Mean Reversion Momentum Strategy

Overview

The mean reversion momentum strategy is a trend trading strategy that tracks short-term price averages. It combines the mean reversion indicator and momentum indicator to judge the medium-term market trend.

Strategy Logic

The strategy first calculates the mean reversion line and standard deviation of the price. Then, combined with the threshold values set by the Upper Threshold and Lower Threshold parameters, it calculates whether the price exceeds the range of one standard deviation from the mean reversion line. If so, a trading signal is generated.

For long signals, the price needs to be below the mean reversion line by one standard deviation, the Close price is below the SMA of the LENGTH period, and above the TREND SMA, if these three conditions are met, a long position will be opened. The closing condition is when the price breaks above the SMA of the LENGTH period.

For short signals, the price needs to be above the mean reversion line by one standard deviation, the Close price is above the SMA of the LENGTH period, and below the TREND SMA, if these three conditions are met, a short position will be opened. The closing condition is when the price breaks below the SMA of the LENGTH period.

The strategy also combines Percent Profit Target and Percent Stop Loss for profit taking and stop loss management.

The exit method can choose between moving average crossover or linear regression crossover.

Through the combination of dual-directional trading, trend filtering, profit taking and stop loss, etc., it realizes the judgment and tracking of medium-term market trends.

Advantages

-

The mean reversion indicator can effectively judge the deviation of the price from the value center.

-

The momentum indicator SMA can filter out short-term market noise.

-

Dual-directional trading can fully capture trend opportunities in all directions.

-

The profit taking and stop loss mechanism can effectively control risks.

-

The selectable exit methods can be flexible to adapt to market conditions.

-

A complete trend trading strategy that better captures medium-term trends.

Risks

-

The mean reversion indicator is sensitive to parameter settings, improper threshold settings may cause false signals.

-

In volatile market conditions, stop loss may be triggered too frequently.

-

In sideways trends, the trading frequency may be too high, increasing trading costs and slippage risks.

-

When the trading instrument has insufficient liquidity, slippage control may be suboptimal.

-

Dual directional trading has higher risks, prudent money management is required.

These risks can be controlled through parameter optimization, stop loss adjustment, money management etc.

Optimization Directions

-

Optimize the parameter settings of mean reversion and momentum indicators to better suit different trading instruments.

-

Add trend identification indicators to improve trend recognition ability.

-

Optimize the stop loss strategy to better adapt to significant market fluctuations.

-

Add position sizing modules to adjust position sizes based on market conditions.

-

Add more risk management modules, such as maximum drawdown control, equity curve control etc.

-

Consider combining machine learning methods to automatically optimize strategy parameters.

Summary

In summary, the mean reversion momentum strategy captures mid-term mean reversion trends through simple and effective indicator design. The strategy has strong adaptability and versatility, but also has some risks. By continuous optimization and combining with other strategies, better performance can be achieved. Overall the strategy is quite complete, and is a trend trading method worth considering.

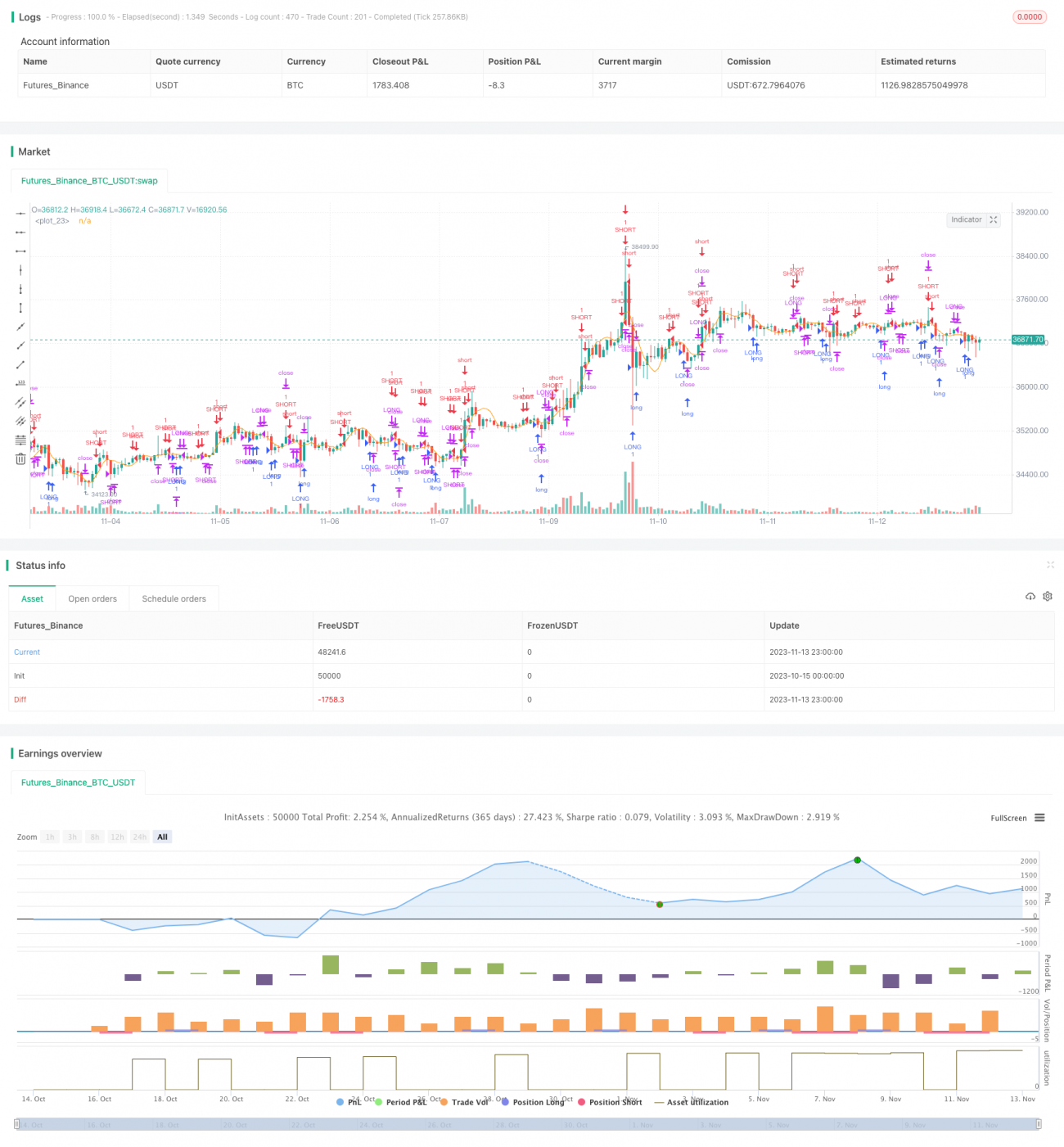

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlobalMarketSignals

//@version=4- 1