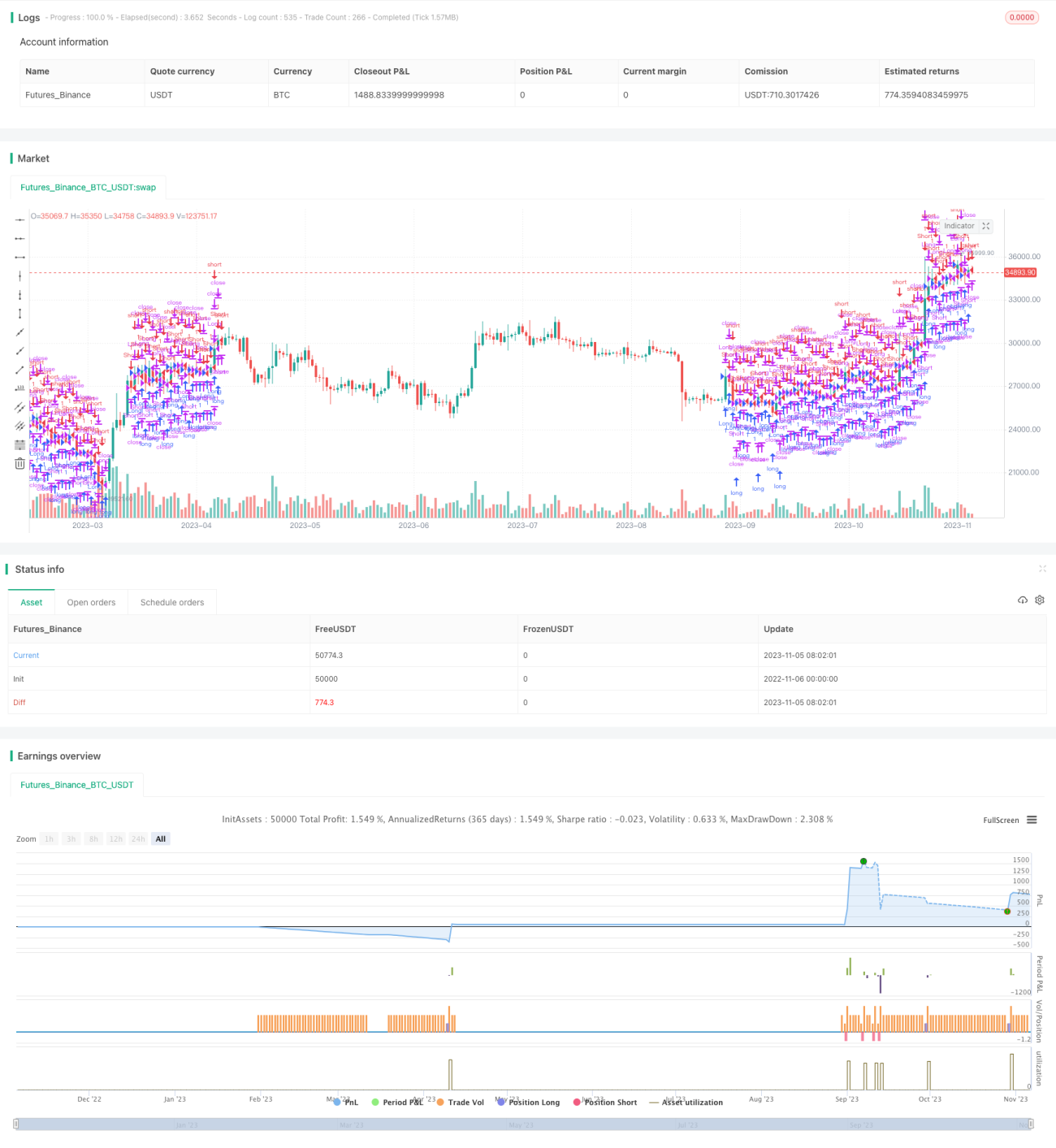

概述

本策略的核心思想是在RSI策略的基础上,加入了一些关键的交易管理规则,包括止损、止盈、追踪止损,以及杠杆追踪止损。这使得策略在回测期间能够在趋势行情中获得更高收益,同时在震荡行情中尽量减少亏损。

策略原理

该策略首先计算RSI指标,当RSI低于超买线时做多,当RSI高于超卖线时做空。

做多信号触发后,记录该时刻的最高价作为追踪止损的参考点。如果价格低于追踪止损点减去止损幅度,则止损平仓。

做空信号触发后,记录该时刻的最低价作为追踪止损的参考点。如果价格高于追踪止损点加上止损幅度,则止损平仓。

同时设置固定止盈和止损距离。如果价格达到止盈距离,则止盈清仓;如果达到止损距离,则止损清仓。

另外,根据杠杆设置杠杆追踪止损线。如果价格触及杠杆追踪止损线,则清仓止损。

通过在趋势向上时追踪最高价止损,趋势向下时追踪最低价止损,结合固定止盈止损距离,可以在趋势行情中获得更高收益。同时设置杠杆追踪止损可以尽量避免亏损扩大。

优势分析

该策略最大的优势在于引入了多个交易管理规则,在发挥RSI策略优势的同时,可以更好地控制风险。

具体来说,策略的优势有:

-

在趋势行情中,追踪止损可以持续跟踪趋势获利,从而获得更高收益。

-

固定止盈止损距离可以锁定部分利润,避免全部盈利在趋势反转时被套牢。

-

杠杆追踪止损可以尽量避免亏损扩大,控制风险。

-

多种止损方式的结合可以在不同市场环境中发挥各自的优势,整体上提高策略的稳定性。

-

策略参数可以灵活调整,适应不同交易品种和市场环境。

-

策略逻辑清晰易理解,便于验证、优化和应用。

风险分析

该策略的主要风险来源于:

-

RSI策略本身存在一定的错交易风险,可能出现止损被触发的情况。可以通过调整RSI参数来优化。

-

在止损点附近震荡可能频繁触发止损。可以适当扩大止损距离来避免。

-

止盈距离无法完全锁定趋势行情中的利润。可以结合其它指标判断趋势结束时机。

-

固定止损距离可能过小,无法完全避免亏损。可以考虑采用振荡止损或动态止损。

-

杠杆过高可能导致杠杆追踪止损过于靠近开仓价格。应适当降低杠杆设置。

-

回测时间范围无法完全代表未来市场行情。应做好风险控制,并验证不同时间段的效果。

以上风险可以通过参数调整、优化止损机制、风险控制等方式得到缓解。但任何策略都无法完全规避市场风险,需做好风险控制。

优化方向

该策略可以从以下几个方向进行进一步优化:

-

优化RSI参数,降低错交易概率。可以测试不同市场的最优参数组合。

-

尝试其他指标判断入场时机,如KD,MACD等,结合RSI形成多重过滤。

-

利用机器学习等方法动态优化止损止盈参数。

-

尝试更复杂的止损方式,如振荡止损、平均止损、动态止损等。

-

优化杠杆水平的设置,不同杠杆对收益和风险控制的影响。

-

根据市场环境变化自动调整参数,如α-Dual Thrust。

-

结合其它因素判断趋势持续性,如交易量能量等。

-

利用深度学习等技术开发更稳定和可解释的止损方式。

-

测试不同品种和时段的数据,评估策略的稳健性。

总结

本策略在RSI策略基础上增加多种止损方式,充分发挥止损在趋势获利和风险控制中的双重作用。策略优化空间还很大,可以从多方面入手提高策略优势并降低风险。止损策略思想普适性强,可扩展到更多策略和交易品种中,是非常值得研究的方向。通过不断优化和验证,止损策略可以成为机械交易体系中极为重要的一环。

/*backtest

start: 2022-11-06 00:00:00

end: 2023-11-06 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Adding some essential components to a prebuilt RSI strategy", overlay=true)

/////////////// Component Code Start ///////////////- 1