The Smooth Moving Average Ribbon Strategy

Overview

This strategy constructs a smooth price band using smooth moving averages and integrates various smooth moving averages to filter the trend in real time. It belongs to a typical trend following strategy.

Strategy Principle

- Construct a smooth price band to track price changes using smooth moving averages.

- The strategy supports various moving average types as the calculation method for smooth moving averages, such as EMA, SMMA, KAMA, etc.

- It supports 1-5 layers of stacking smoothness on these moving averages to obtain an even smoother price band.

- It also supports adding Bollinger Bands between prices and moving averages to better capture price changes.

- By enabling an additional moving average filter, it can filter out fluctuations better and identify trend directions. The filter also supports multiple moving average types.

- Combined with pattern recognition indicators, it can automatically identify buy and sell signals.

By constructing a smooth price band to capture price trends, and integrating a moving average filter to confirm trend directions, this strategy belongs to a typical trend following strategy. By adjusting parameters, it can be flexibly adapted to different products and timeframes.

Advantages

- Constructing price bands can track price trend changes more smoothly, reducing the probability of missing opportunities.

- Supporting multiple moving average types allows selecting suitable moving averages based on different timeframes and products, improving the adaptability of the strategy.

- 1-5 layers of stacking smoothness can significantly improve the tracking capability of price changes and capture trend reversal points more precisely.

- The moving average filter can effectively reduce invalid signals and improve win rate.

- By adjusting moving average lengths, it can be adapted to different timeframes. Multi-timeframe verification can further improve strategy performance.

- Supporting black glass display enables clear and intuitive observation of price band trends.

Risks

- Strong in tracking long-term trends, but poor in tracking and reacting to short-term fluctuations, tending to generate more invalid signals in range-bound markets.

- In violent price surges and plunges, the lagging of smooth moving averages may miss the best entry timing.

- Excessive stacking of moving averages may overly smooth price changes and cause inaccurate identifications of buy and sell points.

- If the enabled moving average length parameters are improperly set, it may generate a large number of false signals.

Solutions:

- Appropriately shorten moving average lengths to accelerate reaction to price changes.

- Adjust stacking times to reduce over-smoothness.

- Optimize and test moving average combinations to select optimal parameters.

- Use multi-timeframe verification with other indicators to reduce false signals.

Optimization Directions

- Test and optimize combinations of moving average types to select optimal parameters.

- Test and optimize moving average length parameters to adapt to more products and timeframes.

- Try different stacking smoothness times to find the optimal balance point.

- Try adding Bollinger Bands as an auxiliary indicator.

- Test different additional moving averages as filters.

- Use multi-timeframe verification with other indicators.

Conclusion

This strategy belongs to a typical trend following strategy that continuously tracks price trends by constructing smooth moving average bands and avoids invalid signals with assisting filters. Its advantage lies in constructing smooth price bands to better capture turns in price trends. It also has certain risks of lagging. By parameter optimization and indicator optimization, the strategy performance can be continuously improved and is worth further research.

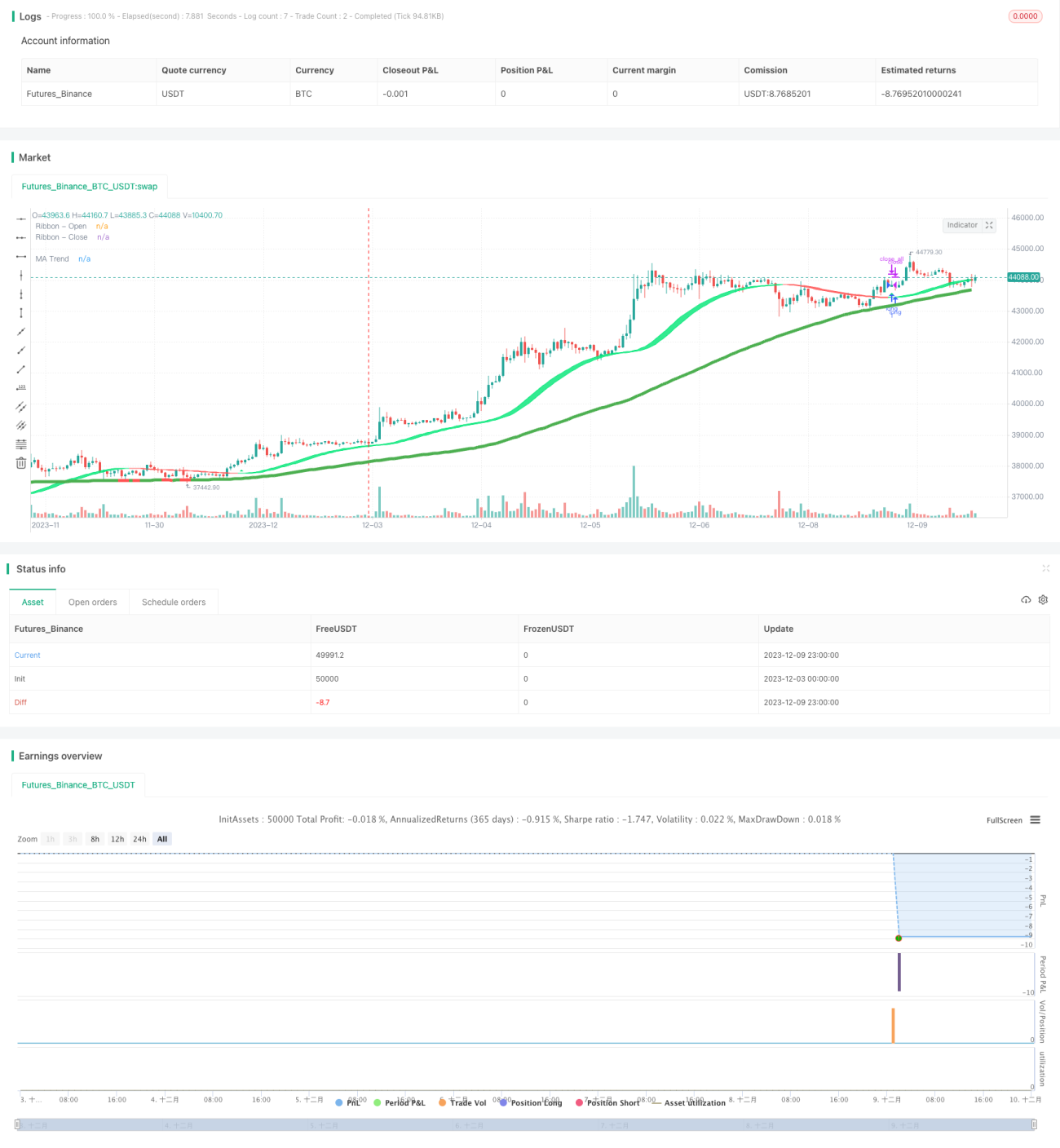

/*backtest

start: 2023-12-03 00:00:00

end: 2023-12-10 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Copyright (c) 2007-present Jurik Research and Consulting. All rights reserved.

// Copyright (c) 2018-present, Alex Orekhov (everget)

// Thanks to everget for code for more advanced moving averages- 1