Momentum Pullback Strategy

Overview

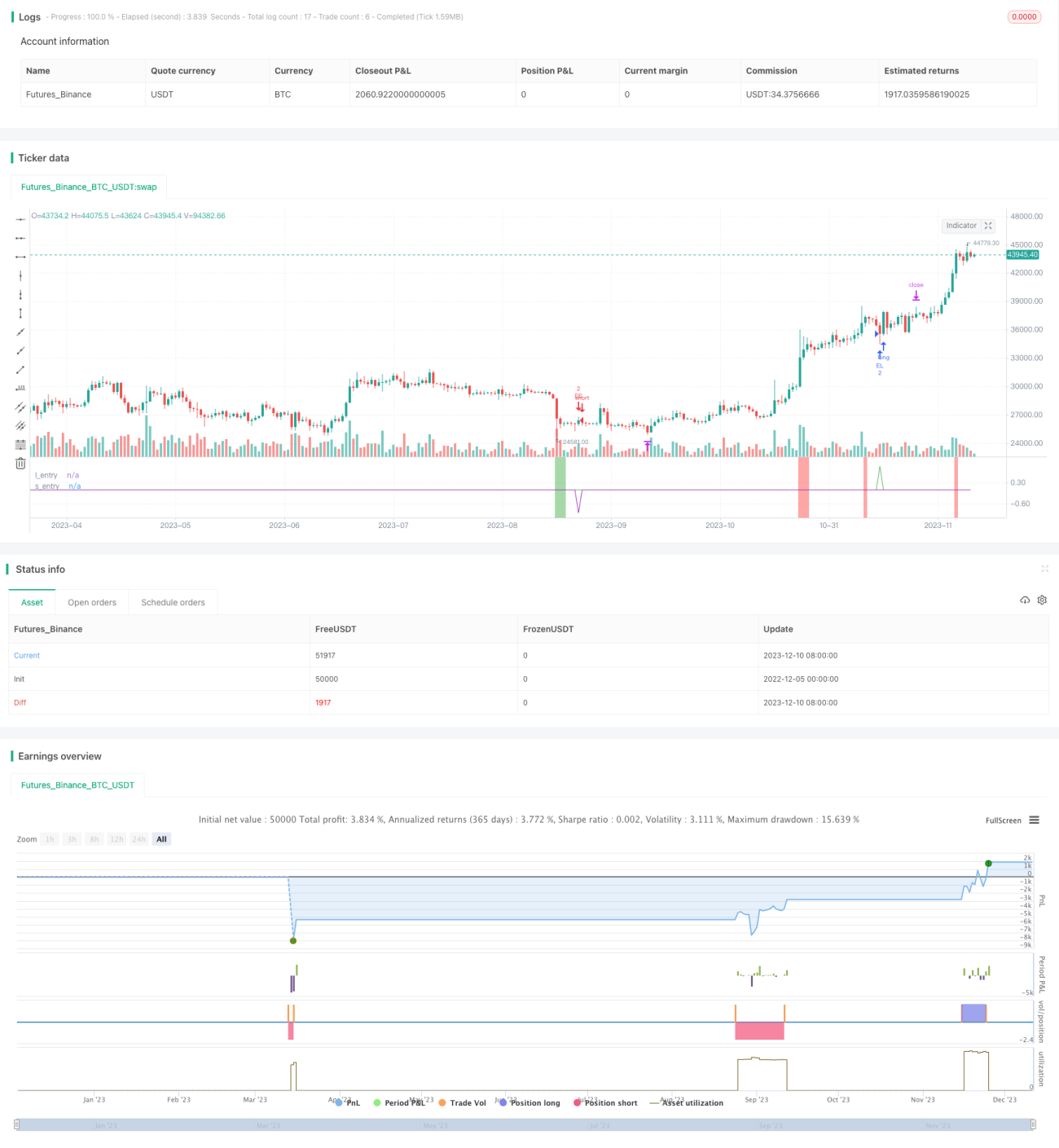

The Momentum Pullback Strategy identifies extreme RSI readings as momentum signals for a long/short strategy. Unlike most RSI strategies, it looks to buy or sell the first pullback in the direction of the extreme RSI reading.

It enters long/short on the first pullback to the 5-period EMA (low)/5-period EMA (high) and exits at the rolling 12-bar high/low. The rolling high/low feature means the profit target will begin to reduce with each new bar if the price enters prolonged consolidation. The best trades tend to work within 2-6 bars.

The suggested stop loss is X ATRs (adjustable in inputs) from the entry price.

The strategy is fairly robust across timeframes and markets with 60%-70% win rate and larger winning trades. Signals occurring from news volatility should be avoided.

Strategy Logic

-

Calculate 6-period RSI and identify values above 90 (overbought) and below 10 (oversold).

-

When RSI is overbought, go long on a pullback to the 5-period EMA (low) within 6 bars.

-

When RSI is oversold, go short on a pullback to the 5-period EMA (high) within 6 bars.

-

The exit strategy is a moving take profit, with the initial target being the highest high/lowest low of the past 12 bars, updating on each new bar for a rolling exit.

-

The stop loss is X ATRs from the entry price (customizable).

Advantage Analysis

The strategy combines RSI extremes as momentum signals and pullback entries to capture potential reversal points in trends, with a high win rate.

The moving take profit mechanism locks in partial profits according to actual price action, reducing drawdowns.

The ATR stop helps effectively control single-trade loss.

Good robustness to apply across different markets and parameter sets for easy real trading replication.

Risk Analysis

A too-wide stop loss if ATR multiplier set too high, increasing loss per trade.

Moving take profit mechanism may reduce profit margin if prolonged consolidation occurs.

Missing trades if pullback extends beyond 6 bars.

Potential slippage or false breakout if major news events occur.

Optimization Directions

Test shortening entry bar count from 6 to 4 to improve entry rate.

Test increasing ATR multiplier to further control loss per trade.

Incorporate volume indicators to avoid losses from divergence in consolidation.

Enter on pullback break of 60min mid-point to filter noise.

Conclusion

The Momentum Pullback Strategy is an overall very practical short-term mean reversion approach, incorporating elements of trend, reversal and risk management for easy real trading while still carrying alpha-generating potential. Further stability enhancements are possible through parameter tuning and combining additional indicators. It represents a great boon for quant trading and is well worth learning and applying.

- 1