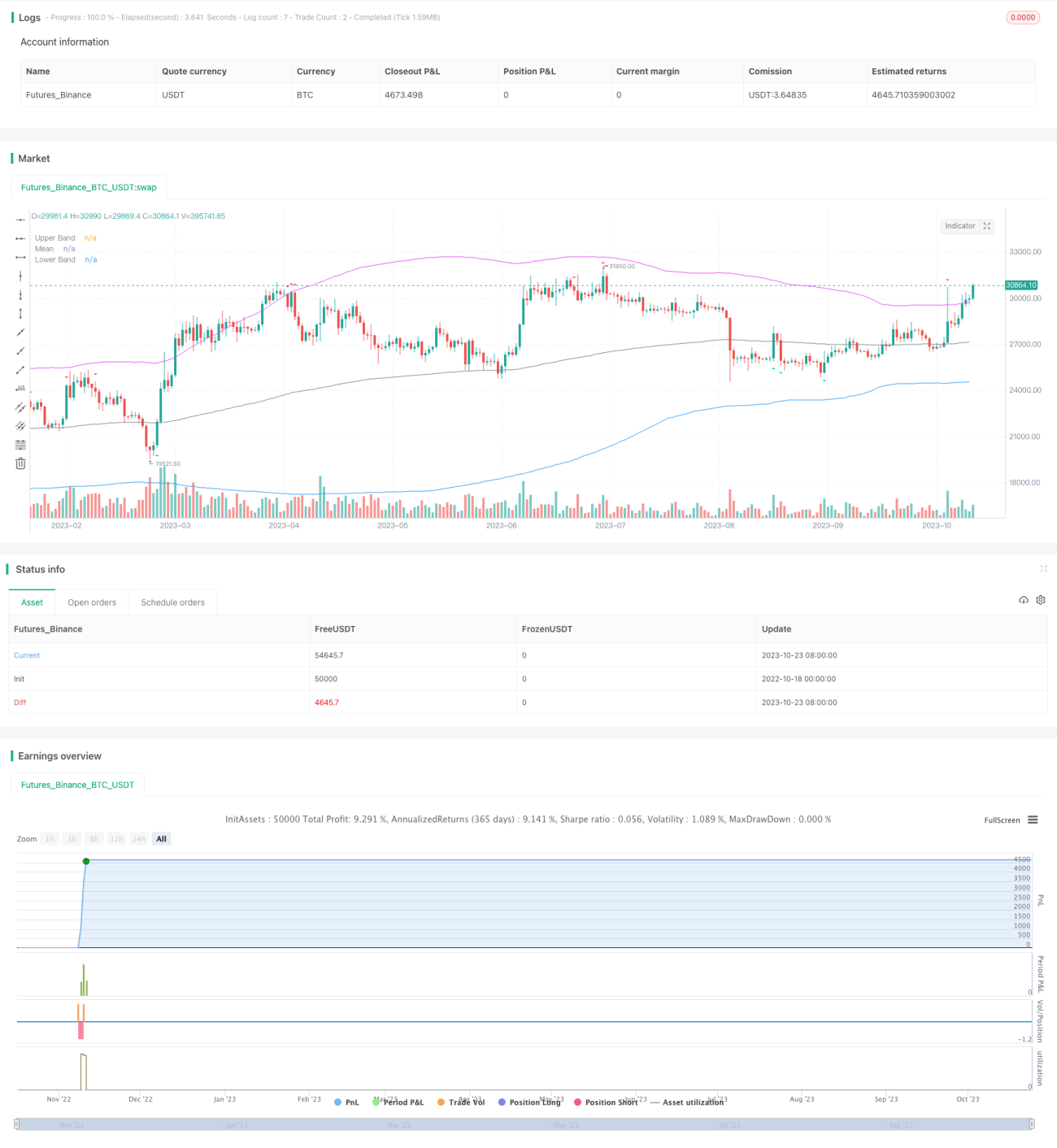

Price Gap and Trend Following Trading Strategy

Overview

This strategy uses the CCI indicator and momentum indicator combined with the RSI indicator to identify market trends and enter when gap appears in overbought/oversold zone. It also utilizes Bollinger Bands to recognize trends and mean reversion range. The strategy can effectively identify breakouts and pullbacks, get in early in trend start, and adapt to different products by adjusting parameters.

Strategy Logic

Firstly, the strategy determines long and short signals by CCI indicator or momentum indicator crossing above/below 0 line. Also it requires RSI to be in overbought/oversold zone, i.e. above 65 for overbought and below 35 for oversold, to avoid false signals.

In addition, the strategy can choose to determine RSI bullish/bearish divergences to ensure more reliable signals.

When CCI or momentum long signal triggers, and RSI is in oversold zone, the strategy will check if previous high and low are both above Bollinger Band mean line. If so, a long signal is generated. Vice versa, when short signal triggers and previous high low are below mean line, a short signal is generated.

Thus the strategy utilizes both trend and oscillation indicators, to get in a trend early and avoid false breakout with mean reversion range. When price breaks out of Bollinger Bands, the strategy will close all positions to lock profit and prevent further drawdown.

Advantage Analysis

-

Combining trend and oscillation indicators can enter trend early and avoid unnecessary positions in range market.

-

Using Bollinger Band mean with price gaps filters false breakouts effectively.

-

Checking historical RSI avoids generating wrong trade signals.

-

Fully automated trading without manual interference, suitable for algorithm trading.

-

Flexible parameter adjustment adapts to different trading products.

-

Stop loss and take profit controls risk effectively.

Risk Analysis

-

Improper Bollinger Band parameters may cause invalid mean reversion identification.

-

Wrong indicator parameters may generate too many false signals.

-

Failed breakout needs timely stop loss when price pulls back to mean.

-

Poor liquidity may cause ineffective breakout trading.

-

Ensure sufficient historical data to avoid poor curve fitting.

-

Pay attention to trading sessions to avoid false breakout.

Improvement Directions

-

Optimize Bollinger Bands parameters for more stable mean reversion range.

-

Test parameters on different products for better optimization.

-

Add position sizing to avoid oversized single position.

-

Add trading session filter to trade mainly in active hours.

-

Incorporate machine learning models to generate more intelligent signals.

-

Integrate more data sources to determine overall market trend.

-

Add more indicators to form a robust indicator ensemble.

Conclusion

This strategy integrates trend and oscillation indicators to capture trends early. With Bollinger Band mean and price gaps it avoids false breakouts effectively. Flexible parameters adapt to different products with great backtest results. Next steps are to optimize parameters and model ensemble for more robustness, and achieve consistent excess returns in the long run.

- 1