Trend Tracking Strategy Based on Momentum Breakout

Overview

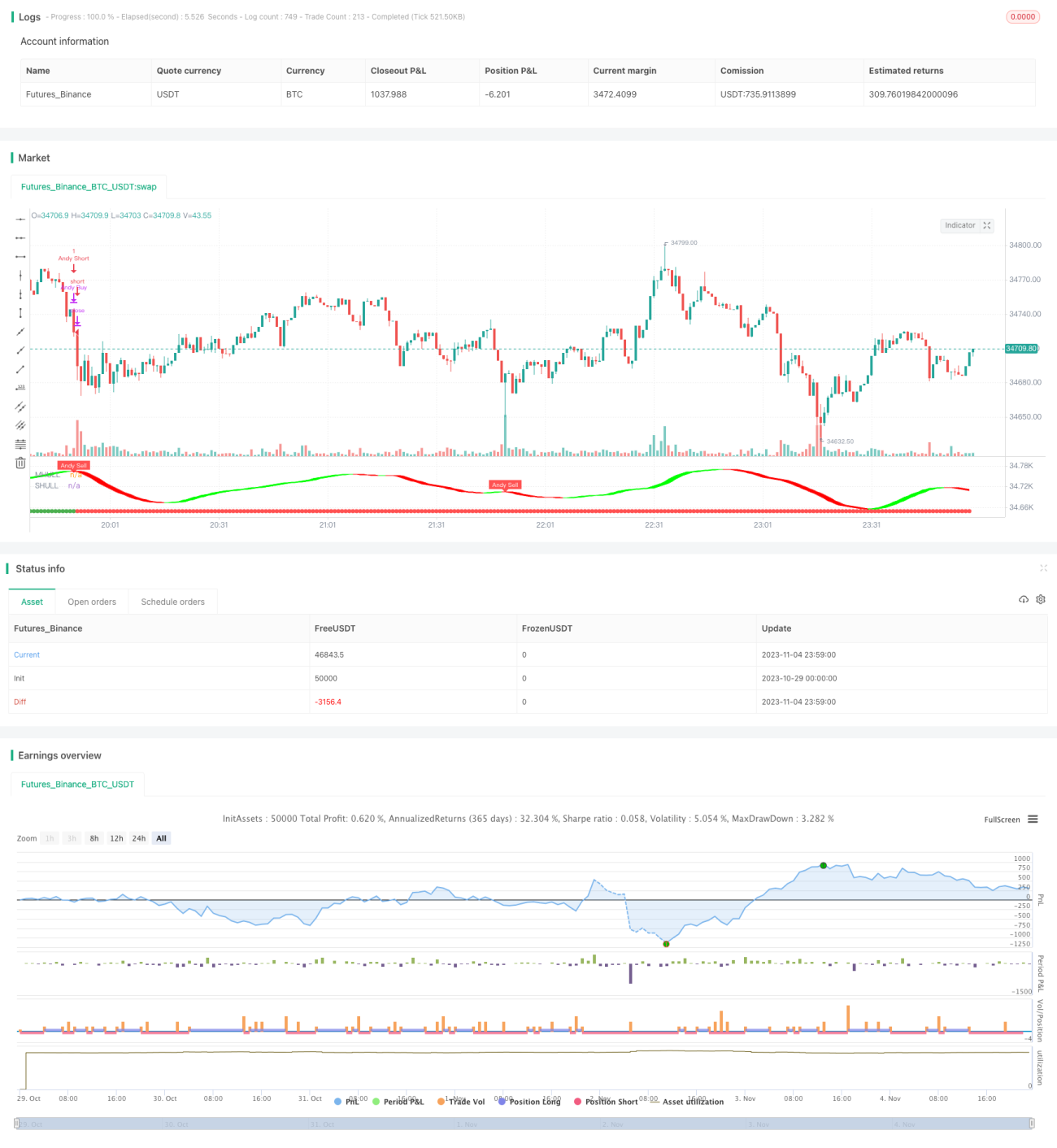

This strategy combines multiple technical indicators to identify trend direction and track the momentum when breakout happens, aiming for excess return.

Strategy Logic

-

Use Donchian Channel to determine the overall trend. A breakout of the channel confirms trend reversal.

-

Hull Moving Average assists in judging trend direction. It is sensitive to price change and can early detect trend reversal.

-

Halftrend system generates buy and sell signals based on price channel and ATR range. It avoids false breakout.

-

When Donchian, Hull and Halftrend signals align, a strong momentum breakout is confirmed and strategy enters.

-

Exit when above indicators give reverse signal, indicating trend reversal.

Advantage Analysis

-

More robust signal with multiple indicators. Donchian for fundamentals, Hull and Halftrend for details. Catch trend turning points accurately.

-

Pursuit of excess return by momentum breakout. Only enter on strong breakout, avoiding whipsaw in consolidation.

-

Strict stop loss to ensure capital safety. Loss is capped once reverse signal shows.

-

Flexible parameter tuning for different markets. Channel length, ATR range etc can be adjusted and optimized.

-

Easy to understand and implement. Indicator combo is simple and clear, easy to code.

Risk Analysis

-

Miss early trend opportunity. Entry is relatively late, early rally is not captured.

-

Loss from failed breakout and reversal. Drawdown may occur after entry.

-

False signal from bad parameter. Indicators may fail due to bad tuning.

-

Limited trade frequency. Only clear breakouts are traded, resulting in low annual trade numbers.

Optimization Directions

-

Optimize parameter combinations by testing. Find best parameters.

-

Add trailing stop loss condition. Avoid premature stop loss.

-

Introduce more filters like MACD, KDJ. To filter bad signals.

-

Optimize parameters for different sessions. Different sessions can be tuned separately.

-

Improve capital efficiency via leverage, DCA etc. Better capital utilization.

Summary

This strategy combines multiple indicators to identify momentum breakout of established trend, and profit from trend tracking. Strict stop loss manages risk. Flexible parameters adapt to different market environments. Although trade frequency is low, each trade targets high profitability. The strategy can be improved continuously through parameter tuning, additional filters etc.

- 1