Adaptive Take Profit and Stop Loss Strategy Based on Dual Time Frames and Momentum Indicators

Overview

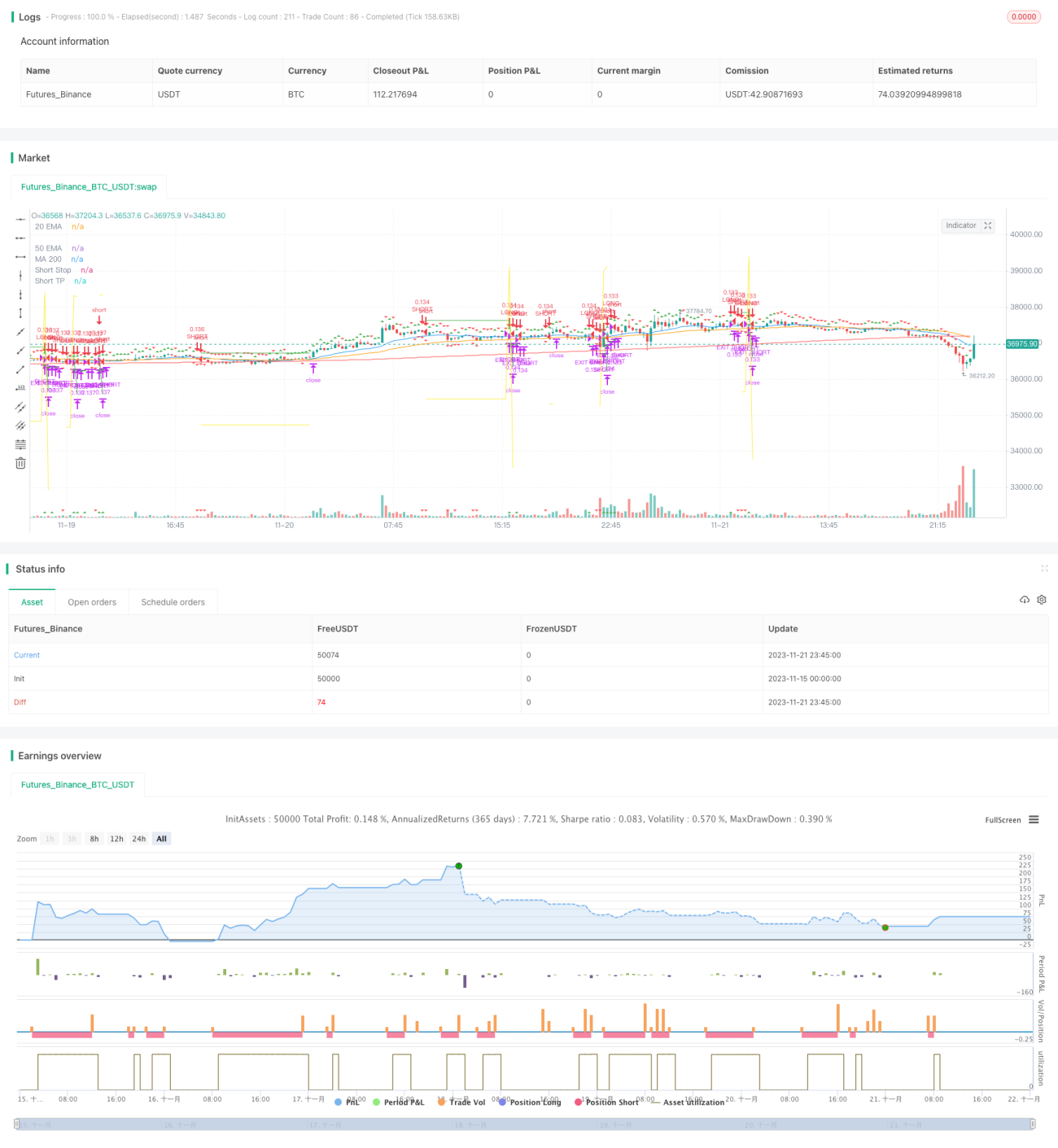

This strategy combines dual time frames and momentum indicators to achieve adaptive take profit and stop loss. The main time frame monitors the trend direction, while the secondary time frame is used to confirm signals. Trading signals are generated when the directions of both align. After entering the market, take profit and stop loss levels are updated progressively.

Strategy Logic

-

The main time frame uses the Squeeze Momentum (SQM) linear regression indicator to determine the trend. The secondary time frame uses an EMA combination on the SQM indicator to filter false signals.

-

When the main chart SQM breaks out upwards and the secondary chart SQM also goes up, a long position is taken. When the main chart SQM breaks downwards and the secondary chart SQM also goes down, a short position is taken.

-

After entering the market, initial take profit and stop loss levels are set based on input parameters. When price reaches the take profit level, both take profit and stop loss levels are updated. Specifically, the take profit level is increased progressively and the stop loss level is tightened, achieving gradual profit taking.

Advantages

-

Dual time frames filter false signals and ensure accuracy.

-

The SQM indicator determines trend direction, avoiding market noise.

-

The adaptive take profit and stop loss mechanism locks in profits to the maximum extent and effectively controls risk.

Risk Analysis

-

Improper SQM parameter settings may miss trend turning points, leading to losses.

-

An improper secondary time frame may fail to filter noise effectively, causing erroneous trades.

-

If the stop loss amplitude is set too wide, the per trade loss can be substantial.

Enhancement Opportunities

-

SQM parameters need to be tuned for different markets to ensure sensitivity.

-

Different secondary time frame periods should be tested to find the best noise filtering effect.

-

Instead of a fixed value, the stop loss amplitude can have a range set dynamically based on market volatility.

Summary

Overall this is a very practical strategy. The combination of dual time frames with a momentum indicator to determine trends, together with the adaptive take profit and stop loss method can generate stable profits. By optimizing the SQM parameters, secondary time frame period, and stop loss amplitude, strategy results can be further improved for productive live application and enhancement.

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1