【Composite CTA Trading System New 】(Multi-factor + Multi-variety + Multi-strategy Adaptive Public Version)

【Composite CTA Trading System New 】(Multi-Factor + Multi-Variety + Multi-Strategy Adaptive Public Version)

A composite strategy module that has been stable and profitable for 800 days of live trading

Hello traders, after several years of live testing, we are pleased to share with you this composite CTA trading system module. This strategy maintains the idea of combining multiple factors, varieties, periods, and strategies, including dozens of sub-strategies such as trend, band, oscillation, and alternative. The holding period ranges from several days to several weeks, and the strategy has a large capacity, suitable for long-term operation with large funds. The profit point of the strategy is the volatility brought by active varieties and active markets. The strategy's drawdown period is a long-term market downturn and disorderly oscillation. The highlight of this strategy is that it has undergone more than 1000 days of live testing (there is a live trading address at the end of the article), and has withstood the test of bull and bear markets. Below, we will introduce this strategy in detail.

Hello~Welcome come to my channel!

Welcome all traders to my channel. I am a Quant Developer, and I develop full-stack CTA & HFT & Arbitrage and other trading strategies.

Thanks to the FMZ platform, I will share more content related to quantitative development in my quantitative channel, and work with all traders to maintain the prosperity of the quantitative community.

For more information, please move to my channel~ I’m waiting for you here to tease 【TradeMan Home】

I. CTA Trading Strategy

CTA stands for Commodity Trading Advisor Strategy, also known as Managed Futures Strategy. It is a type of fund in which professional managers use client funds to invest in futures and options markets with the goal of achieving absolute returns, while charging corresponding investment advisory fees. The first publicly offered futures fund was established by American stockbroker Richard Donchuan in 1949, marking the birth of CTA funds. CTA funds began to rise in the 1970s and in the 21st century, funds using CTA strategies began to show explosive growth. Global CTA funds include: Yuansheng Asset, Aspect Capital, Transtrend B.V., and others.

In terms of investment methods, there are two types of CTA funds. One is subjective CTA, in which fund managers subjectively judge trends based on fundamentals, research, or trading experience, and decide on buying and selling points. The other is quantitative CTA, which analyzes and establishes quantitative trading strategy models, and makes investment decisions based on the buy and sell signals generated by the model. In terms of specific strategies, CTA can be divided into trend, reversal, and band arbitrage strategies. The trend strategy refers to tracking the trend of different periods of the trading target and conducting long or short operations. The reversal strategy refers to using the reversal volatility of the target price for reverse trading. Arbitrage strategies include inter-period arbitrage, inter-variety arbitrage, spot-futures arbitrage, and funding fee arbitrage. Today, quantitative CTA strategies are roughly divided into two categories: traditional CTA, which is mainly rule-based, and predictive CTA, which is mainly based on machine learning and deep learning. Traditional CTA mostly uses linear models, which have strong interpretability and universality, but lower returns and require users to have more experience to optimize. Predictive CTA requires more systematic mathematical and factor reserves, and there are many requirements for the use and combination of nonlinear prediction models. Each type of CTA strategy and methodology has its own advantages and disadvantages, and investors need to choose and match them independently.

II. Composite CTA Trading System Based on Multi-Factor + Multi-Variety + Multi-Strategy

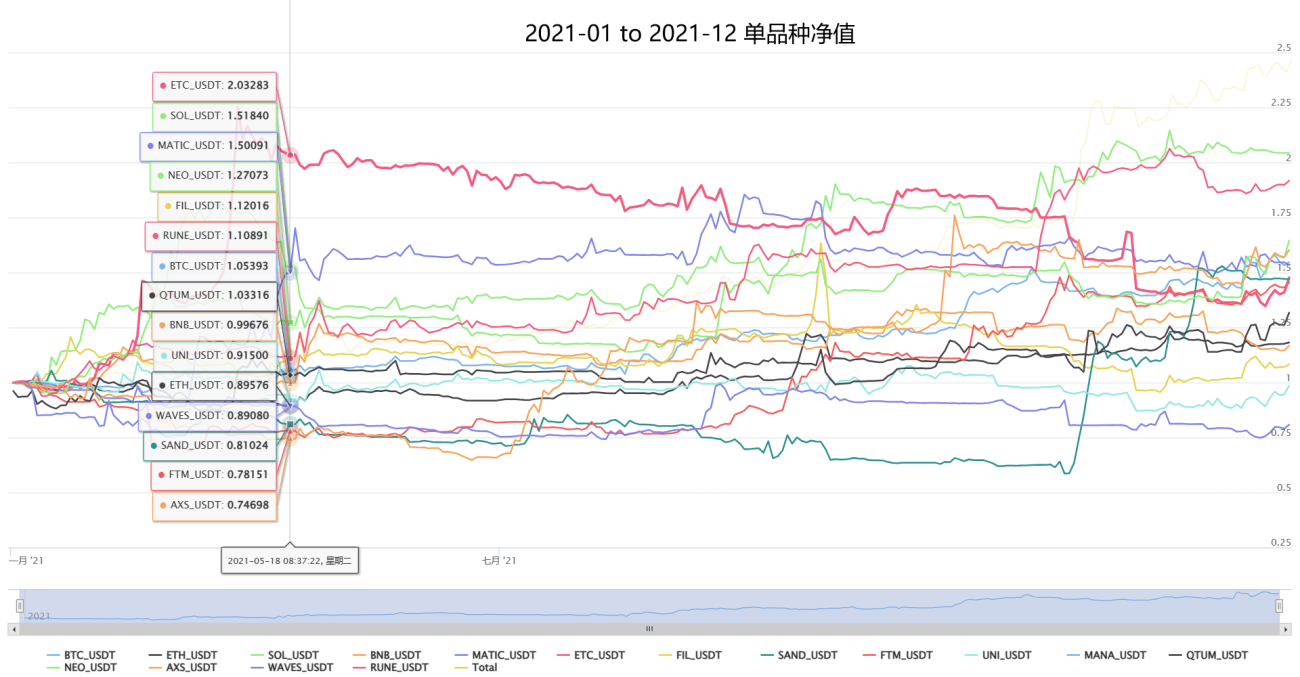

This strategy is based on the low-frequency, trend-following, small-profit, compound-interest trading idea, and practices the combination of multiple factors, varieties, strategies, and dimensions, and has reached a relatively safe and stable state. Some sub-strategies are shown below:

● Trend strategy: Since various behavioral finance effects exist in financial markets, momentum effects are widely used. We use an independently developed multidimensional trend factor library to monitor multiple market information dimensions and time dimensions around the clock, and use multiple protection exit plans (factor signal aggregation exit, dynamic adaptive protection, extreme exhaustion exit).

● Regression strategy: Regression effects are also widely present in financial markets. We use an independently developed multidimensional oscillation factor library to capture overbought and oversold states at various levels and conduct regression trading to hedge trend signals.

● Band strategy: Based on the effect of the market trend movement having three ups and downs, we conduct band trading based on multidimensional trends, and capture reverse weak signals to add or reduce positions, which is used to smooth the trend curve.

● Alternative strategy: Other types of strategies, including statistical strategies and anomaly strategies.

At the same time, this strategy also pays great attention to risk control and capital management. Always remember the saying: "In CTA trading, risk control should always come first, and you should always be cautious." Traders need to set their own risk tolerance levels. The risk control system includes but is not limited to risk exposure management, single signal volatility position control, stop loss/exit principles, portfolio risk management, market feedback, and strategy capital curve adaptive adjustment mechanism. It should be noted that CTA strategies are not violent strategies, but belong to market-following beta strategies. They follow profits when there is market volatility and defend against losses when there is disorderly market volatility. CTA strategies should be robust and have long-term vitality, rather than explosive returns, similar to the relationship between crocodiles and cheetahs in the animal world.

III. Strategy Performance and Profit/Loss Characteristics under Different Market Conditions

■ This strategy is suitable for both coin-based and USDT-based futures contracts. Multiple varieties can be configured in USDT-based contracts, but profits and losses are calculated in USDT. Some users prefer to hold cryptocurrencies for the long term and can also hold coins to do corresponding coin-based futures contracts, where profits and losses are calculated in coins. This can enhance the coin-based effect and obtain excess α returns from the market.

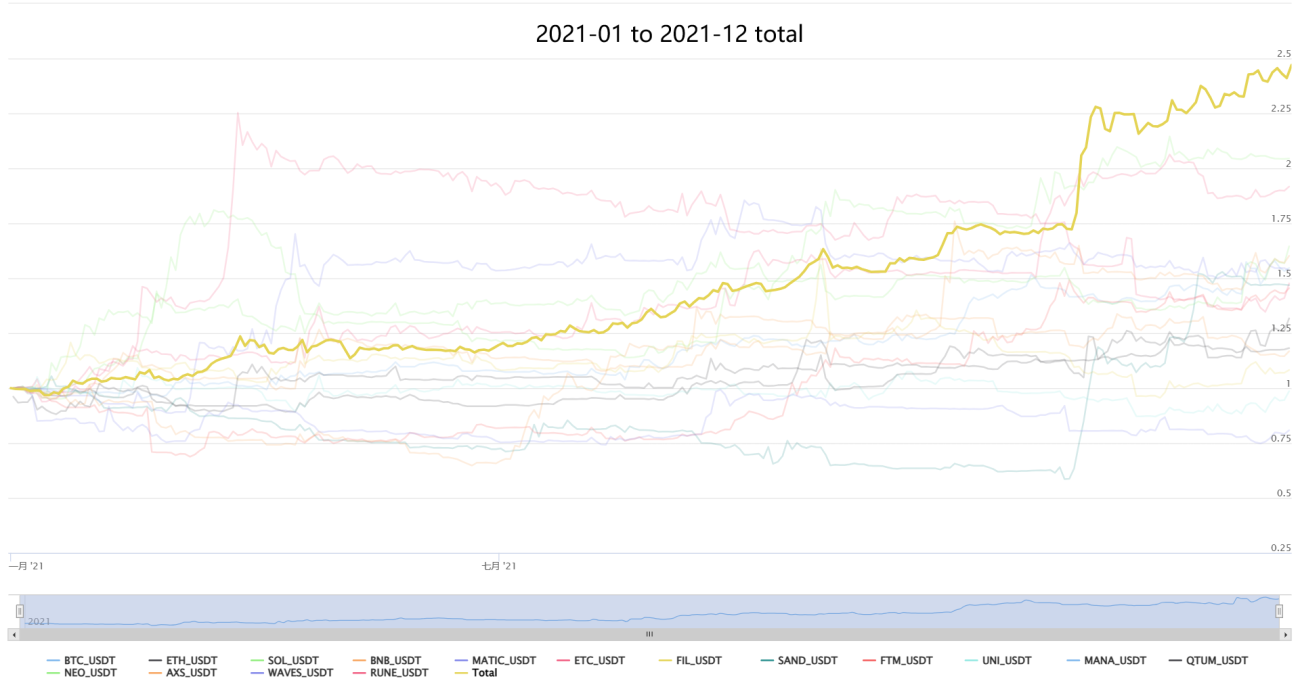

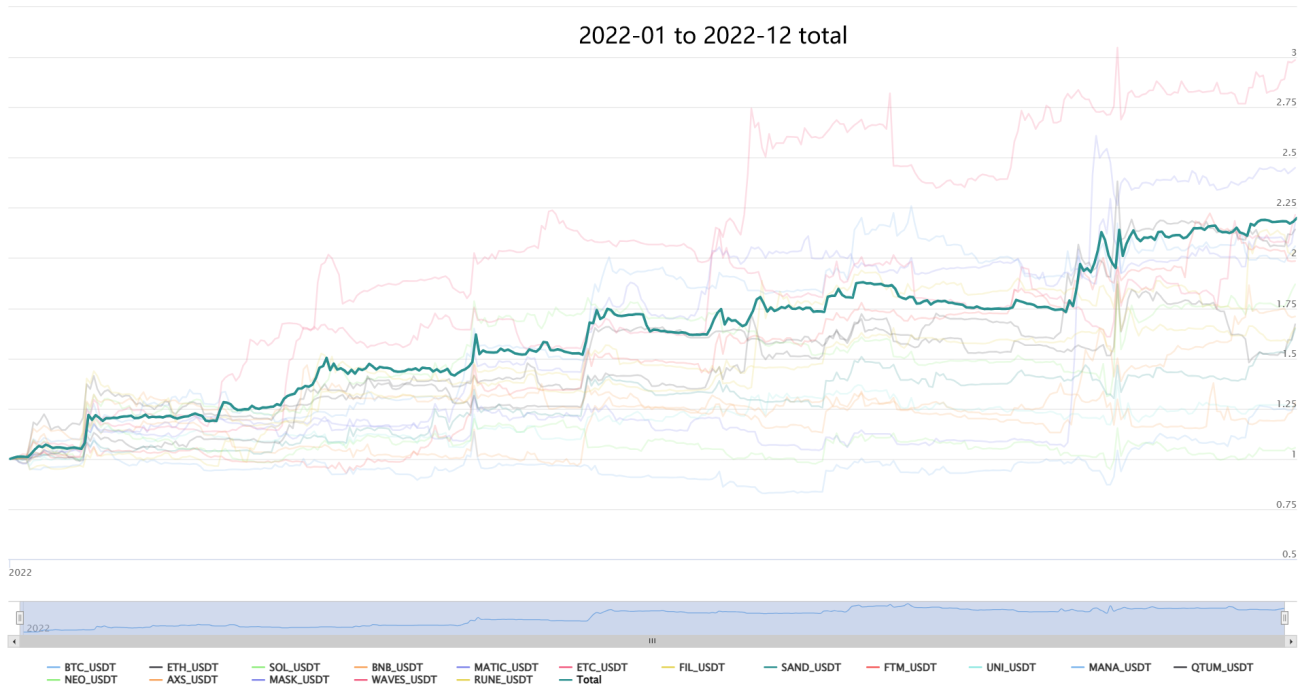

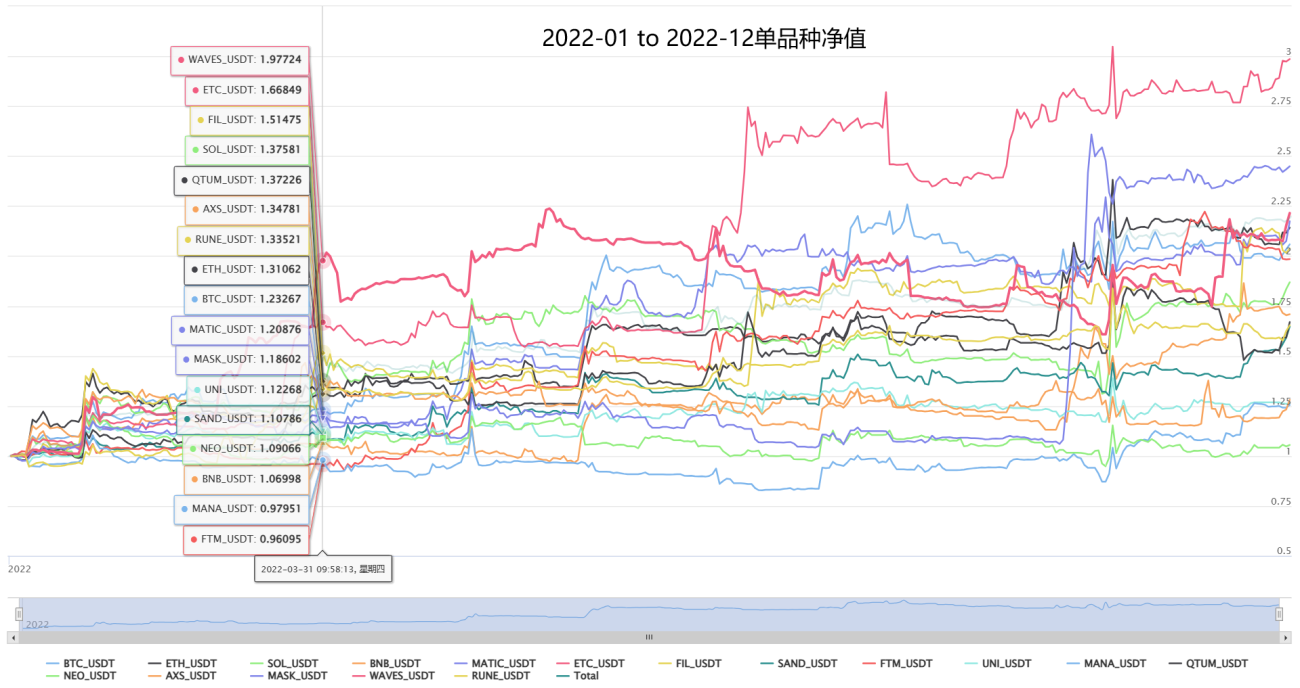

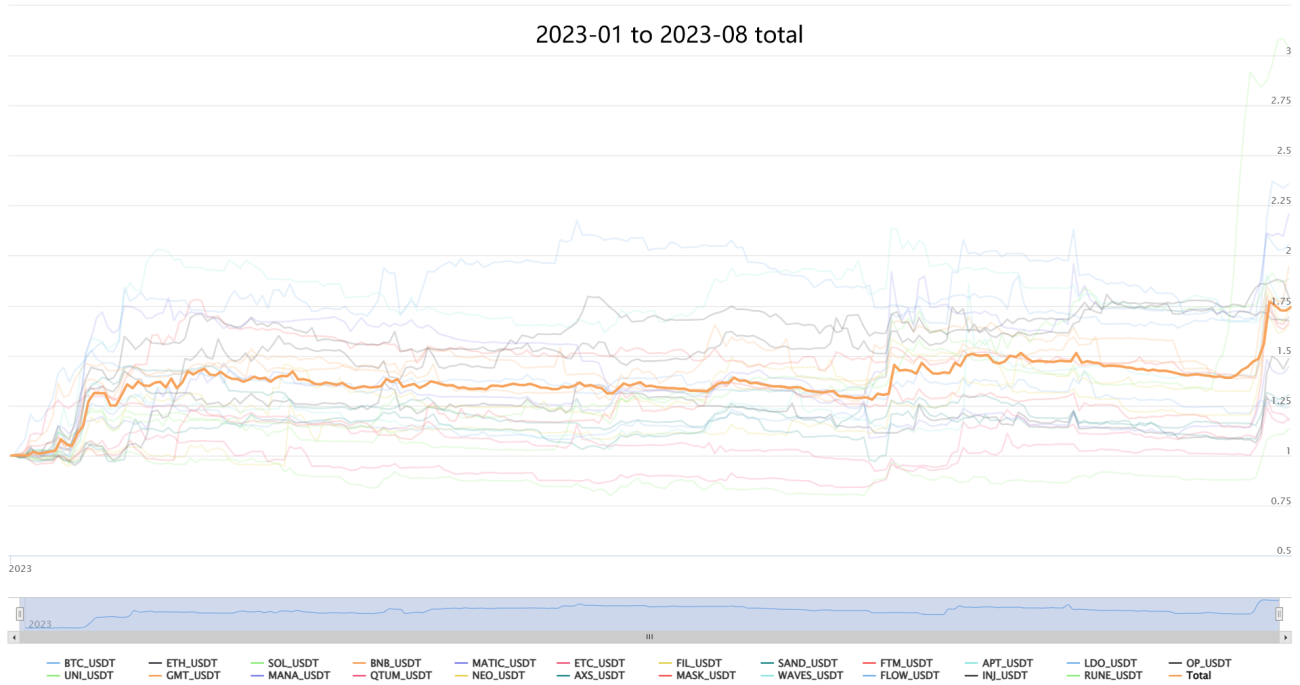

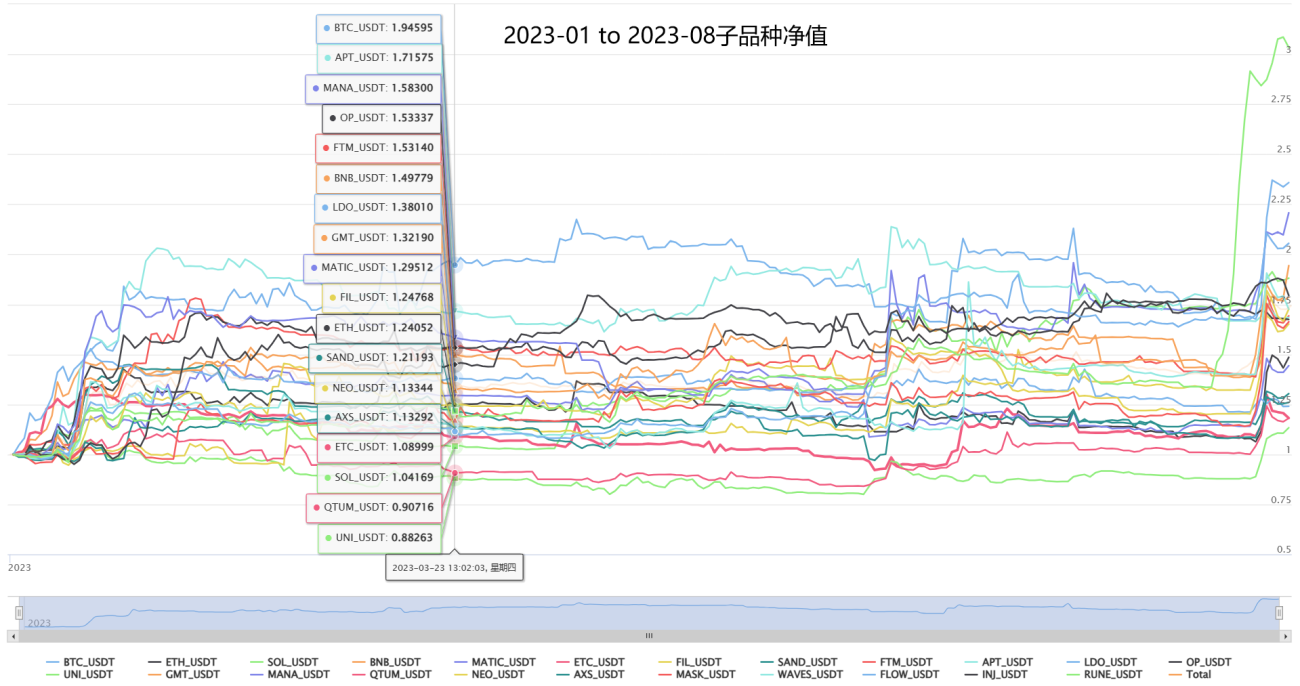

■ Backtesting results are displayed separately for OKEx quarterly coin-based futures contracts and Binance swap USDT-based futures contracts. The data for OKEx coin-based futures contracts is longer and can observe the performance of several bull and bear markets from 2018 to the present, while the data for Binance USDT-based futures contracts mostly starts from 2020 and can observe the performance of this round of bull and bear strategies. The backtesting was conducted with a Taker fee of 0.06%.

■ This strategy firmly believes that universality and robustness are the first priority for CTA strategies (if you want to be aggressive, you need to study other niche strategies). All tests and live trading use the same parameters, and different varieties also use the same parameters. To verify the robustness of the strategy, this strategy was also applied to the testing of dozens of varieties of domestic commodity futures, and also achieved good returns, which will be displayed one by one below.

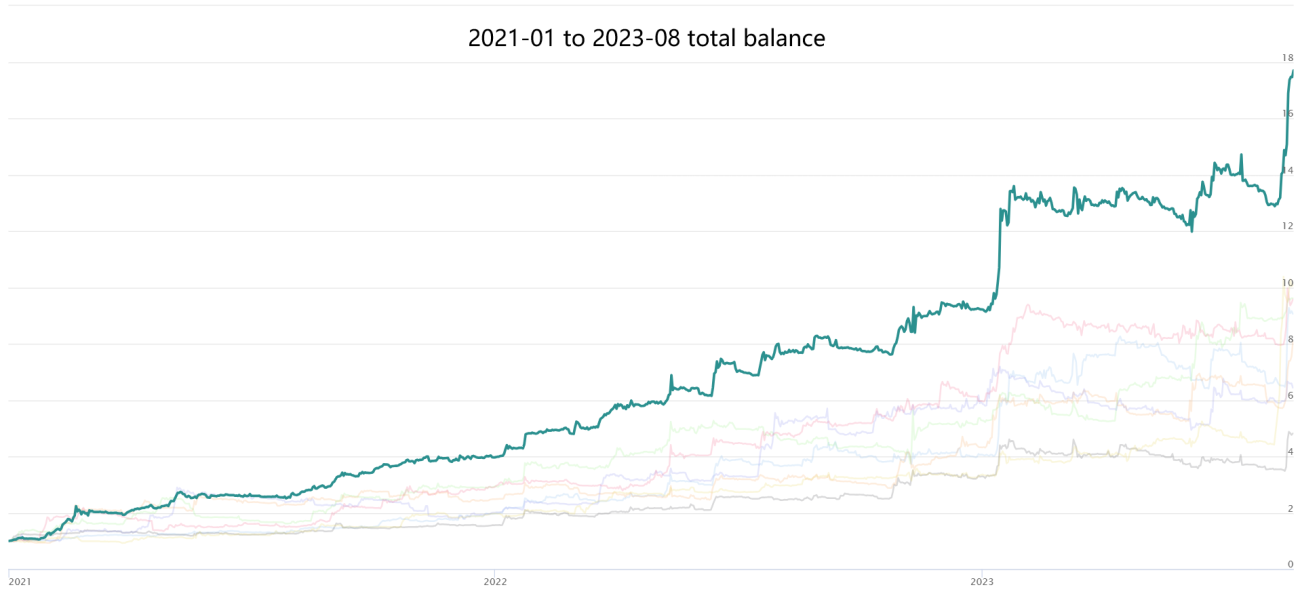

■ Under normal risk mode, the maximum drawdown of the strategy is about 25%, and the expected annualized return is 50%-150% based on market volatility. Users can expand or reduce their risk exposure according to their own risk preferences. Risk and return are unified.

■ Good backtesting results do not necessarily mean anything. This strategy has been live on the FMZ platform since 2021, and although there have been multiple modifications and adjustments along the way, the more than 1000 days of live trading accumulation has still added a lot of trust to the strategy, and the problems and experiences during this period will continue to be injected into new iterations.

USDT-based Testing: 2021-01 to 2023-08

Commodity Futures Stress Testing: To ensure the strong robustness of the strategy, stress testing was conducted using domestic commodity futures without special optimization and using the same parameters. The tested varieties include all varieties in each sector, with funds evenly allocated, including silver, Shanghai aluminum, Shanghai copper, gold, asphalt, fuel oil, hot-rolled coil, Shanghai nickel, rebar, rubber, stainless steel, styrene, corn, iron ore, coke, coking coal, eggs, plastics, live pigs, soybean meal, palm oil, polystyrene, apples, cotton, red dates, glass, soda ash, silicon iron, ferrosilicon, white sugar, PTA, thermal coal, 500 CSI, 300 Shanghai and Shenzhen, 10-year government bonds, 2-year government bonds, and crude oil. As can be seen, the strategy remains stable in decades of performance, with stable profits in the medium and long term, experiencing the super adaptability of this strategy group.

IV. Cooperation Method:

This strategy has been live for more than 800 days since 2021, crossing bull and bear markets, and has a certain degree of credibility and verifiability. The live trading address is: Composite CTA Trading System New (Multi-Factor + Multi-Variety + Multi-Strategy Adaptive Public Version) - Normal Risk Exposure.

Quantitative trading is not a perpetual motion machine, nor is it omnipotent, but it is definitely the direction of future trading, and it is worth every trader's learning and use! Welcome all traders to point out shortcomings, discuss together, learn and progress together, ride the waves in the magnificent market, and forge ahead.

● More cooperation plans: This strategy has a large capacity and is more suitable for long-term operation with large funds. We welcome cooperation with all bigwigs and maintain an open and win-win cooperation attitude for any individual or institution with needs. We look forward to your discussion and customized cooperation based on your needs and risk preferences.

**Another long-term stable statistical arbitrage strategy of neutral hedging with zero long-term exposure risk, and a stable strategy of making more money than Alpha without exposing the beta risk in the market: **

【Neutral-Hedge Statistical Arbitrage New】(Pure-Alpha dream version)

If you have a higher risk preference, like short-term profit and loss, and have a demand for short-term trading, you can check out another stable high-frequency strategy with a monthly return of 5%-30% and no risk of liquidation:

HFT Market-Making Miner Version (High-Frequency Hedging Market Grid New)

✱ Contact Information (Welcome to communicate and discuss, learn and progress together)

If you have any questions or suggestions about the strategy or cooperation, please feel free to contact us through the following channels:

WECHAT:haiyanyydss

TEL:https://t.me/JadeRabbitcm

✱ Fully automatic CTA & HFT & Arbitrage trading system @2018 - 2025

- 1