Simple Momentum Strategy Based on SMA, EMA and Volume

Overview

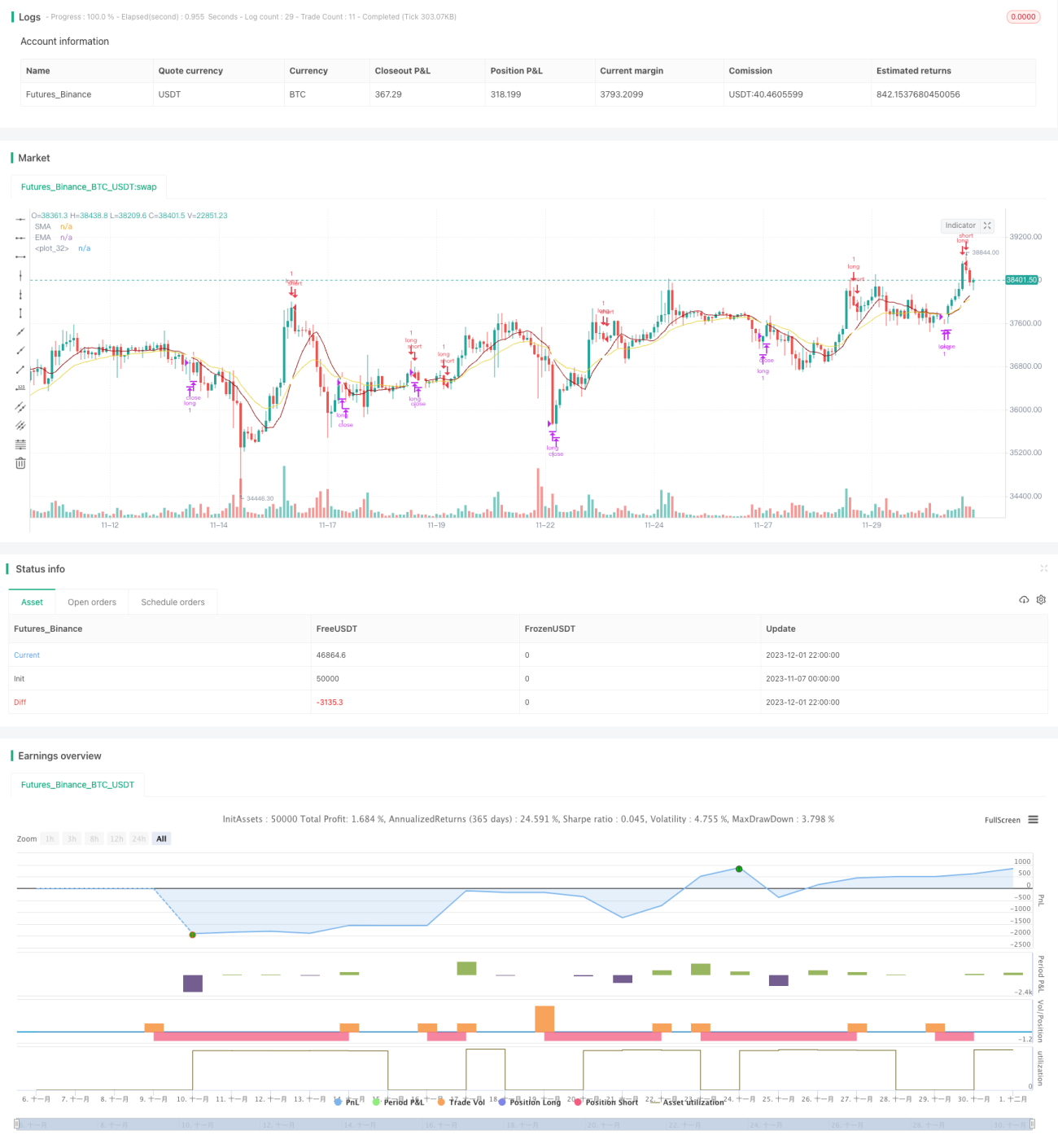

This is a simple intraday momentum strategy that only goes long and does not short. It utilizes SMA, EMA and volume indicators to attempt entering the market at the optimal timing when both price and momentum are trending up. Its advantage is being simple while having some trend recognition capability.

Strategy Principle

The entry signal logic is: when SMA is higher than EMA, and there is a consecutive 3-bar or 4-bar uptrend pattern, with the lowest price of the middle bars being higher than the open price of the starter uptrend bar, an entry signal is generated.

The exit signal logic is: when SMA crosses below EMA, an exit signal is generated.

This strategy only goes long and does not short. Its entry and exit logic has some capability in recognizing persistent uptrends.

Advantage Analysis

The advantages of this strategy:

-

The logic is simple and easy to understand and implement;

-

Utilizes common technical indicators like SMA, EMA and volume for flexibility in parameter tuning;

-

Has some capability in catching some opportunities during persistent uptrends.

Risk Analysis

The risks of this strategy:

-

Inability to detect downtrends or consolidation markets, leading to large drawdowns;

-

Inability to utilize shorting opportunities, unable to hedge against downtrends, missing good profit chances;

-

Volume indicator does not work well on high frequency data, parameters need adjustment;

-

Can use stop loss to control risks.

Optimization Directions

This strategy can be optimized in the following aspects:

-

Adding shorting capability for mean reversion opportunities;

-

Using more advanced indicators like MACD and RSI for better trend detection;

-

Optimizing stop loss logic to reduce drawdowns;

-

Tuning parameters and testing different timeframes to find optimal parameter sets.

Conclusion

In summary this is a very simple trend following strategy utilizing SMA, EMA and volume for entry timing. Its advantage is being simple and easy to implement, good for beginners to learn, but it cannot detect consolidation or downtrends and has risks. Improvements can be made by introducing shorting, optimizing indicators and stop loss etc.

- 1