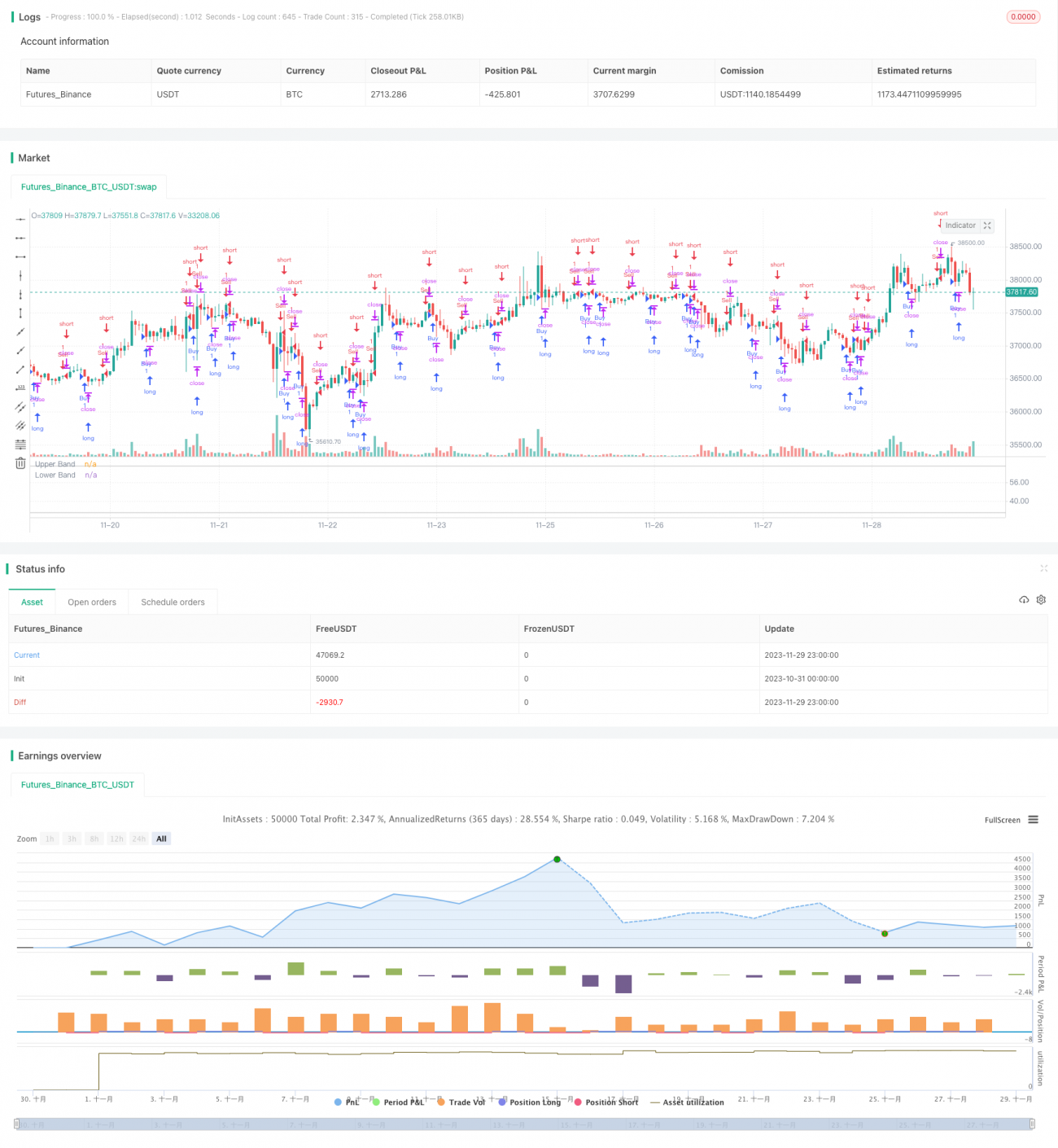

概述

本策略名为“双均线策略”,其核心思想是同时利用相对强弱指标(RSI)和移动平均线(MA)这两个指标来产生交易信号。具体来说,当RSI线从上向下跨过MA线时生成买入信号;当RSI线从下向上跨过MA线时生成卖出信号。该策略相对简单,但通过结合两个不同类型的指标,可以有效减少假信号,提高信号的可靠性。

原理

双均线策略的基本逻辑是:

- 计算RSI值,以反映股票的超买超卖情况

- 计算MA值,以判断价格平均趋势

- 当RSI从高点下降,由超买区域进入超卖区域,并下穿MA时,产生买入信号

- 当RSI从低点上升,由超卖区域进入超买区域,并上穿MA时,产生卖出信号

以上交易信号发生时,我们会在图表上画出相关标记,方便视觉判断。这就是双均线策略的整体工作流程。

优势

双均线策略最大的优势在于能有效结合趋势指标和超买超卖指标,使交易信号更加可靠。具体来说,主要有以下几个方面的优势:

-

减少假信号。RSI和MA的结合使用,可以相互验证信号,避免单一指标产生的假信号。

-

提高胜率。相比单一RSI或MA策略,双均线策略可以获得更高的盈利机会。

-

适应性强。该策略仅用两个参数,操作简单,使用成本低,适合不同市场环境。

-

容易优化。通过调整RSI和MA的周期参数,可以方便优化,适应更多品种。

风险

尽管双均线策略有许多优点,但在实际应用中也不能完全避免风险。主要的风险包括:

-

MA采用了历史均价,可能滞后于最新价格变化。

-

RSI可能出现假突破的情况,产生错误信号。

-

无法适应快速变化的趋势市场,容易止损。

-

参数设置不当也会大幅影响策略表现。

对此,我们主要从以下几个方面进行风险控制:

-

采用自适应MA,根据最新价格变化调整周期参数。

-

增加止损机制,控制单笔亏损。

-

优化参数,选择最佳参数组合测试。

-

采用步进止损,锁定部分利润,降低风险。

优化方向

针对双均线策略可能存在的问题,我们考虑从以下几个维度进行优化:

-

利用自适应MA代替普通MA,可以更快捕捉价格变化趋势。

-

增加成交量指标的验证,避免假突破。例如收盘价与成交量齐齐上涨时才买入。

-

结合其他指标 filt过滤无效信号。例如MACD 或KD指标的 verifies 。

-

优化参数设置区间,寻找最优参数组合。可以通过回测寻找策略Highest 盈利的参数区间。

-

采用机器学习技术进行参数自适应优化。让策略能够根据实时市场状况选择最优参数。

通过以上几点优化,有望大幅提升双均线策略的实盘表现。

总结

双均线策略整合了RSI和MA两个指标的优点,通过二者配合,可以产生更加准确和可靠的交易信号。相比单一技术指标策略,双均线策略具有信号准确度高、假信号少、容易优化等优势。但也不能完全避免误操作风险,我们提出了一些具体的风险控制手段。此外,这一策略也存在可以继续优化的维度,若结合自适应指标、其他辅助验证指标、参数寻优等手段,有望进一步提高策略收益率。总体来说,本策略为量化交易提供了一个简洁实用的技术分析方案。

/*backtest

start: 2023-10-31 00:00:00

end: 2023-11-30 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="RSI + MA", shorttitle="RSI + MA")

reverseTrade = input(false, title = "Use Reverse Trade?")

lengthRSI = input(14, minval=1, title="RSI Length")- 1