Multi Trend Strategy

Overview

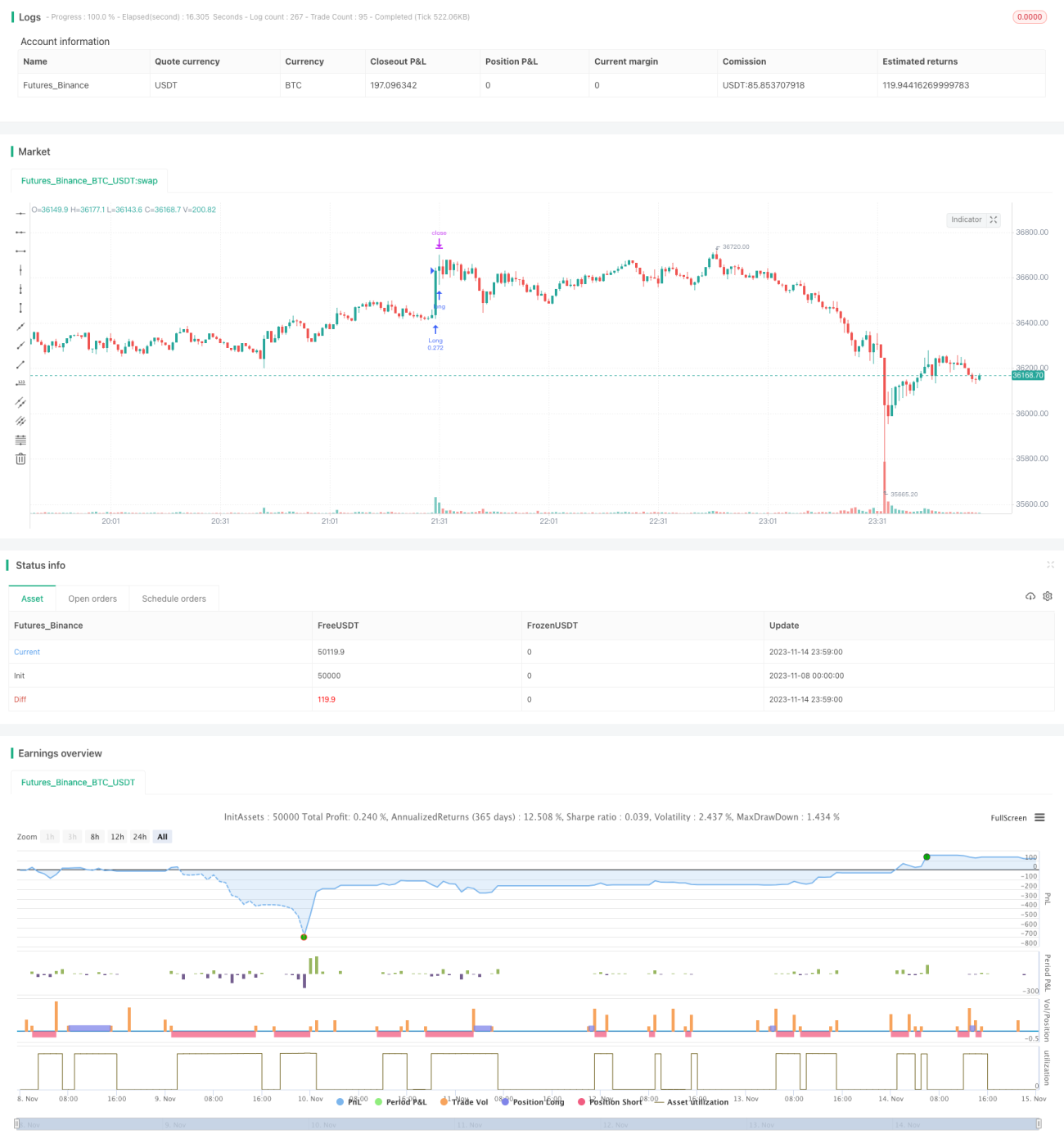

This strategy combines multiple indicators to identify trend direction and uses a trend tracking approach to capture trend opportunities over medium to short term. The strategy is designed specifically for trend tracking to increase win rate and reduce drawdown.

Strategy Logic

-

Use WVAP to judge price level;

-

RSI to judge momentum;

-

QQE to identify price breakthrough;

-

ADX to determine trend strength;

-

Coral Trend Indicator to judge fundamental trend;

-

LSMA to assist in trend judgment;

-

Generate signals based on multiple indicator signals.

The strategy mainly relies on RSI, QQE, ADX and other indicators to determine trend direction and strength, using Coral Trend Indicator curve as the benchmark for fundamental trend. When RSI generates a buy signal and Coral Trend Indicator shows an upward curve, it indicates high probability of uptrend, and the strategy will go long. WVAP is used mainly to determine if price level is reasonable to avoid buying at highs.

Advantages

-

Combination of multiple indicators improves accuracy;

-

Emphasizes trend tracking to increase profitability;

-

Adopts breakout concept to screen for ranging markets;

-

Incorporates fundamental indicators to avoid counter-trend trades;

-

Reasonable trade time and position sizing controls risk;

-

Clear strategy logic, easy to understand and optimize.

The biggest edge of this strategy is the combined signals from multiple indicators, which reduces the probability of misjudgment from any single indicator and improves accuracy. The emphasis on trend tracking and breakout concept also helps screen for reliable medium-term opportunities. In addition, incorporating fundamental indicators prevents trading against major trends. These design choices improve the stability and profitability of the strategy.

Risks

-

Judgment delay due to multiple indicators, missing best entry price;

-

Inadequate drawdown control, large drawdown risk;

-

Potential missed signals when fundamental trend reverses;

-

Profit deterioration risk when trading costs are considered.

The biggest risk is judgment delay due to multiple indicators, causing missed best entry price and profit potential. Also, drawdown control is far from ideal, with considerable drawdown risk. When fundamental trend reverses while indicators have yet to reflect it, losses may occur. Trading costs in actual deployment may also undermine profits.

Improvement Directions

-

Incorporate stop loss for better drawdown control;

-

Optimize parameters to reduce indicator delay;

-

Add more fundamental indicators to improve accuracy;

-

Use machine learning for dynamic parameter optimization.

Priorities for optimization include better drawdown control via stop loss to lock in profits and reduce drawdown. Parameter tuning to reduce indicator delay and improve responsiveness is also important. More fundamental indicators could also help improve accuracy. Applying machine learning for dynamic parameter optimization would significantly enhance strategy stability.

Summary

This strategy combines multiple indicators to determine trend direction and uses a trend tracking approach in its design to improve accuracy and profitability. Its strengths include indicator combos, emphasis on trend tracking, and incorporation of fundamental factors. But issues like judgment delay, inadequate drawdown control remain. Future improvements could come from parameter optimization, stop loss integration, more fundamental indicators, and machine learning for dynamic optimization, to make the strategy more effective in practice.

- 1