Combo 2/20 EMA & Bandpass Filter

1

Follow

1789

Followers

This is combo strategies for get a cumulative signal.

First strategy

This indicator plots 2/20 exponential moving average . For the Mov

Avg X 2/20 Indicator, the EMA bar will be painted when the Alert criteria is met.

Second strategy

The related article is copyrighted material from

Stocks & Commodities Mar 2010

WARNING:

- For purpose educate only

- This script to change bars colors.

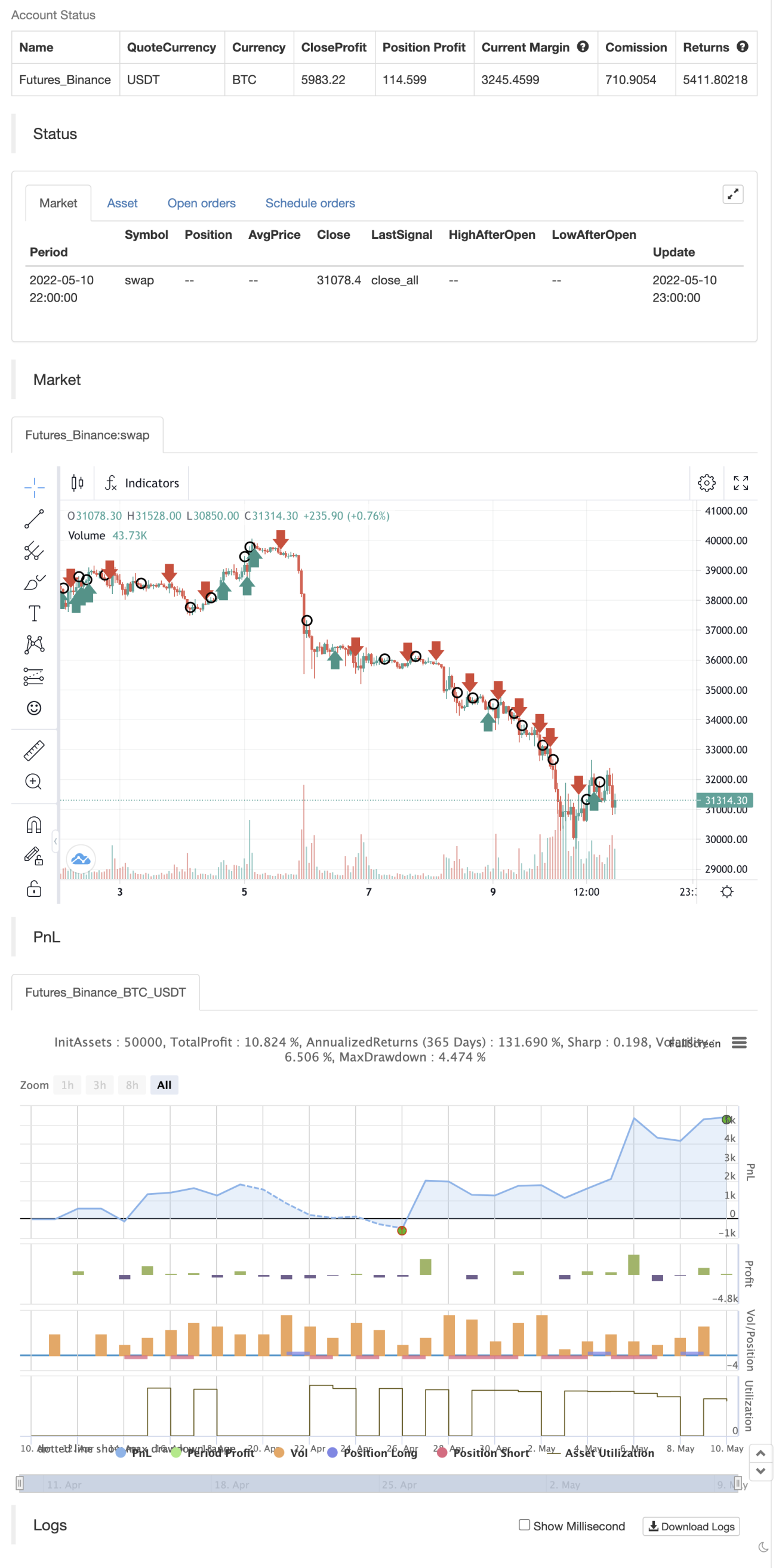

backtest

Source

Pine

//@version=5

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 05/04/2022

// This is combo strategies for get a cumulative signal.

//

// First strategy

// This indicator plots 2/20 exponential moving average. For the Mov

// Avg X 2/20 Indicator, the EMA bar will be painted when the Alert criteria is met.

//

// Second strategy

// The related article is copyrighted material from

// Stocks & Commodities Mar 2010Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1