Dynamic RSI Oscillation Trading Strategy

Overview

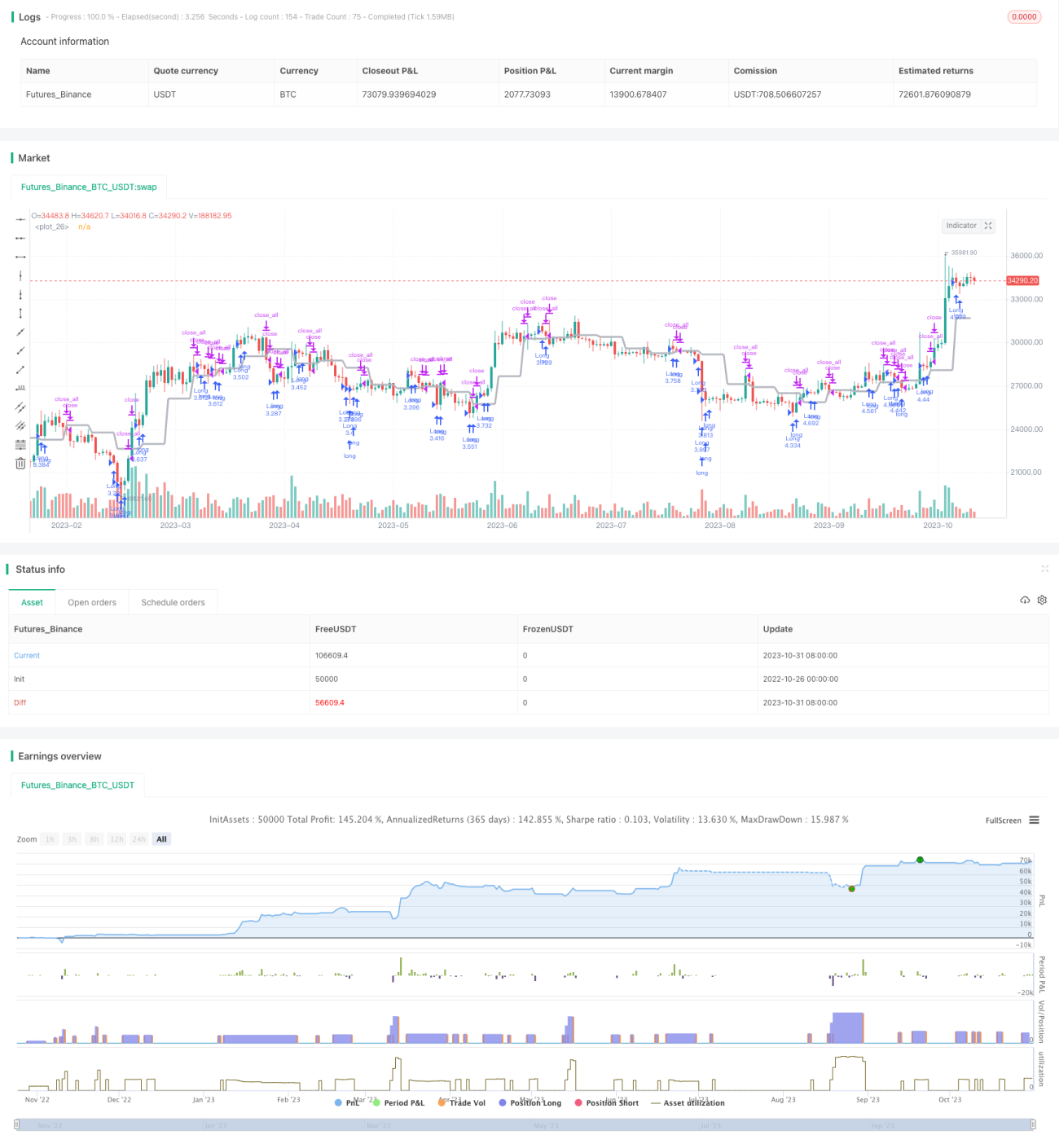

This strategy combines dynamic support/resistance levels and the relative strength index (RSI) indicator. It sets overbought/oversold thresholds for RSI and generates buy/sell signals when price breaks the dynamic support/resistance levels while RSI is not in the overbought/oversold area.

Principles

1. Dynamic Support/Resistance

Use the security function to get closing price as dynamic support/resistance levels. Trading signals are generated when price breaks through these dynamic levels.

2. RSI Indicator

Calculate the average gain and average loss over a certain period to generate RSI values and determine if RSI reaches the overbought/oversold area.

3. Trading Signals

When price breaks the dynamic levels, if RSI is not in the overbought/oversold area, buy/sell signals are generated. Otherwise, the breakout signals are ignored.

4. Exit Signals

Close positions when price falls back to the dynamic level, or when RSI returns to normal range.

Advantage Analysis

-

Use dynamic support/resistance to determine trend direction for higher winning rate.

-

RSI filters out false breakouts and avoids false entries.

-

Combining trend and indicator makes the strategy adaptable to different market conditions.

-

Simple and clear rules make it easy to implement.

Risks and Solutions

-

Multiple tests of dynamic levels may generate false signals. Widen the breakout range to filter.

-

Solo RSI may cause misjudgement. Add other indicators for combo filtering.

-

Frequent trading in range-bound market leads to higher costs. Widen RSI's normal range to lower frequency.

-

Improper parameter settings lead to missing or false signals. Optimize parameters based on different assets.

Optimization Directions

-

Use machine learning to auto optimize RSI parameters.

-

Add stop loss/profit taking strategy to lock in profits and reduce losses.

-

Incorporate more indicators for combo filtering to improve stability.

-

Add volatility indicator to lower position size when volatility is low.

-

Optimize position sizing algorithm to dynamically adjust positions for different market environments.

Summary

This strategy combines trend judgment and indicator filtering to effectively identify trend reversal around key levels while controlling risks. Further optimizations on parameter tuning, stop loss/profit taking, more indicators etc. can improve its stability and adaptability to generate steady profits in a wider range of markets.

- 1