Dual-track Trend Capturing Fusion Strategy

Overview

This strategy fuses the 123 Reversal and SMA Ergodic Oscillator sub-strategies to form a trend tracking strategy with dual-track signal filtering. The 123 Reversal strategy judges potential turning points through candlestick patterns; the SMA Ergodic Oscillator determines trend direction using moving averages. They verify each other to form a dual confirmation mechanism, which can effectively filter out false signals and capture relatively strong trend directions for trend tracking trading.

Strategy Logic

- 123 Reversal Strategy

This strategy is from the system on p183 of Ulf Jensen's book "How I Tripled My Money in the Futures Market". It belongs to the reversal type. When the closing price is higher than the previous close for 2 consecutive days, and the slow line of the 9-day stochastic is below 50, go long; when the closing price is lower than the previous close for 2 consecutive days, and the fast line of 9-day stochastic is above 50, go short.

- SMA Ergodic Oscillator

This indicator is similar to the TSI developed by William Blau, except that SMA oscillator contains a signal line. The SMA Ergodic Indicator uses double moving averages of price minus previous price, and plots an EMA of SMI as signal line to trigger trading signals. The parameters are adjustable for optimization.

Dual confirmation: open positions only when 123 Reversal and SMA Ergodic give signals in the same direction. Keep flat when the signal directions are inconsistent.

Advantages

-

Integration of multiple indicators forms dual confirmation mechanism, which can effectively filter out false signals.

-

123 Reversal strategy judges potential reversal points through candlestick patterns. SMA Ergodic Oscillator issues signals based on trend judgment. They complement each other to overcome the limitations of single indicators.

-

The parameters of SMA Ergodic Oscillator are adjustable for optimization on different products and timeframes. It is flexible.

-

As a whole trend tracking strategy, it can follow the trend continuously to capture strong momentum.

Risks

-

The integration and balance between reversal and trend strategies needs continuous optimization, otherwise it may miss turning points or cause huge losses.

-

Reversal strategies have inherent false trading risks. Parameters need to be adjusted to reduce failure rate.

-

Pure trend following strategies cannot judge reversals. There are potential loss risks. Position size should be reduced in time to avoid risks.

-

Parameters need iterative optimization and testing for different products and timeframes. Do not directly apply them.

Enhancements

-

Adjust parameters of 123 Reversal to reduce false trading frequency.

-

Adjust parameters of SMA Ergodic Oscillator to optimize indicator sensitivity.

-

Add stop loss strategy to limit per trade loss.

-

Incorporate other indicators to judge potential reversals and reduce position size in time.

-

Test parameters on different products to improve robustness.

Summary

This strategy integrates the advantages of reversal and trend strategies through dual confirmation mechanism, forming strong trend tracking effect. It can effectively filter out noise, follow the trend, and continuously capture high quality trend opportunities. Meanwhile, certain drawdown risks exist. Parameters need continuous optimization and risk control using stop loss. The key is balancing reversal and trend, plus stop loss. It may work better for long term tracking. Overall, this strategy has practical value, and can be used as part of strategy portfolio, or independently.

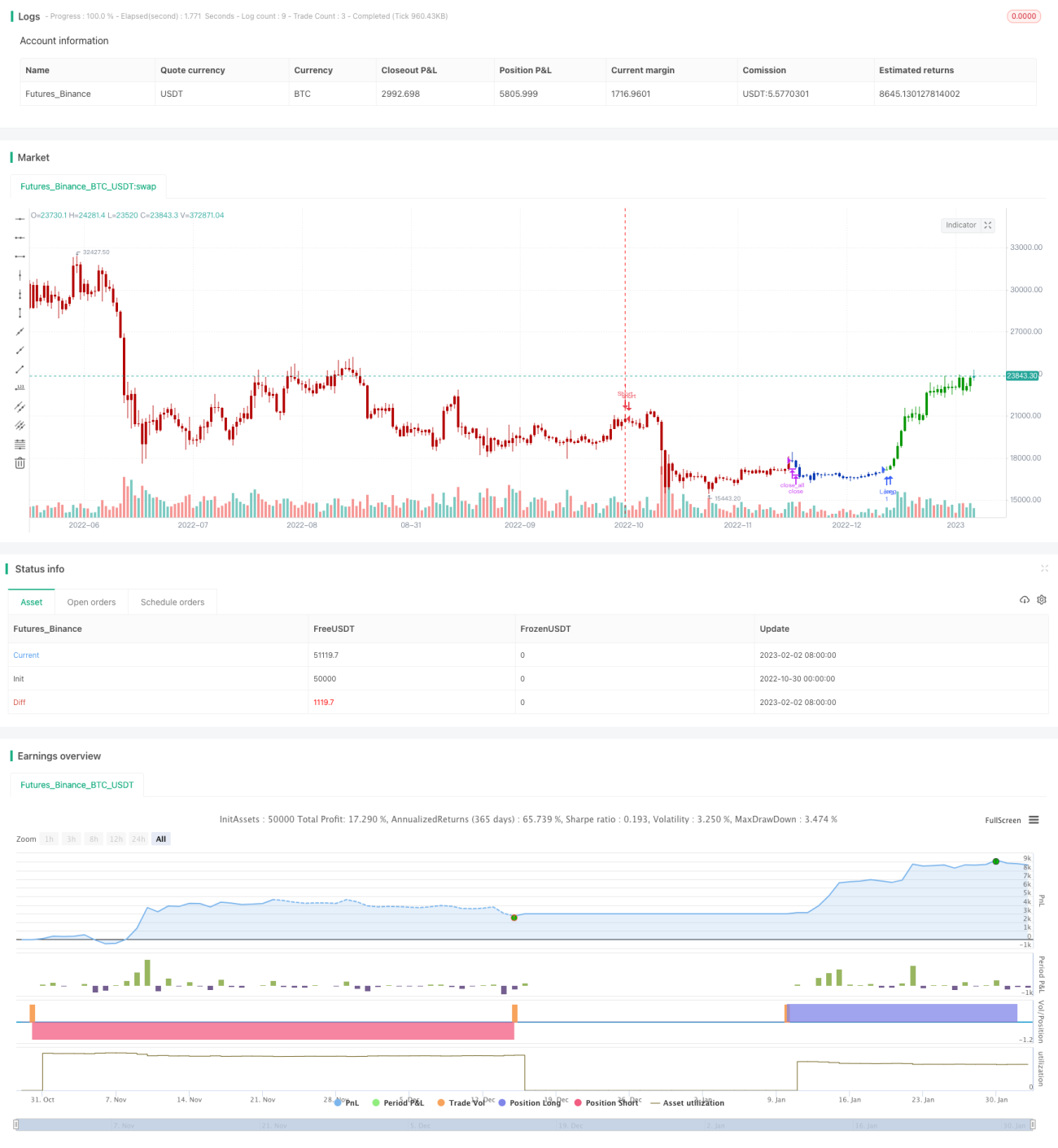

/*backtest

start: 2022-10-30 00:00:00

end: 2023-02-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 14/07/2021

// This is combo strategies for get a cumulative signal. - 1