Reverse Triad Quantitative Strategy

Overview

The Reverse Triad Quantitative Strategy combines the 123 Reversal Strategy and the Accelerator Oscillator to judge trend reversals and generate more accurate trading signals. This strategy is mainly used for short-term and medium-term trading of stock indices, forex, precious metals and energy products.

Strategy Logic

This strategy consists of two independent logic codes.

The first part is the 123 Reversal Strategy. Its principle for judging reversal signals is: a buy signal is generated when the close price is lower than the previous close for two consecutive days and the 9-day STOCH K-line is below the D-line; A sell signal is generated when the close price is higher than the previous close for two consecutive days and the 9-day STOCH K-line is above the D-line.

The second part is the Accelerator Oscillator indicator. This indicator reflects the speed of change of the Awesome Oscillator by calculating the difference between the Awesome Oscillator and its 5-period moving average, which can help identify trend reversal points earlier than the Awesome Oscillator.

Finally, this strategy combines the signals of the two indicators: when the signals of both indicators are in the same direction (both long or both short), the corresponding direction signal is output; when the signals of the two indicators are inconsistent, a zero signal is output.

Advantage Analysis

This strategy combines dual indicator judgments to filter out some false signals, making the signals more accurate and reliable. At the same time, by utilizing the Accelerator Oscillator's feature of reflecting accelerated changes, potential trend reversal points can be captured early, thus capturing greater profit room.

Risk Analysis

The biggest risk of this strategy is that the price has already reversed significantly before the indicators generate signals, resulting in missing the best entry point. In addition, indicator parameters need to be optimized and adjusted in case of drastic market fluctuations.

To address the entry point risk, more reversal indicators can be combined to ensure signal reliability; For the parameter optimization problem, a dynamic adjustment mechanism can be established to ensure parameter rationality.

Optimization Directions

The following aspects of this strategy can be optimized:

-

Add filtering conditions to avoid generating wrong signals during high volatility stages

-

Combine more reversal indicators to form a multi-validation mechanism

-

Establish a parameter self-adaptive mechanism to dynamically adjust indicator parameters

-

Optimize stop loss strategies to control single stop loss

Conclusion

The Reverse Triad Quantitative Strategy improves signal accuracy through dual verification, which is helpful to grasp the key reversal points of the market. At the same time, attention should also be paid to preventing risks such as indicator lagging and parameter failure. Continuous verification and optimization of the strategy is needed to adapt it to the ever-changing market environment. This strategy is suitable for investors with some quantitative trading experience.

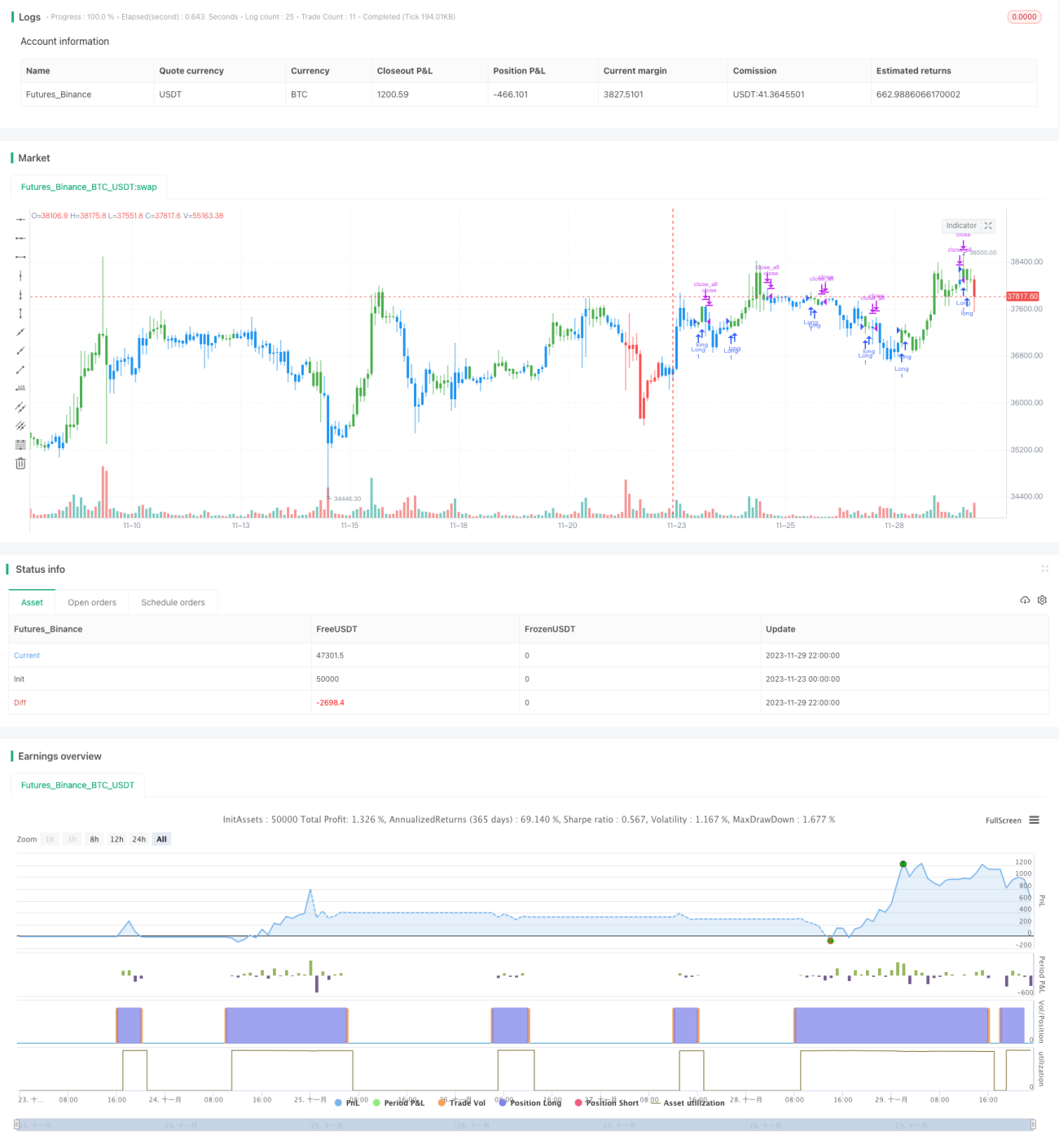

/*backtest

start: 2023-11-23 00:00:00

end: 2023-11-30 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 25/04/2019

// This is combo strategies for get - 1