Early Profit-Taking Moving Average Opening Bell Exit Strategy

Overview

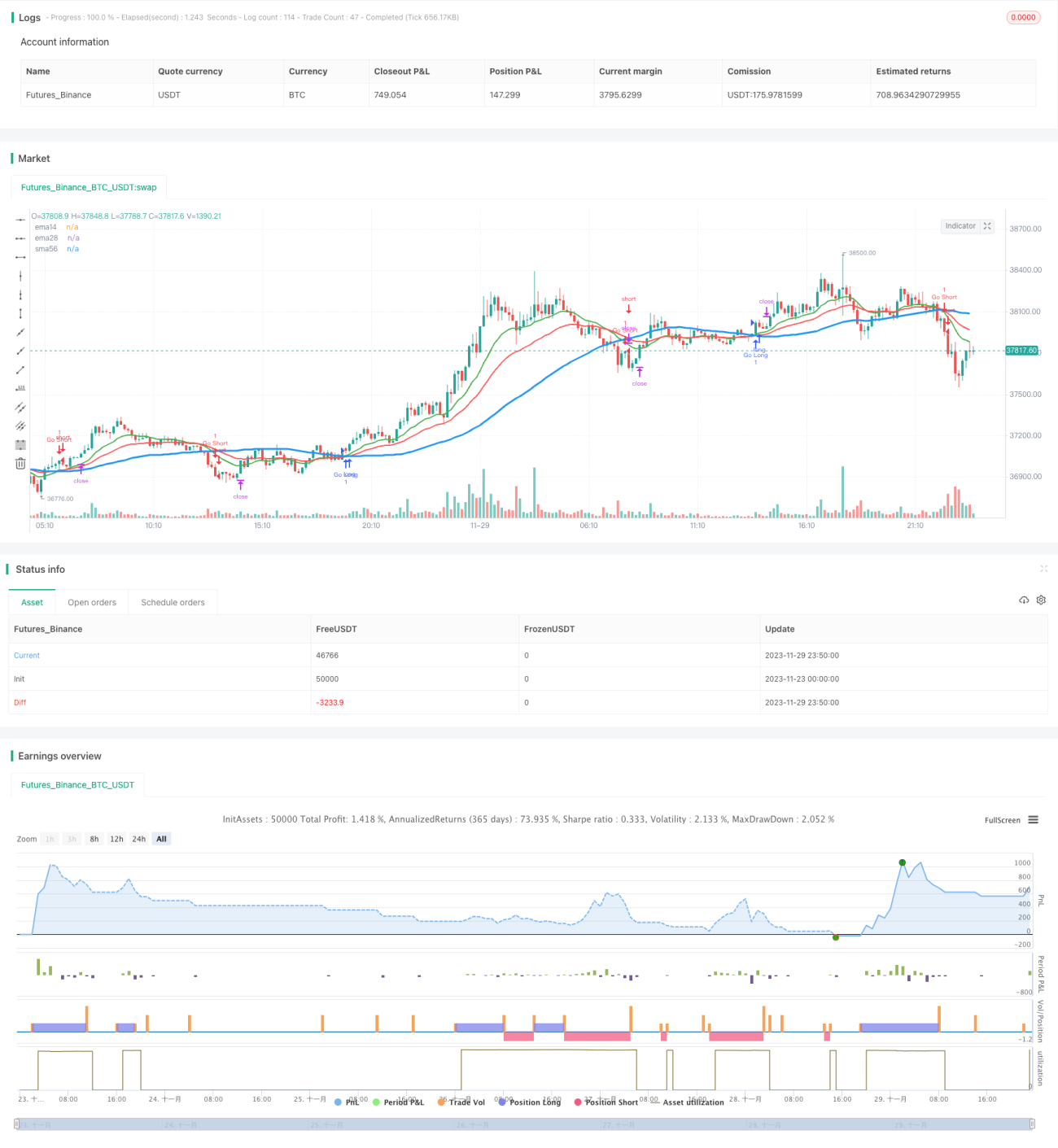

This strategy implements long and short based on moving average crossovers, and exits only in the afternoon based on early profit-taking statistics to avoid being trapped by high opening volatility.

Strategy Logic

The strategy uses 3 moving averages with different parameters: 14-day, 28-day and 56-day lines. It goes long when the 14-day line crosses above the 56-day one, and goes short when crossing below. This basic approach tracks long-term trends. To filter out some noise, the 28-day line is added as a reference, so that signals are triggered only when the 14-day line is also above or below the 28-day one.

The key innovation is that it stops loss and takes profit only between 4 pm and 5 pm. Statistics show 70% chance of daily high/low happening in the first hour after opening. To avoid impact from high opening volatility, exits are enabled only during regular afternoon trading hours.

Advantage Analysis

The advantages of this strategy include:

- Track mid-long term trends, avoid excessive noise

- Utilize statistics of opening volatility for stop loss logic to avoid false breakouts

- Simple and intuitive logic, easy to understand and modify

Risks and Solutions

There are also some risks:

- Missing opportunities if reversal happens early in the day. Can test compatibility with specific stocks.

- Still risks of being trapped after hours. Can test loosening stop loss range.

- Bad setting of backtest period leading to overfitting. Should expand backtest duration.

Enhancement Opportunities

Some ways to further optimize the strategy:

- Test different moving average combinations to find optimum parameters

- Fine tune stop loss range based on volatility patterns of specific stocks

- Add volume filter to avoid traps

- Add dynamic stops to trail pullbacks after breakouts

Conclusion

The strategy has clear and simple logic, effectively uses opening features for stop loss to avoid volatility traps. But risks exist of missing chances and being trapped. Parameters should be adjusted per stock. Overall a simple yet effective idea for novice quants.

- 1