Ichimoku Mixed Equilibrium Table Macd and Tsi Combined Strategy

I. Strategy Overview

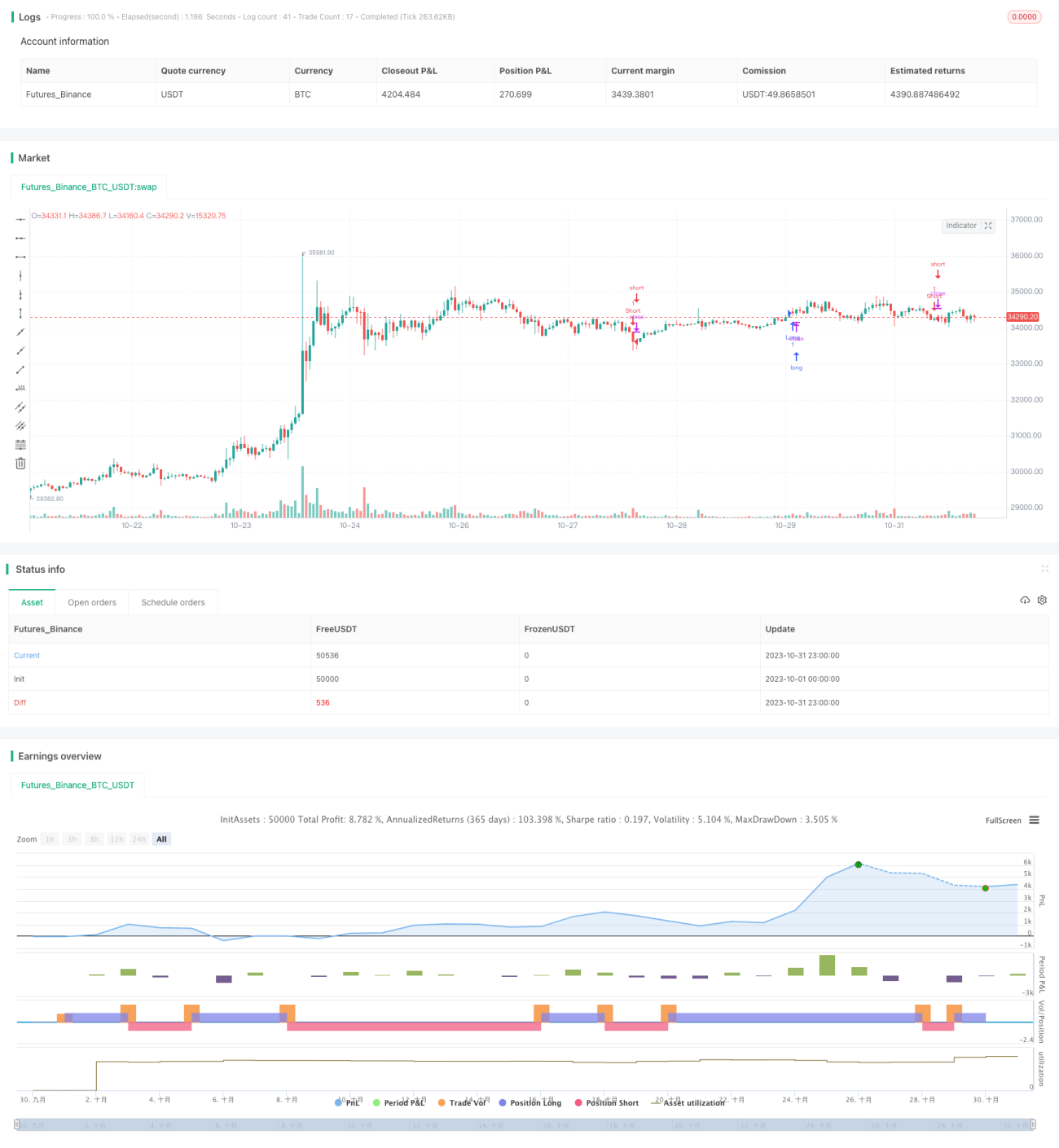

This strategy comprehensively uses technical indicators such as Ichimoku Kinko Hyo, Macd, Chaikin Money Flow and Tsi Oscillator to accurately judge the direction of market trends for short-term trading.

II. Strategy Principle

The strategy uses the Tenkan-sen line, Kijun-sen line, Senkou Span A and Senkou Span B lines in Ichimoku to judge intraday price trends. At the same time, it combines the cross signals of the fast and slow moving average lines of Macd and the money flow indicator and oscillation indicator to determine the inflow and outflow of funds. After the comprehensive judgment of multiple indicators, the buy and sell decisions are made.

When the Tenkan-sen line crosses above the Kijun-sen line, the Chikou Span is above the 0 axis, and the closing price is above the Ichimoku cloud, it is a bullish signal. On the contrary, when the Tenkan-sen line crosses below the Kijun-sen line, the Chikou Span is below the 0 axis, and the closing price is below the cloud, it is a bearish signal. At the same time, the strategy detects whether the MACD histogram is positive and whether the Chaikin Money Flow indicator and the TSI oscillator are positive in the same direction. If the indicators are bullish in the same direction, long position is opened by buying in, and if the indicators are bearish in the same direction, short position is opened by selling out.

When the indicator issues a signal opposite to the previous one, a reverse trade is made to flatten the previous position.

III. Advantages of The Strategy

-

Using a combination of multiple indicators improves judgment accuracy.

-

Short-term operations track market fluctuations in real time.

-

No manual intervention, fully automated algorithmic trading.

IV. Risks of The Strategy and Solutions

-

The combined judgment of multiple indicators being bullish or bearish at the same time has the risk of misjudgment. Some judge criteria could be appropriately relaxed to reduce misjudgment rate.

-

High-frequency short-term trading has relatively high commission fees and it’s hard to catch trends. Position holding period could be appropriately extended to seek excess returns to cover costs.

-

No stop loss setting may lead to greater losses. Appropriate stop loss points or moving stop loss can be set based on the ATR.

V. Directions for Strategy Optimization

-

Optimize parameter combinations. Adjust moving average parameters to adapt to different cycles and varieties.

-

Increase stop loss mechanism. Set dynamic stop loss lines combined with the ATR indicator.

-

Increase position management. Dynamically adjust trading volume proportions.

-

Combine machine learning technology to optimize indicators and signals.

VI. Conclusion

This strategy comprehensively uses multiple technical indicators to determine trend fluctuations in real time for high-frequency short-term trading. Although there are some risks, it can be improved through optimization. The strategy is worth further in-depth research and live trading verification. By increasing stop loss and position management, trading risks could be reduced.

- 1