Ehlers Leading Indicator Trading Strategy

Overview

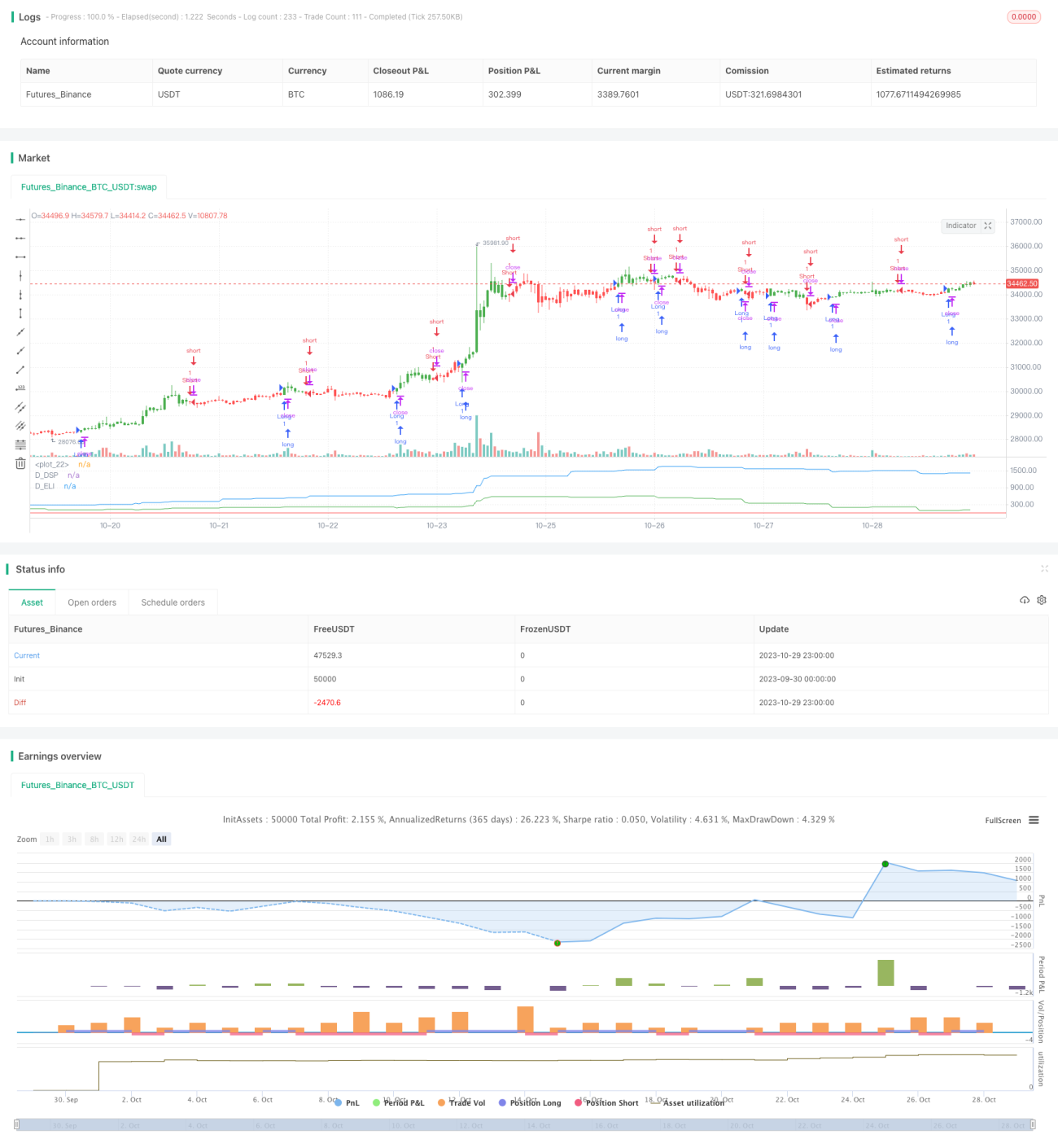

This strategy is based on the ideas of technical analysis master John Ehlers, using the Ehlers Leading Indicator to judge the historical cycle of prices and generate buy and sell signals. The strategy combines the detrended synthetic price and the Ehlers Leading Indicator, generating trading signals when the indicator line crosses over the detrended synthetic price.

Strategy Principle

The strategy first calculates the Detrended Synthetic Price (DSP), which is obtained by subtracting the value of a 3rd order Butterworth filter from a 2nd order Butterworth filter to get a function that is in phase with the dominant cycle of real price data.

Then it calculates the Ehlers Leading Indicator (ELI), which is obtained by subtracting the simple moving average of the detrended synthetic price from the detrended synthetic price itself, and can give advanced indication of a cyclic turning point.

Finally, when the ELI line crosses over the DSP, buy and sell signals are generated. If ELI crosses above DSP, a buy signal is generated. If ELI crosses below DSP, a sell signal is generated.

Advantage Analysis

The biggest advantage of this strategy is using the Ehlers Leading Indicator to judge turning points in price trends ahead of time. It allows entering positions before prices start to reverse, thus capturing larger profit potential.

In addition, combining the detrended price for trade signal generation filters out irrelevant low frequency information in prices, making the strategy more focused on cyclical patterns in prices without being disturbed by short-term market noise.

Risks and Optimization

The main risk of this strategy is the possibility of ELI incorrectly identifying signals, resulting in premature entry and losses. This can be optimized by adjusting indicator parameters to fine-tune indicator sensitivity.

Traders should also note this strategy only applies to products with obvious cyclical patterns. It would be less effective for products with chaotic price movements. Proper evaluation of a product's cyclicality is advised before using this strategy.

Risks can be managed by confirming signals with other indicators, or adjusting position sizing and stop loss strategies. For example, setting stop loss orders, reducing position sizes etc.

Summary

This strategy identifies cyclicality in prices using the Ehlers Leading Indicator, entering positions early before new cycles start, making it a typical trend following strategy. It is very effective for products with clear cyclicality, but also carries certain risks of false signals. Optimization through parameter tuning and risk management can make the strategy more robust.

/*backtest

start: 2023-09-30 00:00:00

end: 2023-10-30 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 23/03/2017

// This Indicator plots a single- 1