123 Reversal Moving Average Envelope Strategy

Overview

The 123 Reversal Moving Average Envelope Strategy is a quantitative trading strategy that combines 123 reversal trading techniques and moving average envelope indicators. It integrates the strengths of catching market reversal opportunities using reversals and determining trend direction with moving average envelopes, achieving steady profits.

Strategy Logic

The strategy consists of two parts:

The first part is the 123 reversal strategy. Its trading signals come from the KDJ oscillator. Specifically, if the closing price is lower than the previous close for two consecutive trading days, and the 9-day slow K line is below 50, a buy signal is generated; if the closing price is higher than the previous close for two consecutive trading days, and the 9-day fast K line is above 50, a sell signal is generated.

The second part is the moving average envelope strategy. It uses moving averages and envelope lines above and below the moving averages to determine trends. Specifically, if the closing price is higher than the upper band, a buy signal is generated; if the closing price is lower than the lower band, a sell signal is generated.

The strategy combines the above two types of trading signals. It will only open long positions when 123 reversals and moving average envelopes both give buy signals; it will only open short positions when both give sell signals. This filters out some invalid signals and reduces trading frequency while improving profitability.

Advantage Analysis

-

Combines reversal and trend to improve profitability

The 123 reversal strategy excels at catching reversal opportunities near key support and resistance levels. The moving average envelope strategy accurately determines trend direction. Using both improves the probability of catching reversals at high-probability price levels.

-

Double filter reduces trading frequency

Trades are only taken when both indicators give signals. This avoids interference from excessive invalid signals from a single indicator and thus reduces trading frequency and costs.

-

Customizable parameters provide flexibility

The adjustable parameters allow users to tailor the strategy to market conditions and personal preferences for improved adaptability.

-

One-sided trading simplifies operations

The strategy only goes long or short, without reverse positions. This simplifies the logic and reduces risks from being whipsawed.

Risk Analysis

-

Reversals struggle in persistent trends

The strategy relies mainly on reversals for profits. During long trending periods, it may produce continuous losses.

-

Parameter optimization is difficult

The multiple adjustable parameters pose optimization challenges. Improper parameter combinations may degrade performance.

-

High turnover increases trade risks

Frequent position changes allow locking in small profits but also increase costs and risks from overtrading.

-

No drawdown limit

The lack of a stop loss means no limit on maximum drawdown. Black swan events could cause severe losses.

Optimization Directions

-

Add stop loss

Implement a moving or trailing stop loss to limit drawdowns. Stopping out early during abnormal market moves protects capital.

-

Optimize parameters

Backtest and forward test to find optimum parameters for higher stability. Consider dynamic optimization for improved adaptability.

-

Add signal filters

Adding filters like MACD and Bollinger Bands can validate signals and further improve quality while reducing unwanted trades.

-

Reduce trade frequency

Modestly relaxing reversal conditions and adjusting moving average settings to lower turnover can reduce costs and risks.

Conclusion

The 123 Reversal Moving Average Envelope Strategy combines the strengths of reversal trading and trend following for steady risk-adjusted outperformance. Further optimizations can improve parameter robustness for even better results. Its effective synthesis of multiple signal types makes it suitable for trends and ranges, and worthwhile for quant traders to study and implement.

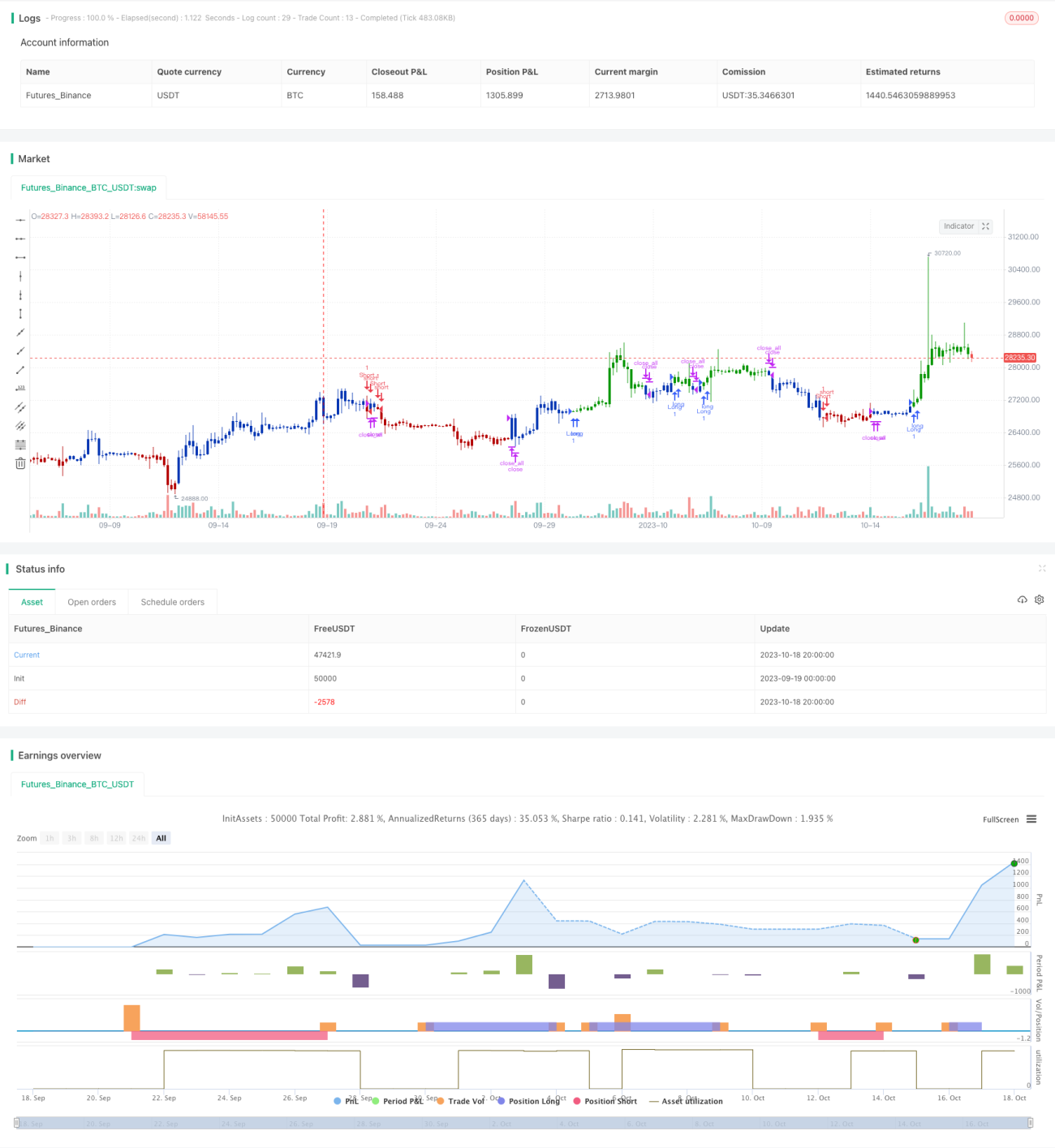

/*backtest

start: 2023-09-19 00:00:00

end: 2023-10-19 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 22/03/2021

// This is combo strategies for get a cumulative signal. - 1