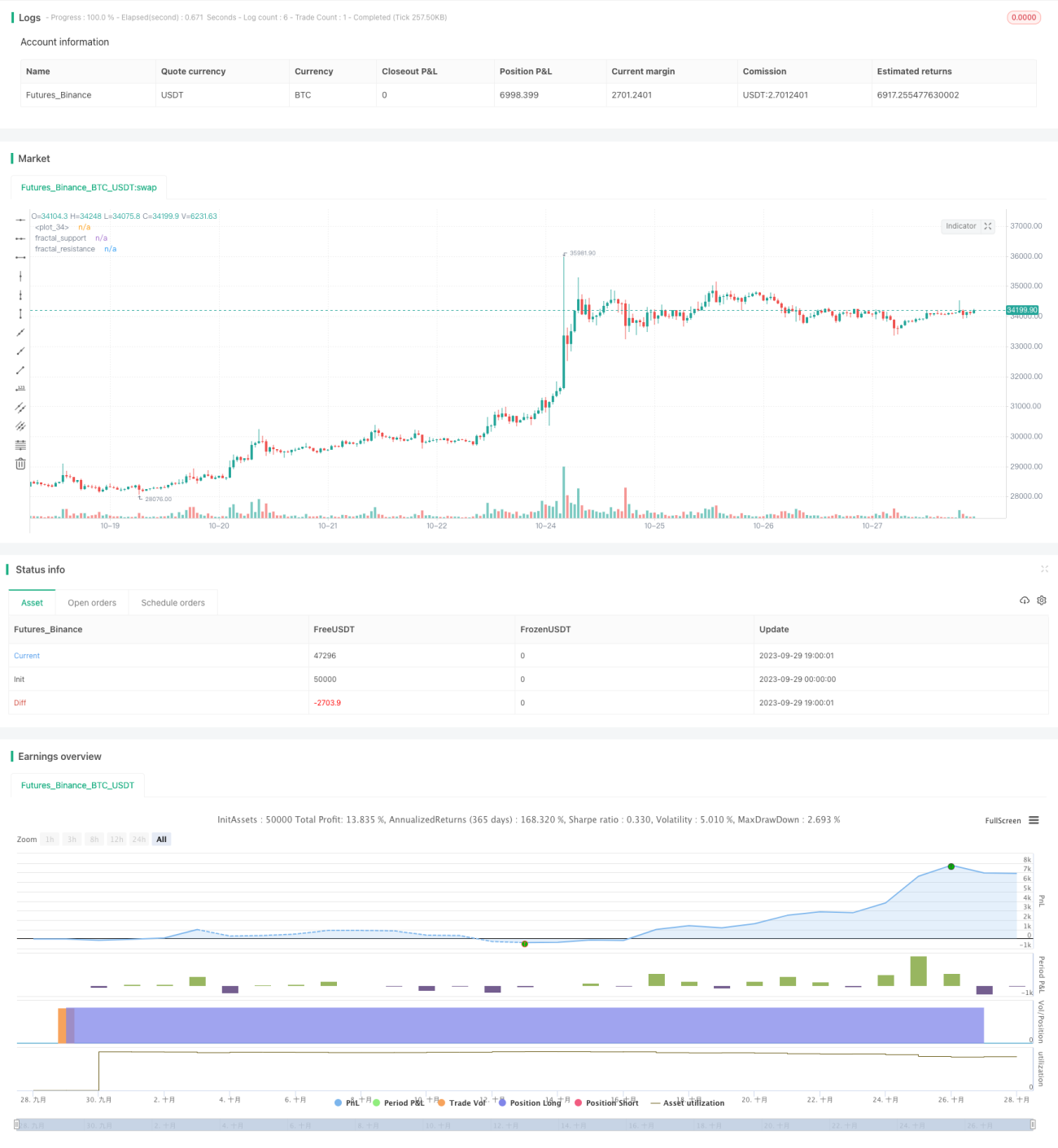

Reversal Trading Strategy Based on Generalized Support/Resistance

Overview

This strategy adopts reversal trading based on bullish/bearish factors, with preset profit-taking levels. The core of the factors is the extended pattern "Generalized Support/Resistance" based on trading volume, suitable for stocks with high volume and volatility. The advantages lie in capturing larger reversal opportunities in medium-short terms and profiting quickly, while it bears the risk of being trapped.

Strategy Logic

-

Identifying bullish/bearish factors based on "Generalized Support/Resistance" with volume

-

Using candlestick patterns to identify classic S/R levels, filtered by significant volume

-

Generalized S/R has better coverage than classic patterns

-

Breaking generalized support signals long factor, breaking generalized resistance signals short factor

-

-

Reversal trading

-

Take reverse position when factor signal triggers

-

If already in position, reduce or add reverse position

-

-

Setting profit target levels

-

Set stop loss based on ATR

-

Set multiple profit levels like 1R, 2R, 3R

-

Partial profit taking when hitting different targets

-

Advantages

-

Capture decent mid-term reversals

S/R breakouts represent strong reversal signals with some reliability, able to catch mid-term reversals

-

Quick profit-taking, small drawdowns

By setting stop loss and multiple profit targets, can achieve quick gains and limit drawdowns

-

Suitable for stocks with significant institutional money and volatility

The strategy relies on volume, requiring sizable institutional participation; also needs volatility to make profits

Risks

-

Getting trapped in range-bound market

Frequent stop loss exit and re-entry in opposite direction can result in whipsaws

-

Failure of support/resistance

Generalized S/R is not absolutely reliable, some failures exist

-

One-sided holding risk

The pure reversal logic may miss large trending opportunities

-

Risk management:

-

Loosen factor conditions, not reverse on every breakout

-

Add other filters e.g. price/volume divergence

-

Optimize stop loss strategy to reduce traps

-

Enhancement Directions

-

Optimize S/R parameters

Find more reliable factors by tweaking generalized S/R settings

-

Optimize profit-taking

Add more profit levels, or use non-fixed targets

-

Optimize stop loss

Adjust ATR parameters or use istics stop loss to reduce unnecessary stops

-

Incorporate trend and other factors

Add trend filters like moving average to avoid big trend conflicts; also add other assisting factors

Summary

The core of the strategy is to capture decent mid-term swings via reversal trading. The logic is simple and direct, and can be practical with parameter tuning. But the aggressive nature of reversals leads to some drawdown and trapping risk. Further enhancements in stop loss, profit-taking and trend alignment will help reduce unnecessary losses.

- 1