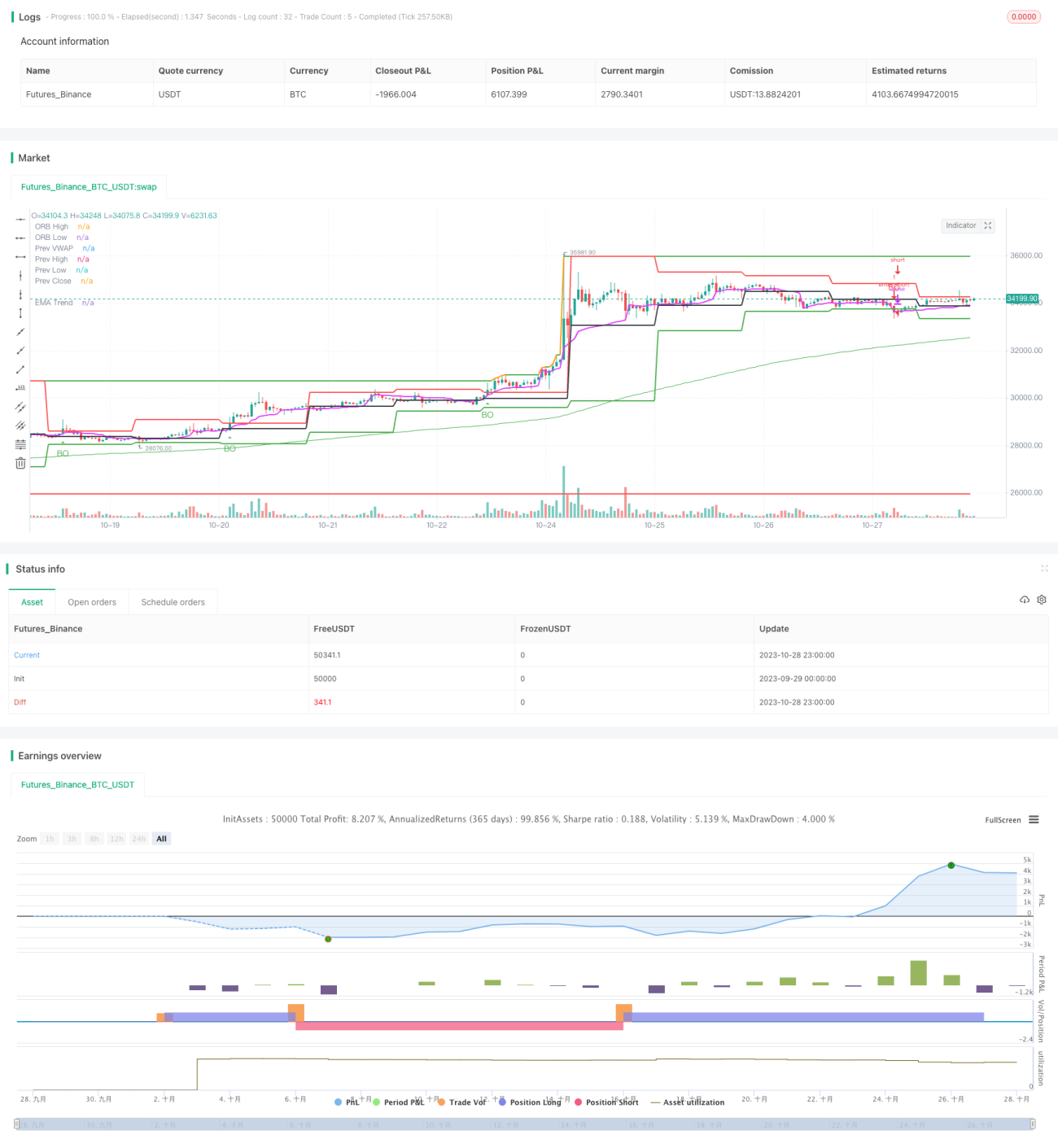

Trend-Following Strategy Based on Moving Average Breakout

Overview

The core idea of this strategy is to follow the trend by detecting breakouts of moving averages across higher timeframes. When the price breaks out above or breaks down below the moving average on a higher timeframe, it signals the potential start of a new trend, allowing traders to take positions accordingly.

Strategy Logic

The strategy is developed in Pine Script and consists of the following main components:

-

Inputs

Defines input parameters period as the moving average period, default to 200; and timeframe as the bar timeframe, default to D (daily bars).

-

Moving Average

Calculates exponential moving average (EMA) using ta.ema function.

-

Breakout Detection

Identifies breakouts and breakdowns using ta.crossover and ta.crossunder functions.

-

Signal Plotting

Plots up and down arrows on bars when breakouts occur.

-

Trade Entries and Exits

Enters trade on breakout signals and exits when price reaches 2x stop loss distance.

The strategy mainly leverages the trend-following capacity of moving averages across higher timeframes. It implements simple breakout logic for trend trading, making it a conventional breakout strategy.

Advantage Analysis

The main advantages of this strategy include:

-

Simple logic, easy to understand and master.

-

Depends on only one indicator, with minimal parameter tuning.

-

Breakout signals tend to align with trend, avoiding excessive trading.

-

Higher timeframes clearly depict major trends without noise.

-

Flexible timeframe combinations cater to different products.

-

Easily scalable across products, avoiding simultaneous drawdowns.

Risk Analysis

The potential risks are:

-

Breakout signals may turn out to be false signals, unable to filter market noise effectively.

-

Unable to capitalize on short-term opportunities.

-

Massive losses if major trend direction is wrong.

-

Timeframe mismatch between moving average and trading timeframe may lead to over-trading or missed profit.

-

Lack of real-time stop loss may result in magnified losses.

Possible solutions include combining with trend-following indicators, adding filters, shortening holding period, implementing dynamic stop loss etc.

Enhancement Opportunities

The strategy can be improved in the following aspects:

-

Add trend-following indicators like MACD, KD to increase breakout reliability.

-

Add filters based on volume or Bollinger Bands to avoid false breakouts.

-

Optimize parameter tuning to match holding period with trend cycle.

-

Incorporate real-time stop loss to control single trade loss.

-

Explore machine learning techniques for dynamic parameter optimization.

-

Test various asset allocation combinations to enhance overall stability.

Conclusion

In summary, this is a simple and practical strategy for trend-following via moving average breakouts. It is easy to understand and implement, serving as a good introductory strategy for algo trading. But it also has some flaws that need to be addressed through combinations of indicators, parameter tuning, dynamic stop loss etc. Much room remains for enhancements and extensions.

- 1