Progressive Take Profit Strategy

Progressive Take Profit Strategy

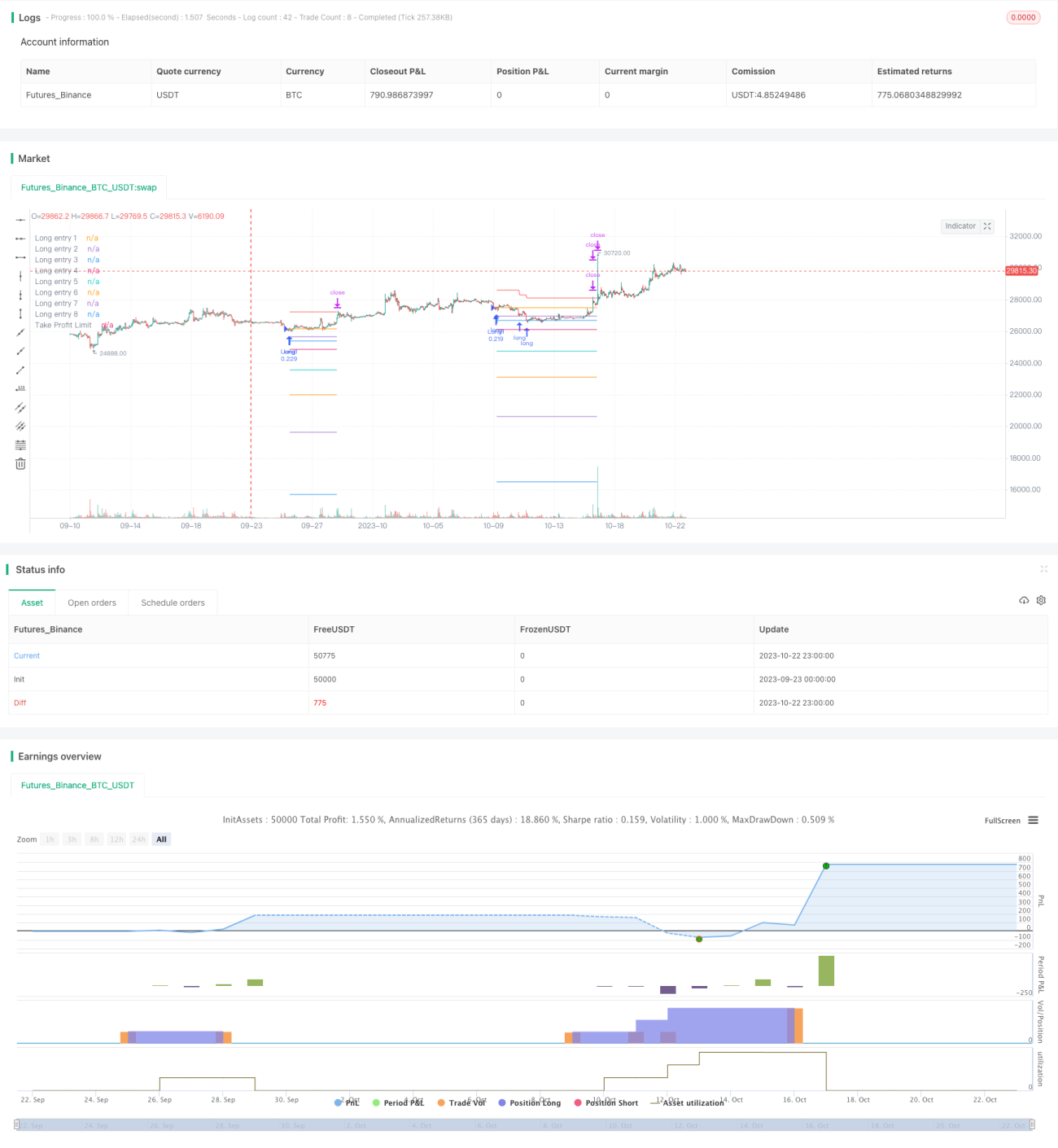

Overview

This strategy combines RSI indicator and price moving average to identify oversold opportunities when price breaks below the moving average line. As the price further declines, the strategy will progressively pyramid more long positions based on preset percentages to achieve cost averaging. When the profit of the positions reaches the configured take profit percentage, the strategy will close the positions. It also introduces a progressive take profit mechanism that dynamically adjusts the overall stop profit price based on per position profits realized. This can effectively reduce the risk of losses and achieve gradual exiting.

Strategy Logic

-

When RSI drops below the oversold line of 29 and closing price is below moving average, open the first long position.

-

When price drops 2% below the first entry price, add a second long position, and so on until maximum 8 entries. This achieves dollar cost averaging.

-

After each entry, record the entry price. These prices serve as the reference prices for entries. Plot them as lines on the chart.

-

After entries, calculate the average holding price. Use 3% of average price as take profit for each position, and 4% for overall position.

-

When price rises above take profit price of a position, close that position.

-

Progressive take profit calculation: after closing each position, deduct the realized profit from the overall take profit price. This slowly drags down the take profit line. Only when the total profit covers max loss will the strategy take profit completely.

-

When price hits the progressive take profit line, close all positions.

Advantages

-

RSI is good at identifying oversold/overbought zones, allowing good entries for reversals.

-

Multiple entries allow cost averaging at low prices.

-

Progressive take profit reduces risk and achieves gradual exits. Losses are contained within a range.

-

Customizable take profit ratio and entry steps allows risk adjustment.

-

Plotted entry and take profit lines offer visual guidance on positions.

Risks

-

Whipsaw markets may trigger excessive entries and exits, causing slippage. Widen the RSI range to reduce trades.

-

Bad configuration of entry steps and ratios may cause over-trading. Be prudent based on account size.

-

Continued pyramiding during declines brings unlimited loss risks. Set a max limit on entries. Keep last entry conservative.

-

Take profit set too tight may exit prematurely. Optimize based on backtest data.

Enhancements

-

Add filters like MACD to avoid bad RSI signals.

-

Incorporate stop loss based on ATR to limit extreme loss events.

-

Optimize entry, take profit and other parameters for different assets.

-

Dynamically adjust take profit based on volatility. Widen when volatile.

Conclusion

The strategy fully utilizes RSI for identifying oversold, combining with MA for reversal trading. The pyramiding and progressive take profit mechanisms control risk while allowing effective long entries. Further optimizations on indicators, take profit etc. can make the strategy more robust. It can be widely applied on trending instruments like index futures and crypto for great investment value.

- 1