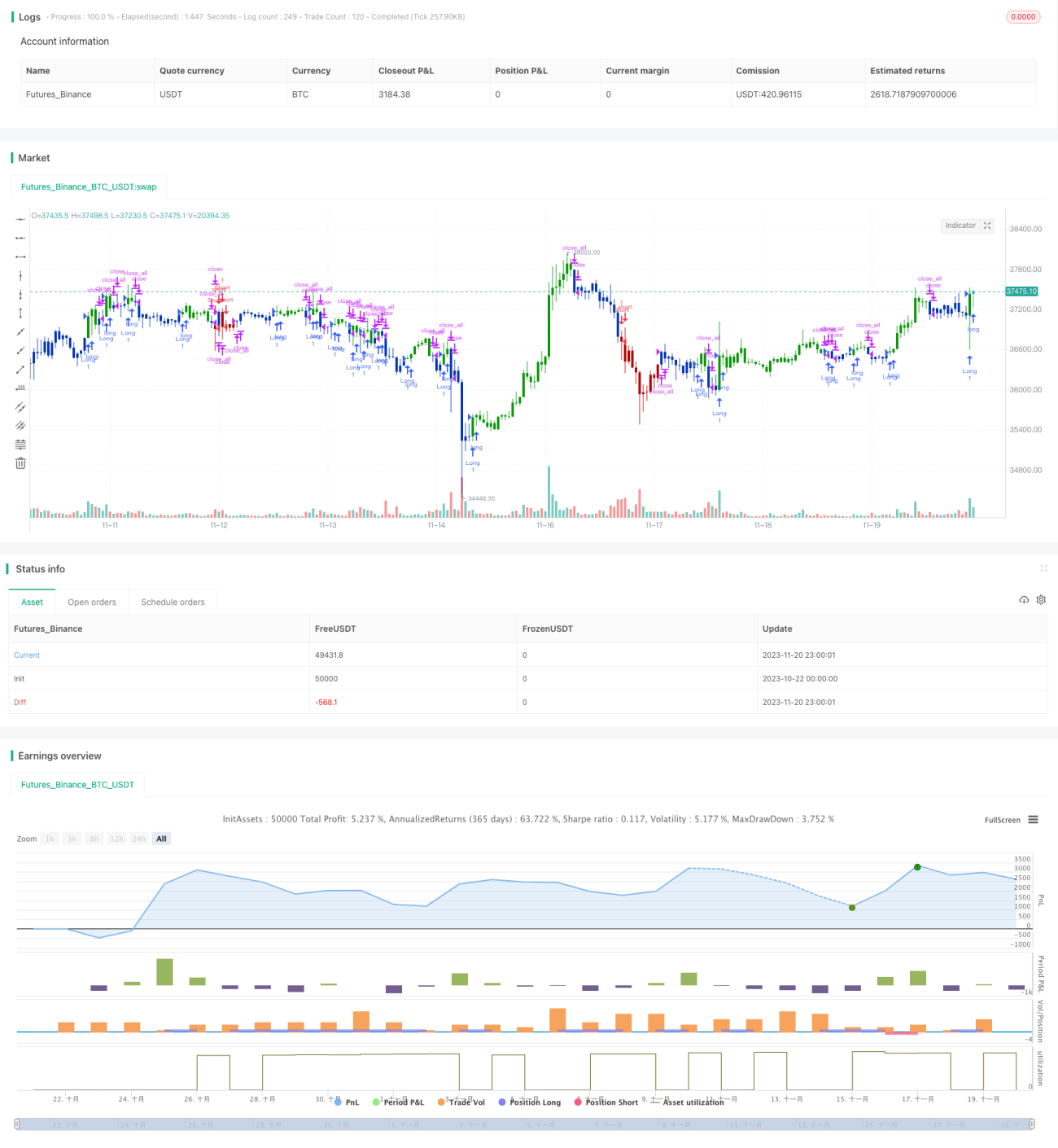

Quant Trading Double Click Reversal Strategy

Overview

This strategy first uses the 123 pattern to determine the reversal signal, and then combines the Klinger Volume Oscillator as a filter to implement the double-click quantitative profit strategy to efficiently capture reversal opportunities.

Principle

The strategy consists of two parts:

-

123 pattern to determine reversal signals: when the closing price falls continuously for 2 consecutive days and the 3rd day closes positive, and the stoch indicator is at a low level for long; when the closing price rises continuously for 2 consecutive days and the 3rd day closes negative, and the stoch indicator is at a high level for short.

-

Klinger Volume Oscillator section: Klinger Volume Oscillator combines price fluctuation range and trading volume changes to determine capital inflows and outflows. When the volume oscillator crosses above its average value, it is a long signal; when it crosses below its average value, it is a short signal.

Finally, the strategy combines the signals from the above two parts and double clicks to determine the final entry.

Advantage Analysis

The biggest advantage of this strategy is that it combines reversal patterns and volume indicators to efficiently capture reversal opportunities. In addition, with the help of stoch indicator, avoid false breakouts, and the Klinger Volume Oscillator to determine real money flow direction, accurate entry timing can be ensured.

Risk Analysis

The main risks of this strategy lie in the problem of reversal pattern judgment and parameter setting. Due to the delay in reversal signals, it needs to ensure that the parameters are set reasonably to avoid missing the best reversal timing. In addition, the reversal patterns themselves may fail.

To reduce risks, you can optimize parameters to make reversal signals more responsive and timely. Other filters can also be added to ensure a sufficient number and amplitude of reversals to avoid widening declines.

Optimization direction

The main optimization space for this strategy is in parameter adjustment and addition of other auxiliary judgments. Specifically, it's possible to appropriately shorten the stoch indicator parameters to optimize the sensitivity of 123 pattern discrimination. It is also feasible to combine with mainstream indicators and patterns currently, such as adding MACD golden crosses and deadly crosses, or double top/bottom multiple bottoms and other judgments.

In addition, consider dynamically adjusting stop loss and take profit conditions to make the strategy more adaptable to market changes. It is also possible to combine machine learning to optimize parameters in real time.

Summary

This strategy integrates the application of classical reversal theories and volume technical indicators to efficiently capture reversal opportunities. The space for optimization is large and has the potential to further improve the effect, which is worth validating and continuously optimizing in real trading.

/*backtest

start: 2023-10-22 00:00:00

end: 2023-11-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 23/12/2020

// This is combo strategies for get a cumulative signal. - 1