Yesterday's High Breakout Strategy

Overview

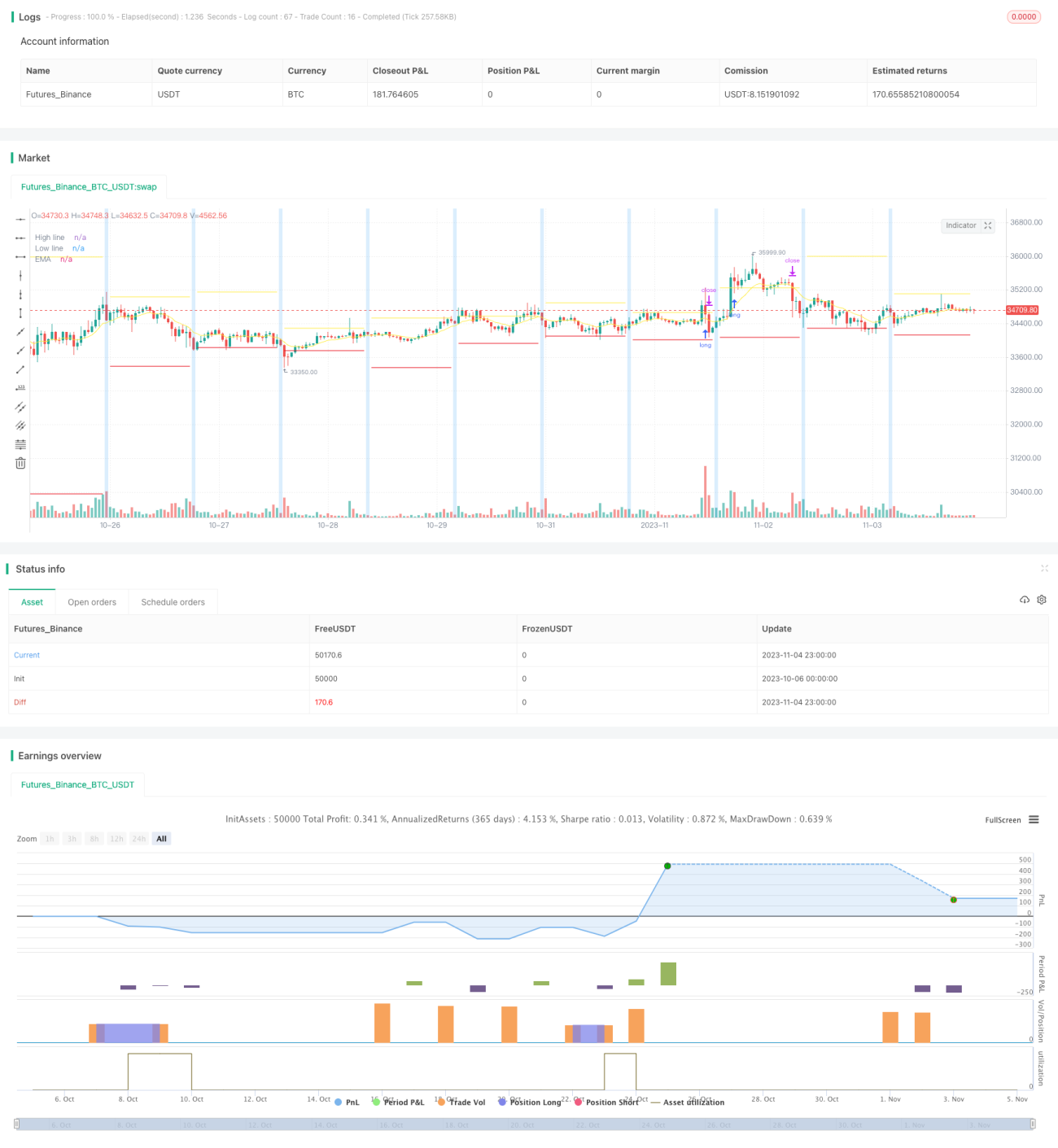

The Yesterday's High Breakout strategy is a trend following system that goes long when the price breaks above yesterday's high, even if the breakout occurs multiple times in a day. It aims to follow the trending market conditions.

Principle

The strategy employs several technical indicators for entry and exit signals:

-

ROC Filter - Strategy is enabled only when today's close has a price change percent above a threshold versus previous day's close. This filters non-trending volatile markets.

-

Trigger Point - Records today's high, low and open prices. Long entry triggered when price breaks above today's high.

-

Entry and Exit Conditions - After entry, stop loss and take profit percentages are set. Trailing stop can be enabled to lock in profit. Conditional exit when price drops below a reference EMA.

-

Configuration - Gap percent to anticipate or delay entry. Customizable stop loss, take profit, trailing stop percentages.

Specifically, it tracks today's high price for entry signal. Long entry when price breaks above today's high. Then stop loss and take profit exits are set, with trailing stop enabled. Alternate exit when price crosses below given EMA. Optimization by setting gap percentage, adjusting stop loss and take profit ratios to control risk, enabling trailing stop to lock in profit.

Advantage Analysis

The advantages of this strategy:

-

Trend following, captures profit from trending moves.

-

Breakout strategy gives clear entry signals.

-

Considers today's high price, avoids consecutive entries.

-

Stop loss and take profit helps risk control.

-

Trailing stop locks in profit.

-

Entry timing can be tuned with parameter optimization to control risk.

-

Simple and intuitive, easy to understand and implement.

-

Applicable for long and short trades.

Risk Analysis

The risks to consider:

-

Breakout strategies susceptible to whipsaws. Price may immediately reverse after entry.

-

Only effective for trending markets, underperforms in ranging conditions.

-

Reasonable stop loss percent needed, too wide may increase loss.

-

Reasonable gap percent needed, too aggressive may increase loss.

-

False breakout can cause unnecessary loss, tuning required.

-

Volume needs to support follow through after breakout.

-

Consistency needed between parameters across timeframes.

Optimization Directions

Possible optimizations:

-

Add other indicators like volume, volatility to avoid whipsaws during ranging markets.

-

Add curve fitting indicators to qualify trend strength, avoid false trends.

-

Dynamic optimization of entry gap based on market volatility.

-

Dynamic optimization of stop loss and take profit following market conditions.

-

Different parameter sets for different symbols and timeframes.

-

Machine learning to TEST parameter impact on strategy performance.

-

Add Options functionality to optimize configurations.

-

Research applicability during ranging market conditions.

-

Expand to cross timeframe and multi-asset strategies.

Conclusion

The strategy offers decent performance during trending markets based on breakout of yesterday's high concept. But risks of whipsaw and parameter optimization difficulties exist. Further optimizations possible by adding judgments, dynamic parameter tuning, expanding to combined strategies etc. Overall it suits short term trend following, but risk control and parameter tuning needed.

/*backtest

start: 2023-10-06 00:00:00

end: 2023-11-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Author: © tumiza 999

// © TheSocialCryptoClub

- 1