SSL Hybrid Exit Arrow Quant Strategy

Overview

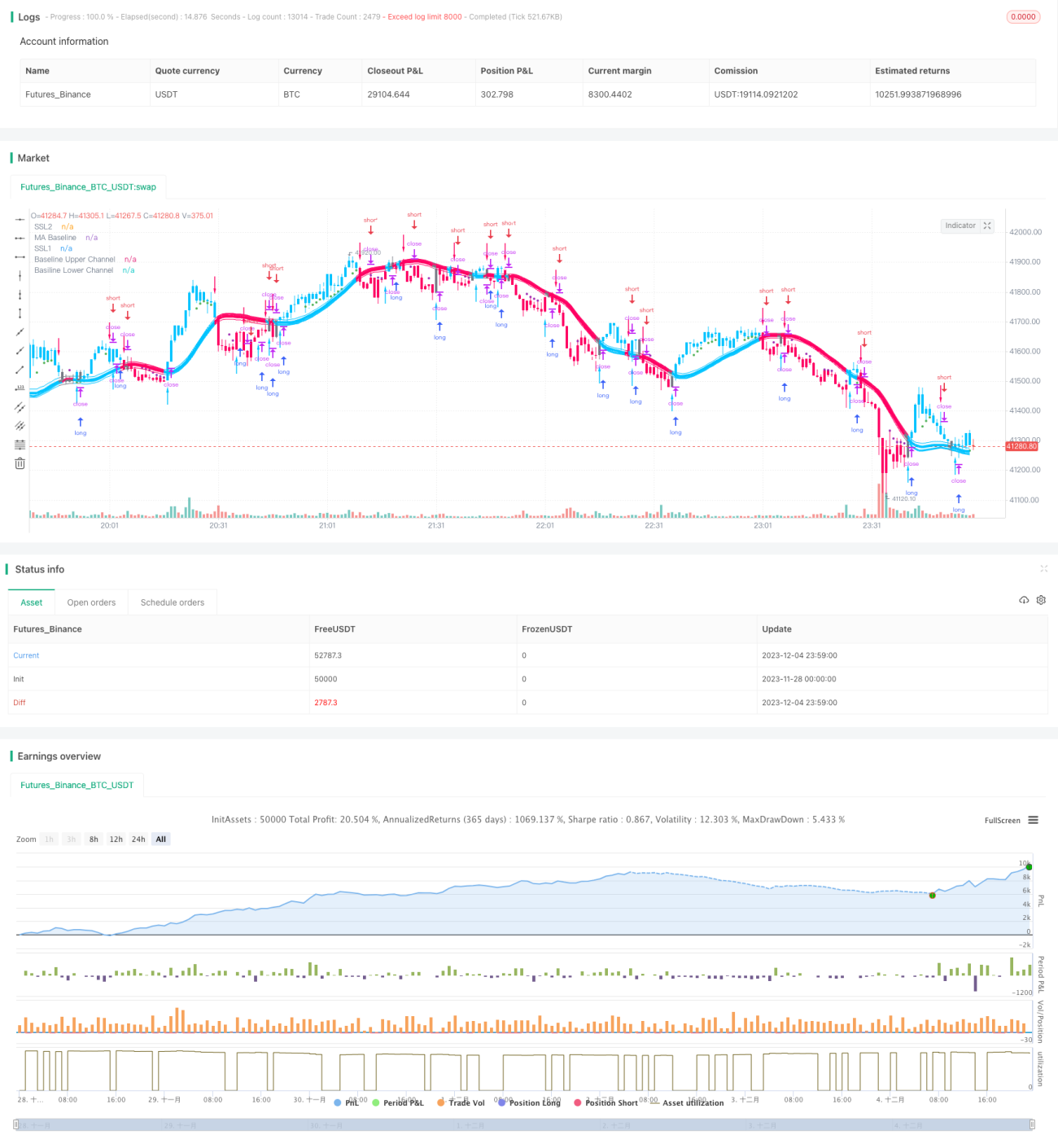

The SSL Hybrid Exit Arrow Quant Strategy is a short-term quantitative trading strategy based on moving averages and maximum/minimum price indicators. It utilizes the EXIT arrows of the SSL hybrid indicator to determine entry and exit points, with the QQE indicator as a filter, and calculates stop loss and add-on positions with the ATR indicator. This strategy suits investors who are sensitive to market volatility and have strict risk control.

Strategy Logic

This strategy uses the EXIT arrows of the SSL hybrid indicator to determine entry points. Above the EXIT arrows are the EXIT high points, and below them are the EXIT low points. A sell signal is generated when the close price crosses below the EXIT high point, and a buy signal is generated when the close price crosses above the EXIT low point.

To improve signal reliability, the QQE indicator is introduced as an auxiliary filter condition. Signals generated by the EXIT arrows are only executed when the QQE indicator is in the same direction.

To control risks, this strategy uses ATR multiples to calculate stop loss and add-on positions. The stop loss for short positions is close price + ATR × 1.8. The stop loss for long positions is close price – ATR × 1.8. Positions are added in three batches, with the amount of each batch being 10% of the initial amount. The add-on price levels are: close price – ATR × 0.1, close price – ATR × 0.3, and close price – ATR × 0.7.

Each batch of add-on positions has its own stop loss. The first batch of 20% of position size will stop loss when reaching the stop loss level, while the remaining positions continue to hold.

Advantages

- Profit from EXIT arrows and effectively control risks with timely stop loss

- The QQE filter improves signal accuracy

- Use the ATR indicator to calculate dynamic stop loss and add-on positions based on market volatility for more precise risk control

- Take full advantage of trends through batched add-on positions

Risks

- Partial stop loss of profitable positions may expose the remaining positions to further stop loss. Consider overall profit taking or fundamentals-based stop loss.

- Differences in sensitivity to market volatility between EXIT arrows and QQE may cause conflicting signals. Parameters should be adjusted to reduce signal conflicts.

- Overly aggressive add-on positions are prone to chasing tops and dumping bottoms. Positions sizes should match market conditions.

Optimization Directions

- Incorporate fundamental indicators like P/B ratio, P/E ratio and dividend yield for fundamentals-based profit taking levels.

- Adjust QQE parameters to align signals with EXIT arrows.

- Reduce add-on ratios based on market sentiment in ranging markets.

- Test optimum parameter sets based on max drawdown, risk-reward ratios etc.

Summary

This strategy uses the EXIT arrows of the SSL hybrid indicator as the signal core, with the QQE and ATR indicators as filters and for stop loss. Profit compounding is achieved through batched add-on positions. It is a short-term quantitative strategy suitable for tracking short-term market trends. The strategy has drawdown control and risk mitigation capabilities, but risks like signal conflicts and chasing tops/smashing bottoms should be noted. Incorporating fundamentals-based profit taking and being more prudent when determining oscillating markets and reducing add-on ratios can further expand this strategy’s profit potential.

- 1