Dual-confirmation Reversal Trading Strategy

Overview

The dual-confirmation reversal trading strategy combines the 123 reversal pattern with the Stochastic RSI indicator to create a robust mean-reversion system. It provides two layers of confirmation before entering a trade, improving the strategy's accuracy and stability.

Strategy Logic

The strategy consists of two components:

- 123 Reversal

It uses the 123 pattern to identify potential reversals. The logic is:

-

Long if close < previous close and current close > previous close and 9-day Slow Stochastic < 50

-

Short if close > previous close and current close < previous close and 9-day Fast Stochastic > 50

This provides an early signal for price reversals.

- Stochastic RSI

It applies Stochastic indicator on RSI for additional confirmation:

-

Compute RSI with length 14

-

Calculate Stochastic of RSI, with lengths 14, to get K

-

Take 3-day SMA of K to get D

-

If K crosses above 80, it indicates long. If K crosses below 20, it indicates short.

A trade is triggered only when both parts agree.

Advantage Analysis

The key advantage of this strategy is the double confirmation, which improves accuracy and reduces whipsaws. Specific benefits include:

-

123 reversal provides early detection of trend reversal

-

Stochastic RSI confirms the reversal signal

-

Combination improves win rate and reduces false signals

-

Parameters can be optimized for different markets

-

Simple and clean implementation for live trading

Risk Analysis

Some risks to consider for this strategy:

-

Failed reversal risk. False reversals may cause losses.

-

Parameter optimization risk. Bad parameters lead to poor performance.

-

Overfitting risk. Excessive optimization to historical data.

-

High trading frequency risk. More signals may increase costs.

-

Coding error risk. Bugs in implementation logic.

Possible solutions:

-

Use prudent position sizing to limit losses.

-

Employ walk-forward optimization methods.

-

Focus on parameter stability, not high returns.

-

Tune conditions to reduce trade frequency.

-

Thoroughly test code logic.

Enhancement Opportunities

The strategy can be improved in the following areas:

-

Parameter tuning for specific markets.

-

Adding filters to avoid hasty reversals.

-

Incorporating stop loss mechanisms.

-

Reducing trade frequency with additional filters.

-

Implementing dynamic position sizing.

-

Adjusting for transaction costs.

Conclusion

The dual-confirmation reversal strategy is a stable and practical system for short-term mean-reversion. It balances the sensitivity to catch reversals and the accuracy from dual confirmation. With proper optimization and modifications, it can effectively complement a quantitative strategy portfolio. But parameters should be robust and risks like overfitting and whipsaws should be managed prudently in live trading.

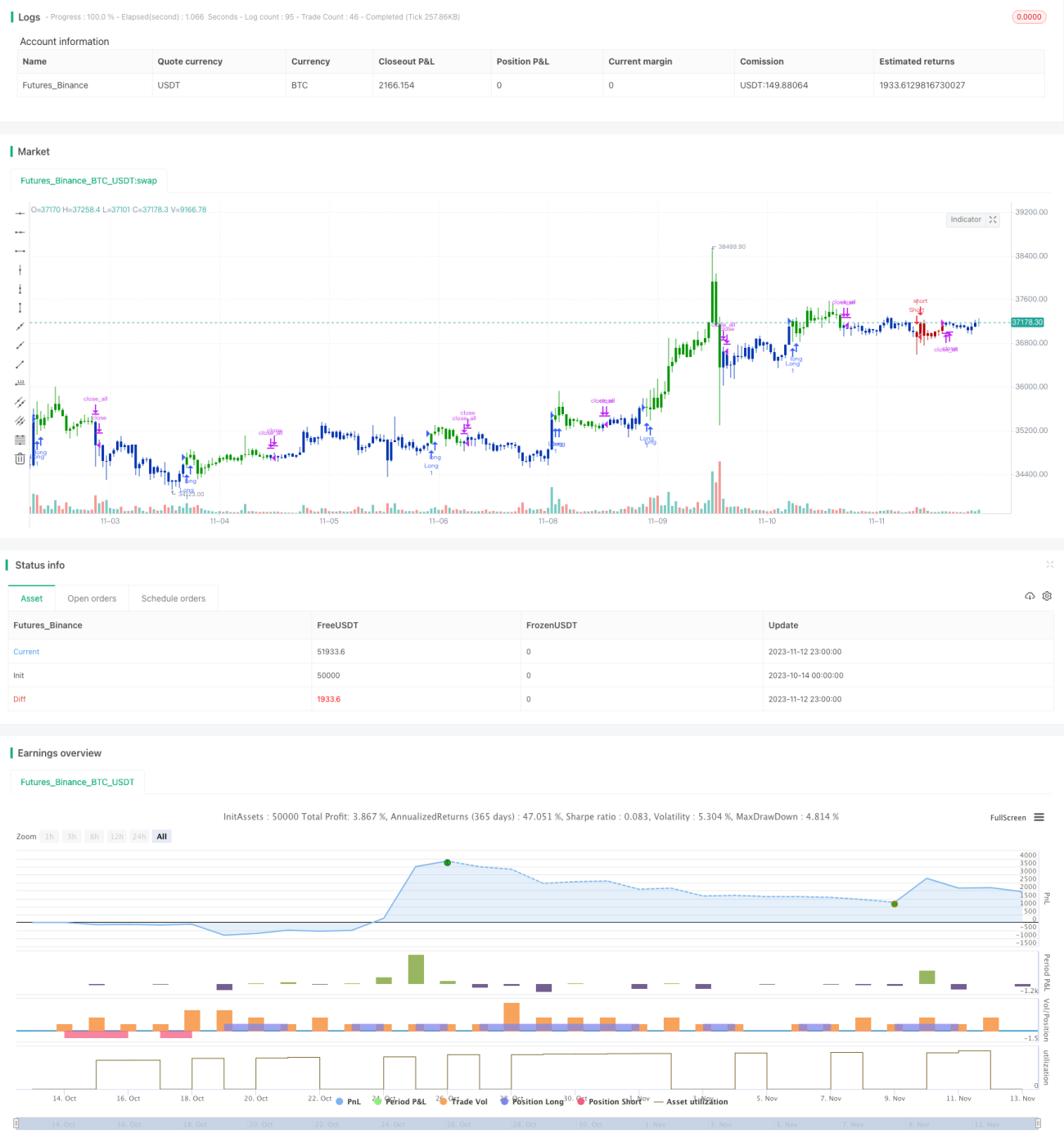

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 03/08/2021

// This is combo strategies for get a cumulative signal. - 1