Quantized Gradual Weighted DCA Trading Strategy

Overview

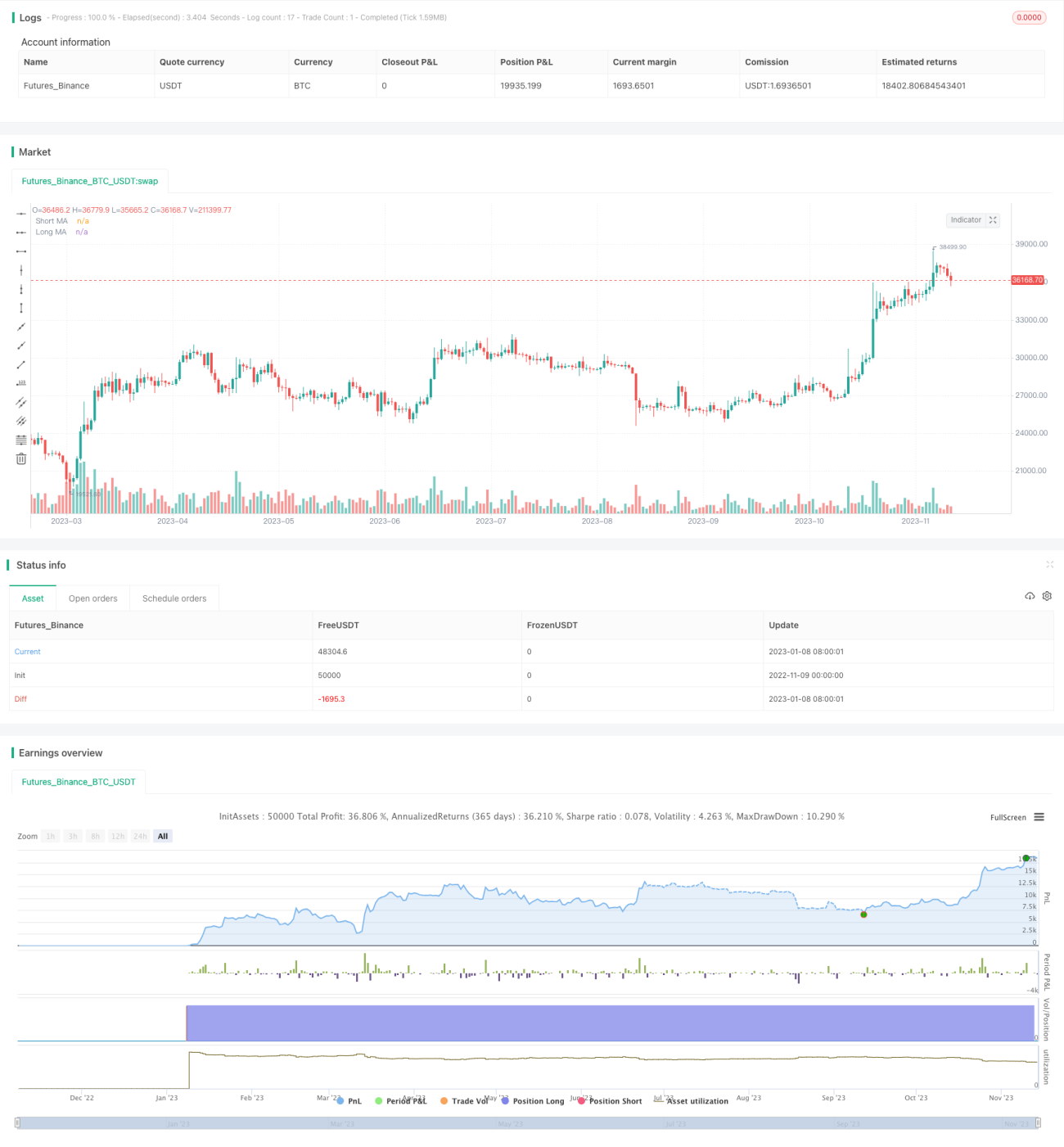

The Quantized Gradual Weighted DCA Trading Strategy is a quantitative trading strategy that combines moving average indicators for signal triggering and gradual weighted dollar cost averaging mechanisms. The strategy aims to achieve relatively stable returns in strongly trending markets through trend identification and cost averaging.

Principles

The strategy consists of three main components:

-

Entry signal judgement

It uses fast and slow moving average crossovers as the entry signal. Users can choose between SMA, EMA or HMA for the fast and slow moving averages. When the fast MA crosses above the slow MA, a buy signal is generated. When the fast MA crosses below the slow MA, a sell signal is generated.

-

Gradual weighted DCA

After a buy signal, the strategy will immediately open a base position. As price continues to fall, the strategy will gradually increase the size of additional safety positions in a weighted manner. The price of each new safety position will be lowered by a fixed percentage relative to the previous one. Also, the allocated funds for each new safety position will be amplified by a factor.

This gradual increase in position size allows a form of cost averaging, obtaining a better average cost while keeping risks in control.

-

Take profit and Stop loss

When price rises above the take profit line, the strategy will close positions for profit. When price falls below the stop loss line, the strategy will exit positions to control loss.

The take profit line is fixed at base position average price * (1 + fixed percentage).

The stop loss line fluctuates based on the last safety position price, fixed percentage below it.

Advantages

-

Combining trend and cost averaging makes it more stable

Using trends avoids meaningless whipsaws, and cost averaging provides better entry costs.

-

Gradual position sizing controls risk

Fixed amplification of safety position sizes, with re-entry threshold, keeps risk in check.

-

Real-time used funds monitoring

Incorporated balance usage indicator prevents over-leveraging and forced liquidations.

-

Separate TP/SL for each position

Independent exits allow securing profits and cutting losses.

Risks and Improvements

-

Price whipsaws can trigger multiple safety orders

In extreme volatility, multiple unnecessary safety orders may be added, increasing loss. Can optimize safety order re-entry threshold.

-

Moving average parameters need optimization

Different instruments need different moving average periods. Parameter tuning required.

-

TP/SL levels need backtest optimization

TP/SL ratios determine risk/reward profile. Optimal levels vary.

-

Add maximum drawdown or holding time based forced exit

Can test incorporating forced exits based on drawdown or holding time to further limit risks.

Summary

The Quantized Gradual Weighted DCA Trading Strategy combines the advantages of trend trading and cost averaging to produce steady returns in strong trends. With optimized parameters, position sizing and re-entry thresholds, it can achieve stable trades with controlled risk. Applicable for hedge funds, CTAs and market neutral strategies.

- 1