韭菜保护程序(唐安奇通道+均仓策略)

1

Follow

57

Followers

适用于所有现货币种

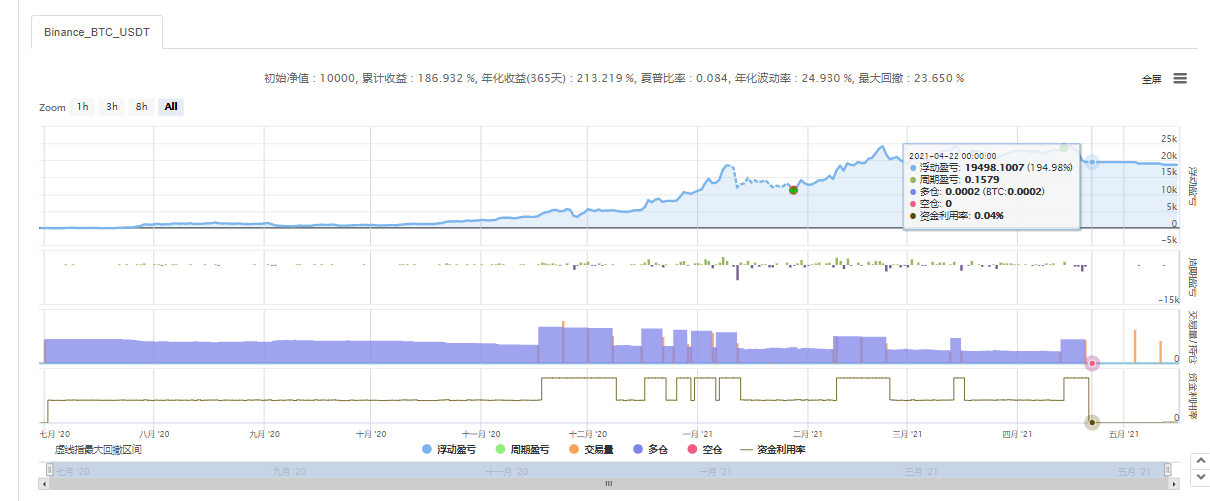

其实吃的就是牛市红利,策略的作用只是降低了回撤,躲开暴跌

最新回测结果:顺利躲过暴跌,4.22就空仓了

使用要求:你百分之一的资金要能购买该币种的最小交易单位

赚钱的老板欢迎打赏我一杯奶茶钱

Source

Python

'''backtest

start: 2021-04-01 00:00:00

end: 2021-04-30 23:59:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Binance","currency":"ETH_USDT","stocks":0}]

'''

import time

class juncang_strategy():

def __init__(self,exchange):

self.p = 0.5

self.account = None

self.cny = 0

self.btc = 0

self.exchange =exchange

#K线合成函数

def k_compose(self,Recordlist,num):

newRecordlist = []

for i in range(len(Recordlist)):

if (i+1)%num == 1:

tempk = {}

tempk["Time"]=Recordlist[i]["Time"]

tempk["Open"]=Recordlist[i]["Open"]

tempk["High"]=Recordlist[i]["High"]

tempk["Low"]=Recordlist[i]["Low"]

tempk["Close"]=Recordlist[i]["Close"]

tempk["Volume"]=Recordlist[i]["Volume"]

newRecordlist.append(tempk)

elif (i+1)%num == 0:

if Recordlist[i]["High"]>tempk["High"]:

tempk["High"] = Recordlist[i]["High"]

if Recordlist[i]["Low"]<tempk["Low"]:

tempk["Low"] = Recordlist[i]["Low"]

tempk["Time"]=Recordlist[i]["Time"]

tempk["Close"]=Recordlist[i]["Close"]

tempk["Volume"]=tempk["Volume"]+Recordlist[i]["Volume"]

del(newRecordlist[-1])

newRecordlist.append(tempk)

else:

if Recordlist[i]["High"]>tempk["High"]:

tempk["High"] = Recordlist[i]["High"]

if Recordlist[i]["Low"]<tempk["Low"]:

tempk["Low"] = Recordlist[i]["Low"]

del(newRecordlist[-1])

newRecordlist.append(tempk)

return newRecordlist

#唐安奇通道计算,分析出当前什么行情

def donchian(self):

exchange.SetMaxBarLen(2000)

temp_k = _C(self.exchange.GetRecords,PERIOD_D1)

week_kline = self.k_compose(temp_k,7)

rt=False

# Log(len(week_kline),week_kline[-1]["High"],TA.Highest(week_kline, 20, 'High'))

if len(week_kline)>20:

if week_kline[-1]["High"]>TA.Highest(week_kline, 20, 'High'):

rt = '全仓'

elif week_kline[-1]["High"]<TA.Highest(week_kline, 20, 'High') and week_kline[-1]["Low"]>TA.MA(week_kline, 10)[-1]:

rt = '均仓'

elif week_kline[-1]["Low"]<TA.MA(week_kline, 10)[-1]:

rt = '空仓'

else:

rt = '均仓'

return rt

def cancelAllOrders(self):

orders = self.exchange.GetOrders()

for order in orders:

self.exchange.CancelOrder(order['Id'], order)

return True

#全仓买入函数

def allin(self):

kr = _C(self.exchange.GetRecords,PERIOD_H1)

account = _C(self.exchange.GetAccount)

self.cny = account.Balance

buynum=_N(self.cny*0.99/kr[-1].Close,3)

if buynum>0:

Log("全仓allin")

self.exchange.Buy(kr[-1].Close,buynum)

#全仓卖出函数

def allout(self):

kr = _C(self.exchange.GetRecords,PERIOD_H1)

account = _C(self.exchange.GetAccount)

self.btc = _N(account.Stocks,3)

if self.btc>0:

Log("空仓allout")

self.exchange.Sell(kr[-1].Close,self.btc)

#均仓函数

def balanceAccount(self):

kr = _C(self.exchange.GetRecords,PERIOD_H1)

account = _C(self.exchange.GetAccount)

if account is None:

return

#赋值

self.account = account

#赋值

self.btc = account.Stocks

self.cny = account.Balance

accountmoney=self.btc * kr[-1].Close + self.cny

self.p = self.btc * kr[-1].Close / accountmoney

tradenum=_N(accountmoney/kr[-1].Close/100,3)

if tradenum<0.001:

tradenum=0.001

#判断self.p的值是否小于0.48

# Log(self.p)

if (0.45<self.p < 0.49):

#调用Log函数并传入参数"开始平衡", self.p

Log("开始平衡", self.p)

self.exchange.Buy(kr[-1].Close, tradenum)

Log("持币数:",self.btc,"现金数:",self.cny)

#判断self.p的值是否大于0.52

elif (0.55 > self.p > 0.51):

#调用Log函数并传入参数"开始平衡", self.p

Log("开始平衡", self.p)

#调用Sell函数并传入相应的参数

self.exchange.Sell(kr[-1].Close, tradenum)

Log("持币数:",self.btc,"现金数:",self.cny)

elif (self.p >= 0.55):

#调用Log函数并传入参数"开始平衡", self.p

Log("开始平衡,快速平仓", self.p)

self.exchange.Sell(kr[-1].Close, _N(tradenum*10,3))

Log("持币数:",self.btc,"现金数:",self.cny)

elif (self.p <= 0.45):

#调用Log函数并传入参数"开始平衡", self.p

Log("开始平衡,快速建仓", self.p)

self.exchange.Buy(kr[-1].Close, _N(tradenum*10,3))

Log("持币数:",self.btc,"现金数:",self.cny)

#交易循环

def loop(self):

self.cancelAllOrders()

rt=self.donchian()

if rt=='全仓':

self.allin()

elif rt=='均仓':

self.balanceAccount()

else:

self.allout()

Sleep(1000*60)

#函数main

def main():

#reaper 是构造函数的实例

reaper = juncang_strategy(exchange)

while (True):

reaper.loop()

Related strategies