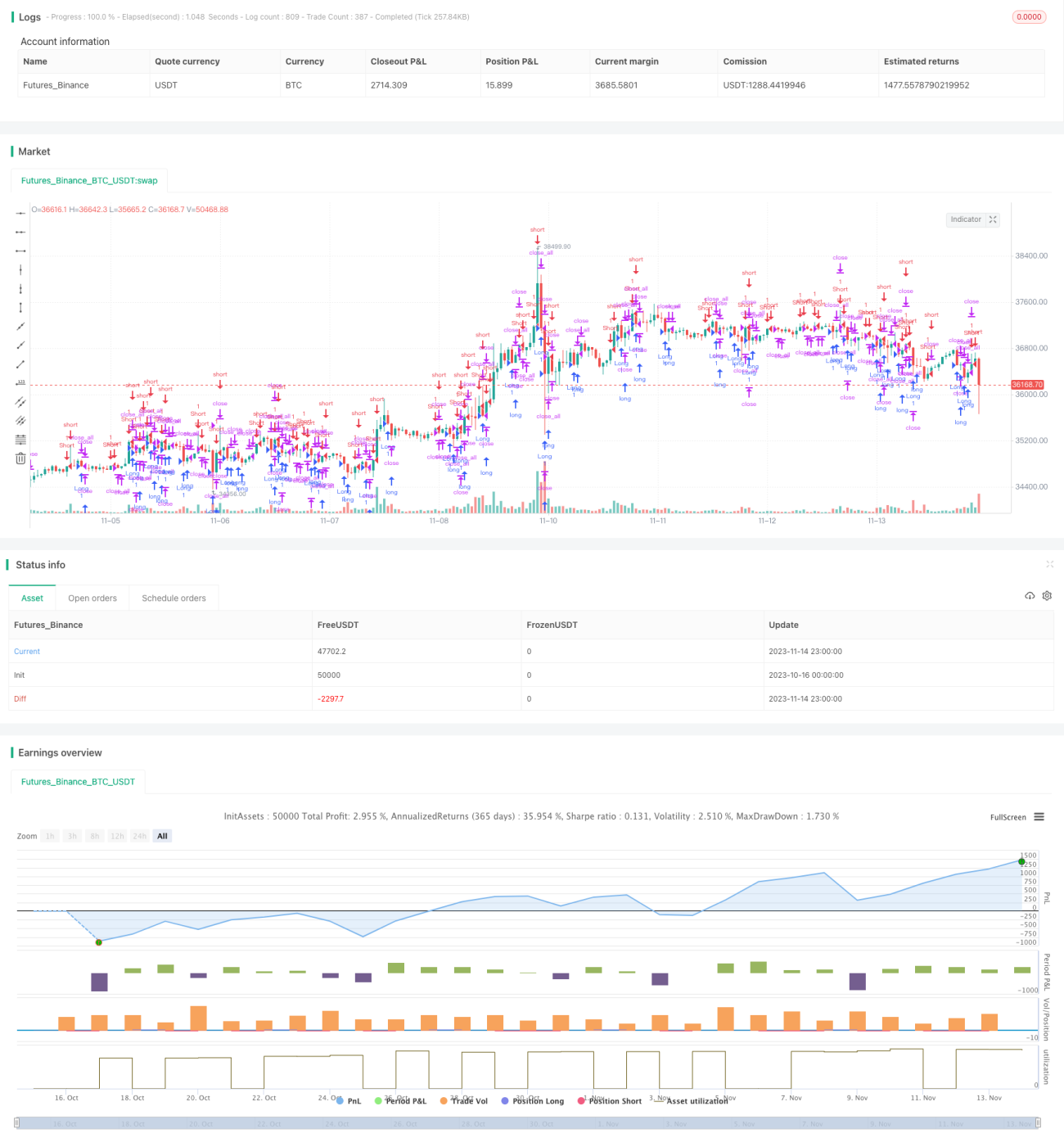

概述

该策略基于K线的实体长度来判断多空方向。它计算最近30根K线的平均实体长度,当阳线实体长度大于平均实体长度时做多,当阴线实体长度大于平均实体长度时做空。

策略原理

该策略首先计算K线的实体长度body,及最近30根K线实体长度的平均值sbody。

当今日K线为阴线(bar==-1),且实体长度大于平均实体长度时,打开多单(up1)。

当今日K线为阳线(bar==1),且实体长度大于平均实体长度时,打开空单(dn1)。

多单打开后,如果今日K线为阳线(bar==1),且当前头寸为盈利状态,则平仓多单。

空单打开后,如果今日K线为阴线(bar==-1),且当前头寸为盈利状态,则平仓空单。

该策略简单有效地利用了K线实体的长度来判断行情趋势,实体越长表示趋势越强,因此以实体长度作为判断多空的依据。

优势分析

该策略具有以下优势:

-

策略思路简单明了,容易理解和实现。

-

利用K线实体长度判断趋势,避免被噪音干扰。

-

采用动态平均值计算,可以适应市场的变化。

-

设置盈利平仓条件,可以提高策略收益率。

-

可配置策略参数,适用于不同市场环境。

风险分析

该策略也存在一些风险:

-

实体较长不一定代表强势趋势,可能是正常波动。

-

平均实体长度的时间窗口设定不当可能导致错失交易机会。

-

突发事件可能导致策略亏损。

-

多空头寸持有时间过长可能导致亏损扩大。

对应风险的解决方法:

-

结合其它指标判断趋势,避免错 trades。

-

测试不同参数取值,优化平均实体长度的计算。

-

设置止损止盈条件,控制单次亏损。

-

优化开仓和平仓逻辑,避免持仓时间过长。

优化方向

该策略可以从以下方面进行优化:

-

结合MACD、RSI等指标判断趋势,避免因常规波动产生错误信号。

-

测试不同的平均实体长度时间窗口参数,寻找最优参数组合。

-

添加开仓量控制逻辑,随着亏损次数增加逐步减少开仓量。

-

设置移动止损或利润率止损退出条件,控制单次亏损比例。

-

优化开仓和平仓条件,避免无效交易。例如连续3根K线实体较长再开仓。

-

在特定时间段或重要数据发布前后避开交易,控制汇率冲击带来的亏损。

总结

该策略整体思路清晰易懂,通过比较K线实体与其平均长度来判断入场时机。策略优化空间较大,可从多方面入手进行优化调整,使策略参数更符合不同市场环境。整体来说,该策略作为一个量化交易入门策略足够简单可靠,适合新手 traders 使用和学习。通过不断优化和组合更多指标,可以进一步提高策略收益率和稳定性。

- 1