Bollinger Band Fitting Strategy

Overview

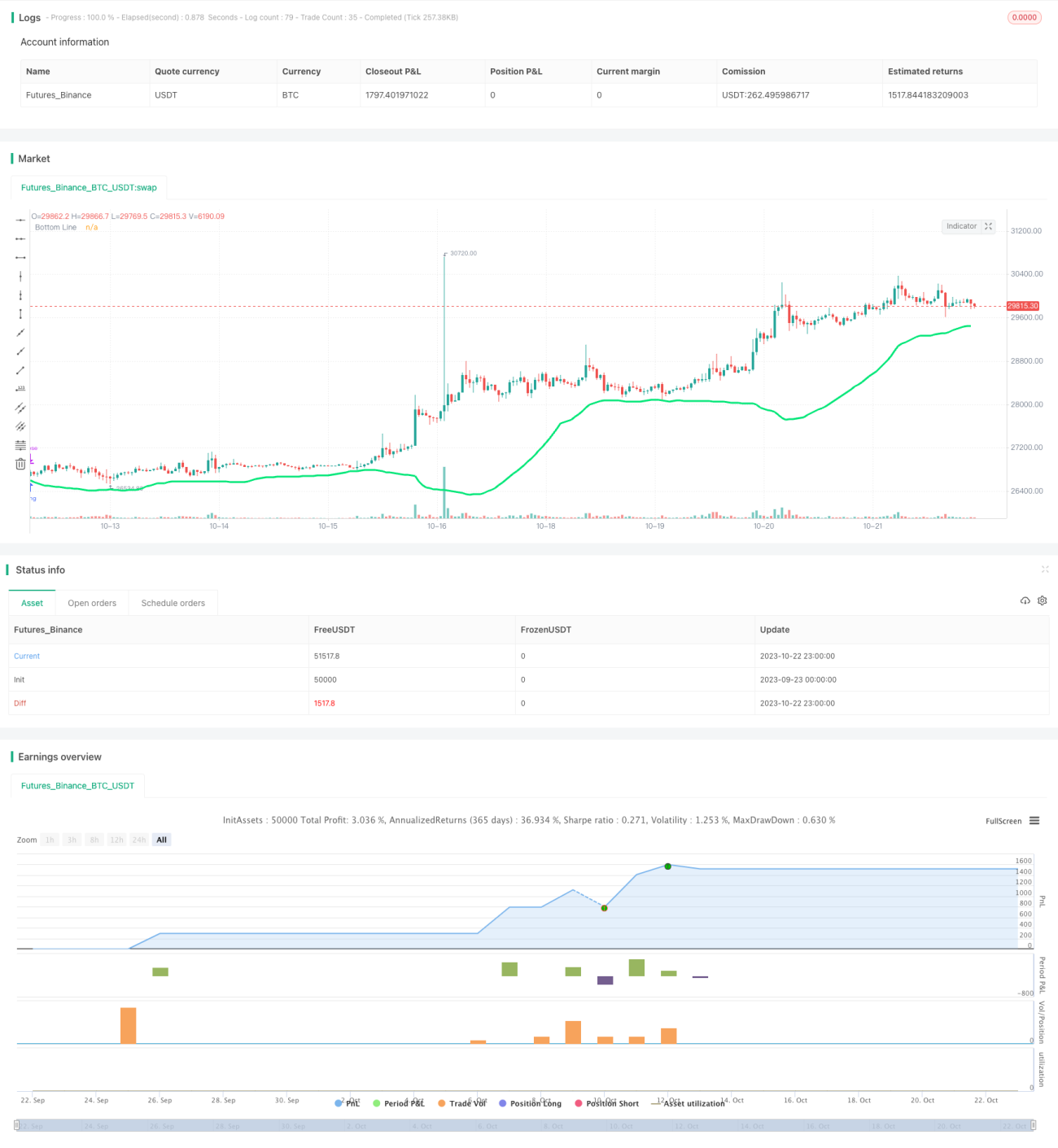

This strategy uses the Bollinger Bands indicator for trend judgment, combined with the RSI indicator to avoid overbuying, as well as candle body filters and color filters to further validate trading signals. Overall, the main idea of this strategy is to buy at the beginning of a trend and exit before the trend reversal, in order to profit.

Principles

This strategy first uses the lower band of the Bollinger Bands indicator. When the price is below the lower band, it is considered an opportunity to open a position. To avoid overbuying, the strategy also introduces the RSI indicator, which requires the RSI to be less than 30 to generate a buy signal. In addition, the strategy sets a candle body filter that requires the body of the current candlestick to be greater than half the average body of the candlesticks over the past 10 periods in order to trigger a buy. Finally, the color filter requires the candle to be green (closing higher) to further validate the timing of the buy.

When the price breaks through the lower band of the Bollinger Bands, the RSI is less than 30, the body is sufficiently large, and the candle is green, a buy signal is generated. When the closing price is higher than the opening price and the body is greater than half of the average body, it is a trend reversal signal indicating closing the position.

Advantage Analysis

The biggest advantage of this strategy is that it can successfully determine the beginning of a trend and enter the market, and exit before the trend reversal, thus profit potential is large. Specifically, the main advantages are:

-

The Bollinger Bands indicator accurately judges trend direction. It uses the price fluctuation range to determine price movements, so using this indicator can effectively determine the start and end of trends.

-

The RSI indicator avoids overbuying. RSI can measure overbought and oversold conditions. Using it avoids wrongly buying during temporary price corrections.

-

Entity filtering increases signal reliability. A larger candle body represents a more powerful breakthrough. Entity filtering ensures buying strong breakthroughs.

-

Color filtering confirms timing. Only buying on green candles further validates proper timing.

-

Candle turning green indicates trend reversal after buying. Traders say "trends take turns", and candle turning green can judge reversal timing.

Risk Analysis

The strategy also has some risks to note:

-

Possibility of false signals from Bollinger Bands. It may also produce false breakout signals when the market oscillates.

-

Losses enlarge without stop loss. The lack of stop loss can lead to larger losses if judgements are wrong.

-

Filtering conditions too strict miss buying opportunities. Multiple stacked filters may miss opportunities.

-

Relies on optimized backtesting results. Parameter and filter settings need optimization and verification, real trading results also need verification.

-

Candle turning green unreliable for determining reversals. It doesn't fully confirm trend reversal.

For the risks, stop loss can control losses, optimizing filters reduces missed buys, using multiple indicators verifies signals, and verifying results in live trading.

Improvement Directions

The strategy can be optimized in several aspects:

-

Optimize Bollinger Band parameters for best settings. Test different periods, standard deviation multiples, etc.

-

Test different oscillators instead of RSI. e.g. KDJ, Williams %R, etc.

-

Add trailing stop loss to control risks. Set reasonable stops based on backtest data.

-

Optimize filter condition parameters. Test different body filter sizes and periods.

-

Incorporate other indicators to confirm signals. e.g. volume-price confirmation indicators.

-

Test different reversal signals. e.g. moving average crosses to determine trend reversal.

-

Test on different products and time frames. Evaluate strategy across different markets.

Conclusion

Overall, the strategy has relatively strong trend following ability and adaptiveness. The core strengths are using Bollinger Bands to determine trend direction and using RSI and filters to ensure timing. But there are also certain risks that need targeted optimization and testing. If parameters and rules can be verified, it may achieve good results in live trading. In conclusion, the strategy has practical value worth exploring.

- 1