Multifactor Dynamic Money Management Strategy

Overview

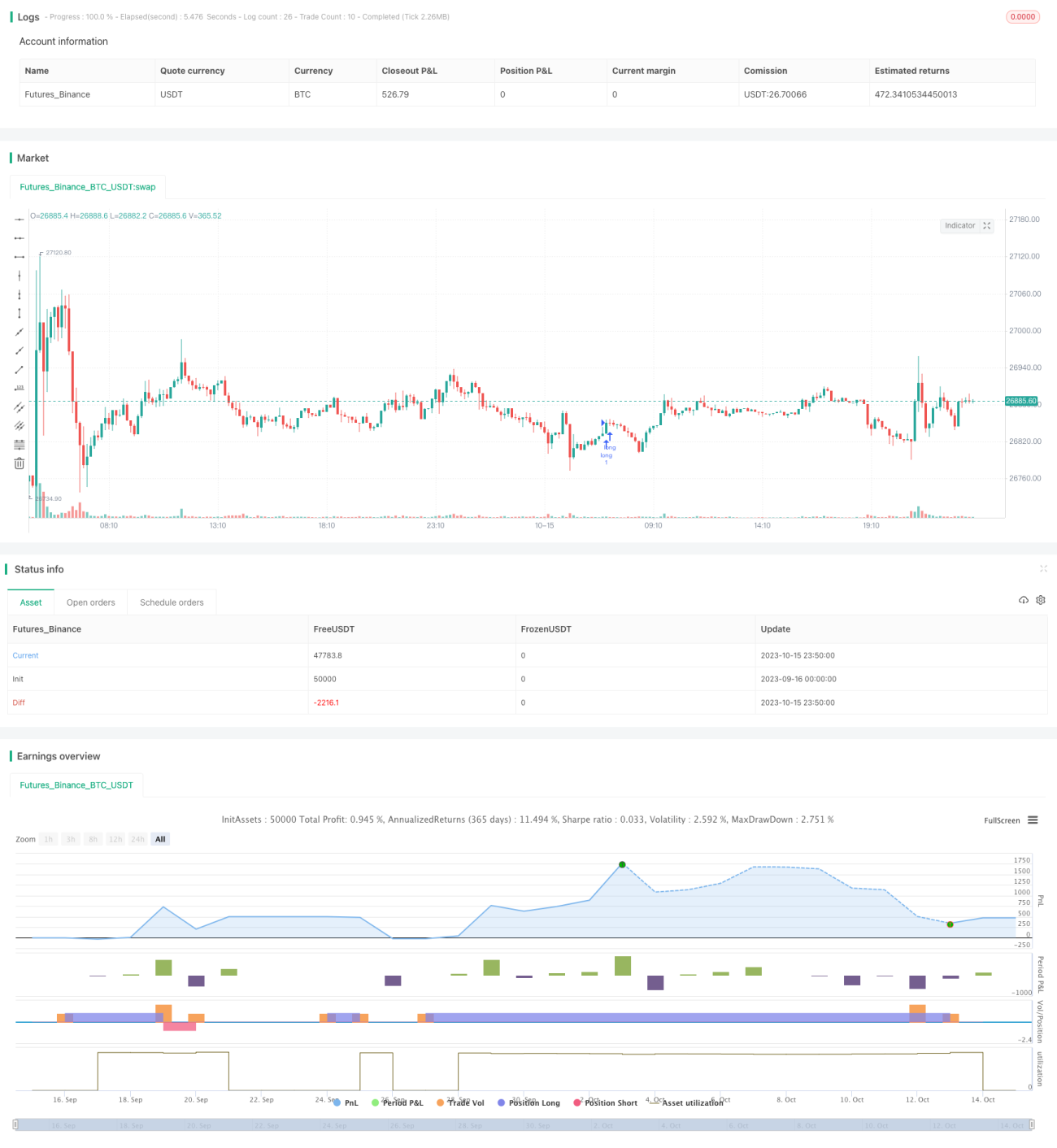

This strategy integrates MACD, RSI, PSAR and other technical indicators together with the dynamic money management methodology to track trends and make reversal trades across multiple timeframes. The strategy can be applied for short-term, medium-term and long-term trading.

Principles

The strategy uses PSAR indicator to determine the trend direction. The crossover between EMA and BB middle line serves as the first confirmation point. MACD histogram direction acts as the second confirmation point. RSI overbought and oversold areas serve as the third confirmation point. Trading signals are generated when all the above conditions are met.

After entering the position, take profit and stop loss points are set. The stop loss point is determined by multiplying ATR value by a fixed number. The take profit point is calculated in the same way. Meanwhile, floating loss percentage stop loss is set. When the loss reaches a certain percentage of total account equity, the stop loss will be triggered.

There is also percentage setting for floating profit. When profit reaches a certain percentage of total account equity, take profit will be triggered.

Dynamic money management calculates position size based on total account equity, ATR value and the multiplier used for stop loss. Minimum trading quantity is also set.

Advantages

-

Multiple factor confirmation avoids false breakouts and improves entry accuracy.

-

Dynamic money management controls single trade risk and protects the account effectively.

-

Stop loss and take profit points are set according to ATR, which can be adjusted based on market volatility.

-

Floating loss and profit percentage settings lock in profits and prevent pullbacks.

Risks

-

Multiple factor combinations may miss some trading opportunities.

-

High percentage settings can lead to greater losses.

-

Improper ATR value settings may result in stop loss and take profit points that are too wide or too aggressive.

-

Improper money management settings may lead to excessively large position sizes.

Optimization Directions

-

Adjust factor weights to improve signal accuracy.

-

Test different percentage parameter settings to find optimal combinations.

-

Select reasonable ATR multipliers based on different product characteristics.

-

Dynamically adjust money management parameters based on backtest results.

-

Optimize timeframe settings and test trading sessions.

Summary

This strategy integrates multiple technical indicators for trend determination and adds dynamic money management to control risks, realizing steady profits across multiple timeframes. It can be further optimized by adjusting factor weights, risk control parameters and money management settings based on backtest results.

- 1