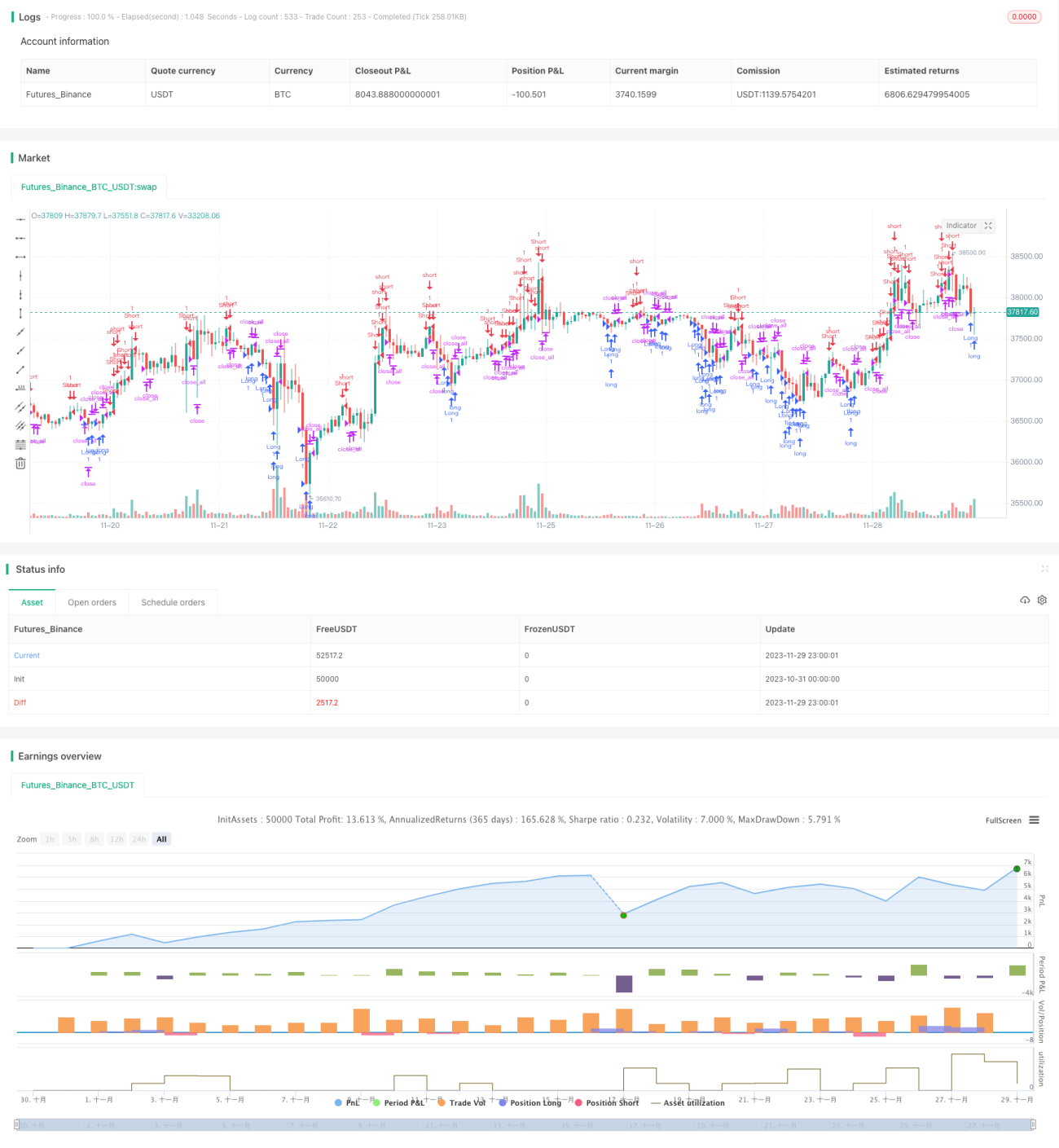

Fast RSI Reversal Strategy

这里是我根据你提供的代码和要求写的SEO文章,包含了策略名称、概述、策略原理、优势分析、风险分析、优化方向和总结等部分:

Overview

This strategy is a fast RSI reversal trading strategy that mainly captures reversal opportunities when RSI is overbought or oversold. It uses 3-day RSI to judge overbought and oversold levels, and combines 30-day MA to determine breakthrough signals, opening positions when reversals occur after overbought or oversold status.

Strategy Logic

The strategy uses two indicators:

-

3-day RSI to judge overbought and oversold levels.

-

30-day MA to determine the strength of reversal signals. When the reversal bar body is greater than half of the 30-day MA, it is used as the entry signal.

Specific trading rules:

Long signal: When RSI is below the lower limit (default 25) and the current bar body is greater than half of the 30-day MA, go long.

Short signal: When RSI is above the upper limit (default 75) and the current bar body is greater than half of the 30-day MA, go short.

Exit signal: When holding long positions, if RSI crosses above the upper limit, or when holding short positions, if RSI crosses below the lower limit, meanwhile the bar body is greater than half of the 30-day MA, close positions.

Advantage Analysis

The advantages of this strategy include:

-

Using short-period RSI to capture short-term reversal opportunities quickly.

-

Increasing signal reliability by combining with MA filter, avoiding whipsaws in range-bound markets.

-

Controllable drawdowns, maximum drawdown won't be too large.

-

Clear position control rules, avoids over-trading.

Risk Analysis

The risks of this strategy include:

-

Failed reversal risk. Overbought and oversold does not necessarily lead to reversals.

-

Loss risk by trading against the trend in trending markets.

-

Missing opportunities due to too strict bar filter rules.

-

High parameter sensitivity, RSI and MA periods need adjustment.

Optimization Directions

The strategy can be optimized from the following aspects:

-

Optimize RSI parameters to find the optimal period.

-

Optimize MA parameters to determine the best bar filter period.

-

Add stop loss strategies like trailing stop loss, to control single trade loss.

-

Add trend determination rules to avoid trading against trends.

Conclusion

In conclusion, this is a short-term reversal-focused RSI strategy. It captures reversals by identifying quick RSI overbought and oversold levels, and uses MA bar filter to confirm entries. The advantages are controllable drawdowns and clear position controls. It is suitable for short-term trading but should watch out risks of failed reversals and trading against trends. It can be improved by parameter optimization, adding stop loss, and judging trends.

/*backtest

start: 2023-10-31 00:00:00

end: 2023-11-30 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy(title = "Noro's Fast RSI Strategy v1.0", shorttitle = "Fast RSI str 1.0", overlay = true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, pyramiding = 5)

//Settings- 1