Multi Timeframe Moving Average Momentum Trading Strategy

Overview

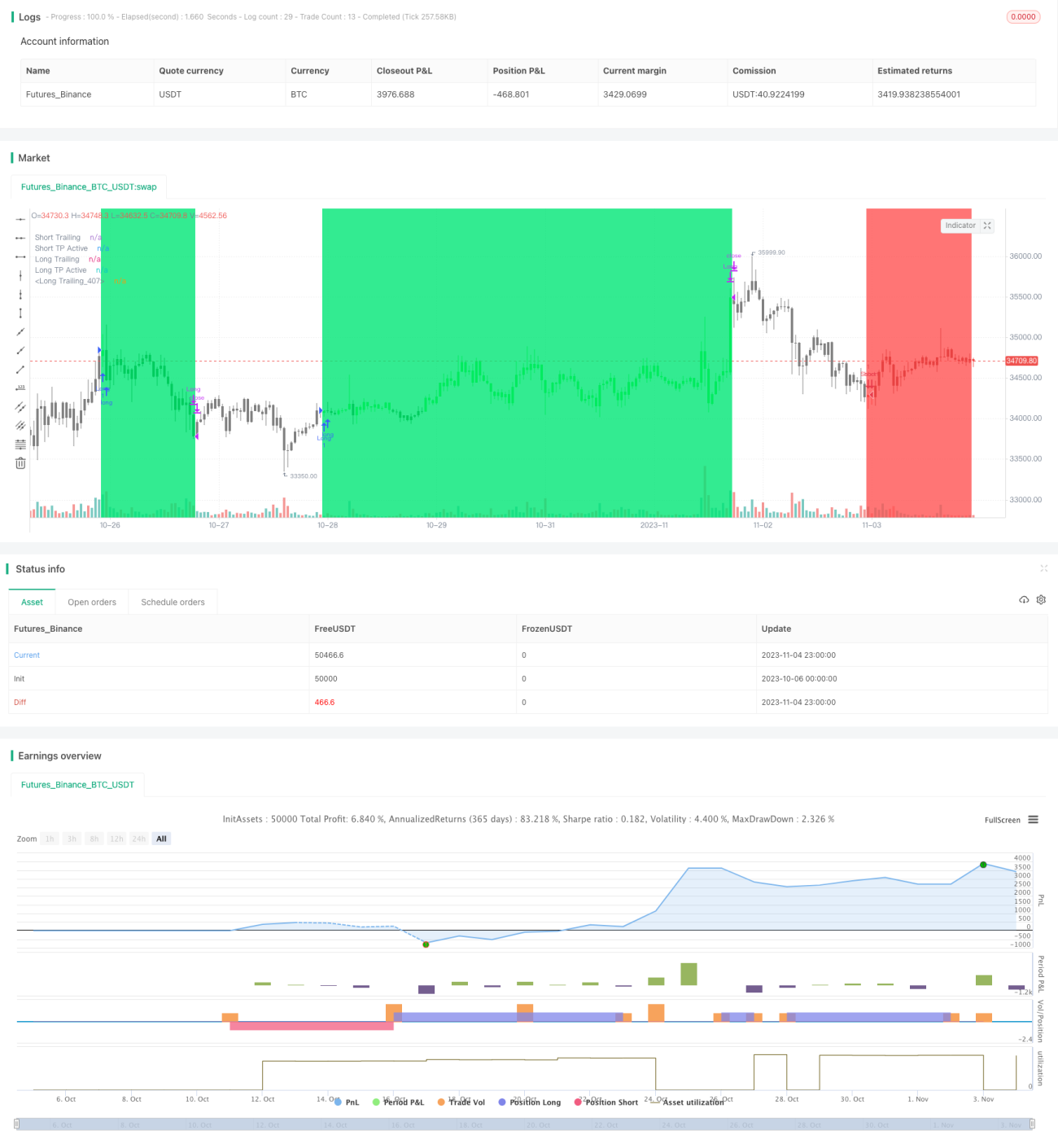

This trading strategy combines multiple moving averages and momentum indicators to identify the direction and strength of trends, establishing positions early in emerging trends, and then optimizing profit and risk management through the use of trailing stops and take profits. It aims to capture significant price swings during sustained trends.

Strategy Logic

-

Two sets of moving averages with different parameters are constructed to create fast and slow lines:

- Fast line consists of 5-period EMA and 25-period WMA, representing short-term trend

- Slow line consists of 28-period EMA and 72-period WMA, representing mid- to long-term trend

-

When fast line crosses above slow line, it signals short-term trend is gaining strength over mid-term trend, and presents entry signal.

-

RSI filter incorporated, only taking entries at RSI lows (for long) and RSI highs (for short) to avoid false breakouts.

-

Once entered, trailing stop used to minimize losses, while take profit locks in gains.

-

When fast line crosses below slow line, it signals trend reversal, prompting exit via stop loss or take profit.

Advantage Analysis

- Dual moving average combinations filter noise and identify trend direction & strength during trend progression.

- Entries established early in emerging trends avoids unnecessary losses from false breakouts.

- RSI filter improves quality of entries.

- Trailing stop compresses losses from individual losing trades.

- Take profit allows sizable profit capture during favorable moves.

Risk Analysis

- Dual moving averages can lag at turning points, missing reversal opportunities.

- Shorten moving average periods for greater sensitivity.

- False breakouts lead to unnecessary entries.

- Incorporate more filters before entry.

- Stop loss / take profit distances not optimized, may be too wide or too narrow.

- Optimize via backtest to find optimal levels.

- Directional strategy only works for trending markets.

- Only employ strategy based on market conditions.

Optimization Directions

- Optimize moving average parameters to find best representations of trend.

- Add trend filters like dynamic ATR stop, momentum oscillators etc.

- Optimize stop loss / take profit parameters.

- Incorporate regime filters based on market conditions.

- Add cross-timeframe analysis using higher timeframes to guide shorter-term strategy direction.

Summary

This strategy integrates moving averages and momentum indicators to identify and establish early entries during emerging trends, while managing risk and reward via timely stops and take profits. Although further parameter and logic optimization is needed to adapt to wider market conditions, it already has a basic framework and directionality for capturing mid- to long-term trends. With continual improvements, this strategy can potentially grow into a robust, efficient trend-following system.

- 1