Moving Average Trading Strategy

Overview

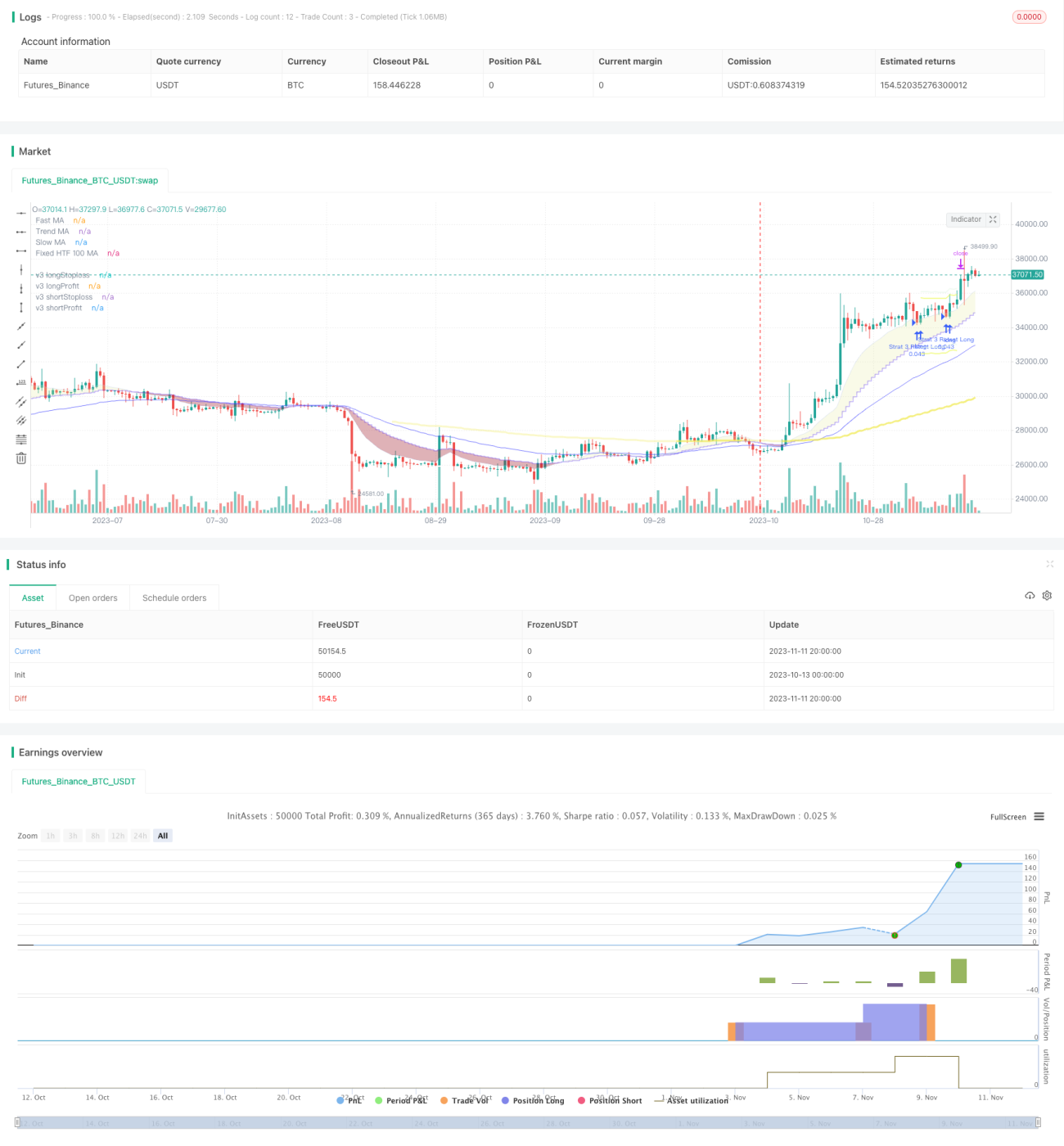

This strategy is based on moving average crossover system. By calculating moving averages of different periods and using crosses between them as trading signals, supplemented by RSI indicator for signal filtering, it improves profitability while lowering trading frequency.

Strategy Logic

-

Calculate fast, medium and slow moving averages. Fast MA and medium MA form the trading channel.

-

Go long when price crosses above fast MA, and go short when price crosses below fast MA.

-

Trend direction judged by: fast MA > medium MA is bullish, fast MA < medium MA is bearish. Only trade in the direction of the channel.

-

Slow MA acts as trend filter: only go long above slow MA and go short below slow MA.

-

RSI filter: only go long above RSI buy level and go short below RSI sell level.

-

ATR based stop loss and take profit.

Advantages

-

Flexible MA combinations adaptable to market changes.

-

RSI filter avoids false breakouts and improves signal quality.

-

ATR dynamic SL/TP lowers risk of maximum drawdown.

-

Dual filters by slow MA and RSI avoid unnecessary trades.

Risks

-

MA crossovers may lag price actions.

-

Dual filters may miss some trading opportunities.

-

ATR SL could exceed normal SL range.

-

Poor parameter tuning leads to too frequent or too sparse trades.

Corresponding risk management measures:

-

Use shorter MA periods to reduce lag.

-

Adjust filter parameters to maintain decent trade frequency.

-

Tune ATR multiplier to keep SL within acceptable range.

-

Optimize parameters to find the best combination.

Optimization Directions

-

Test combinations of different MA types.

-

Optimize MA periods.

-

Optimize RSI parameters.

-

Optimize ATR SL/TP coefficients.

-

Optimize filter parameters to find best filter strength.

Conclusion

This strategy combines MA, RSI and ATR, which through parameter optimization, can generate trading systems adaptable to different markets. Compared to single indicator strategies, it effectively reduces false signals and improves profitability. But no technical strategies can completely avoid market risks. Strict risk management practices are required as safeguards.

- 1