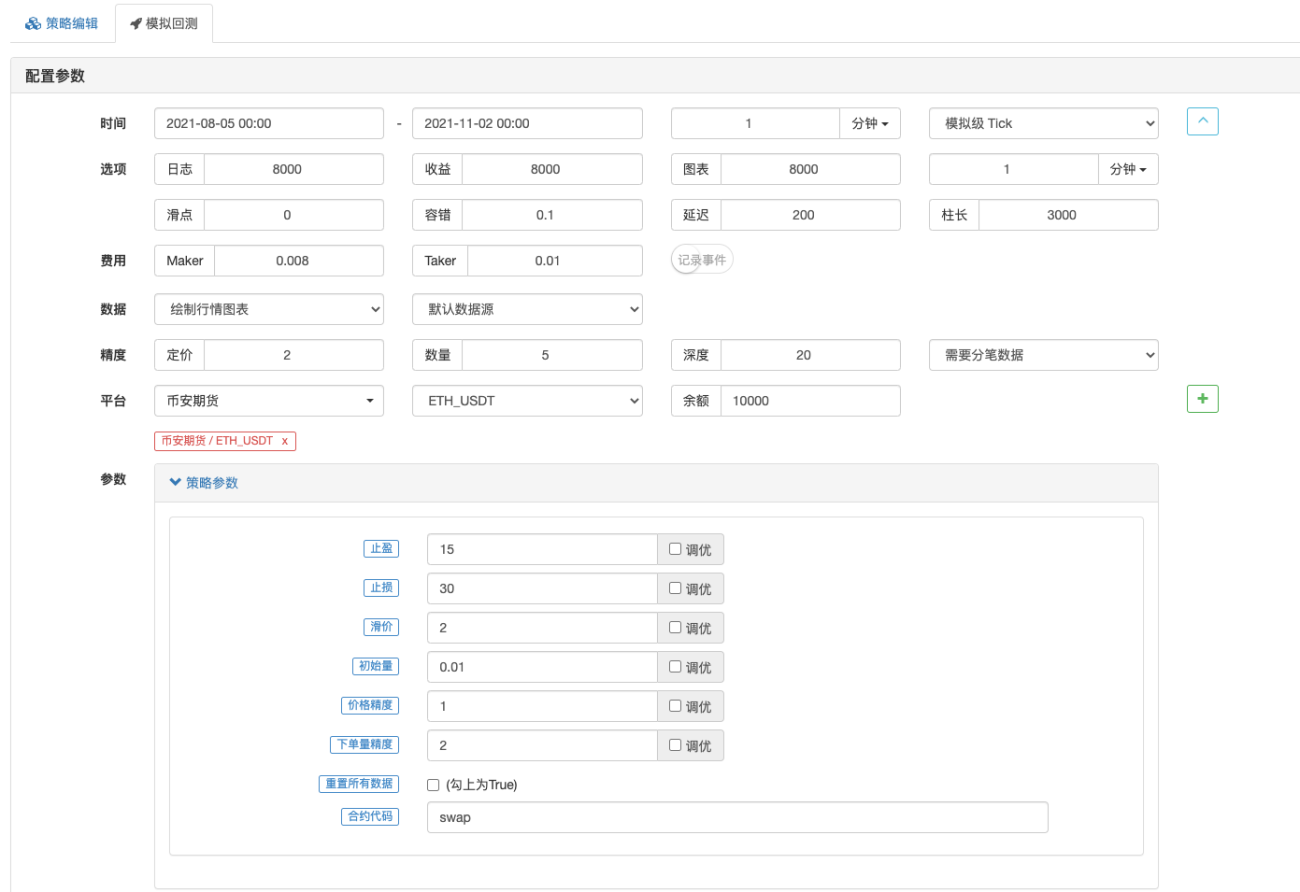

回测

回测仅供参考就好,>_<!

主要检查策略是不是有什么BUG,用币安期货回测。

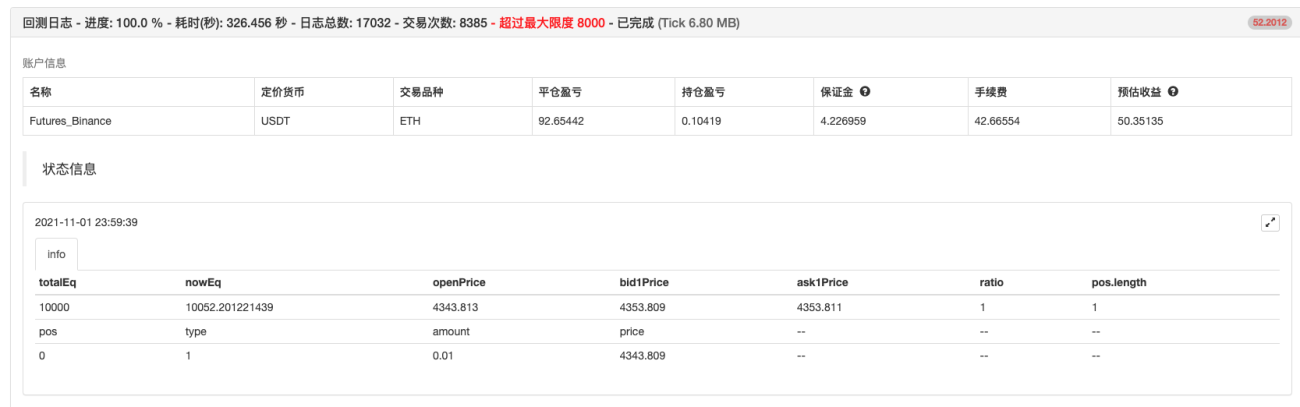

回测完了,没什么BUG。不过感觉我是不是拟合回测系统了..T_T,实盘跑着玩一下。

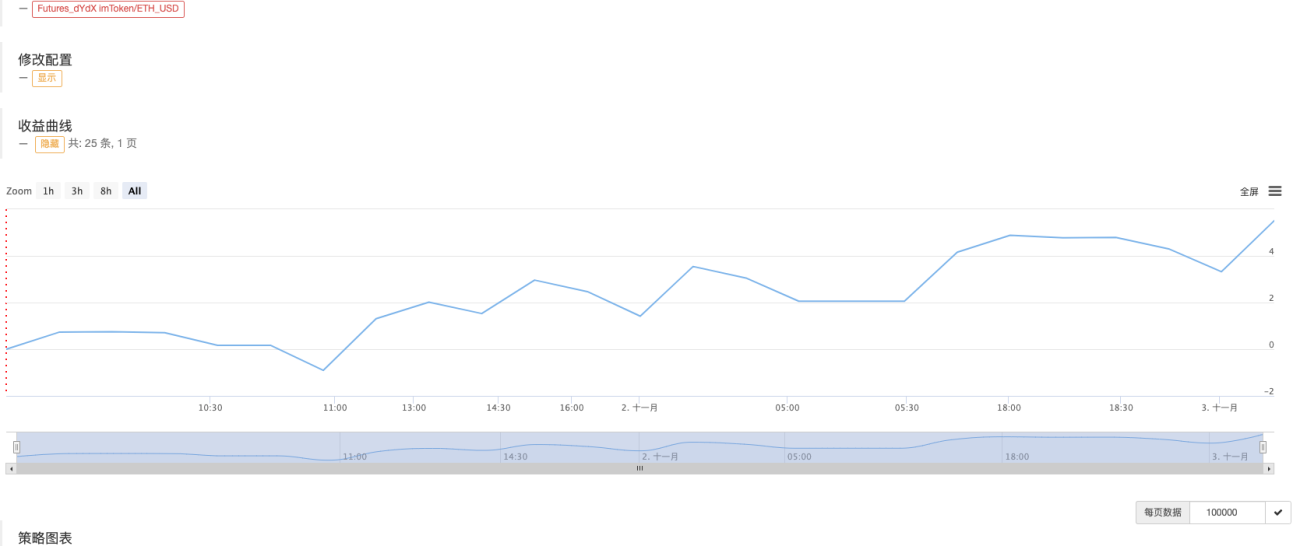

实盘跑跑

本策略仅供学习、参考,千万~千万不要实盘使用!!

问一下, dydx去中心化交易所现在是否支持现货交易? 还是只能永续合约? 从来没用过 去中心化交易所, 如果dydx支持现货交易, 可以考虑做个现货网格交易策略. 还有就是去中心化交易所, 确认买卖是否成功还需要等待时间, 不像中心化交易所那么闪电般快, 需要旷工确认. 要是速度这些克服了, 又支持写网格等量化策略, 那是非常好.

- 1