EMA Golden Cross Short-term Trading Strategy

Overview

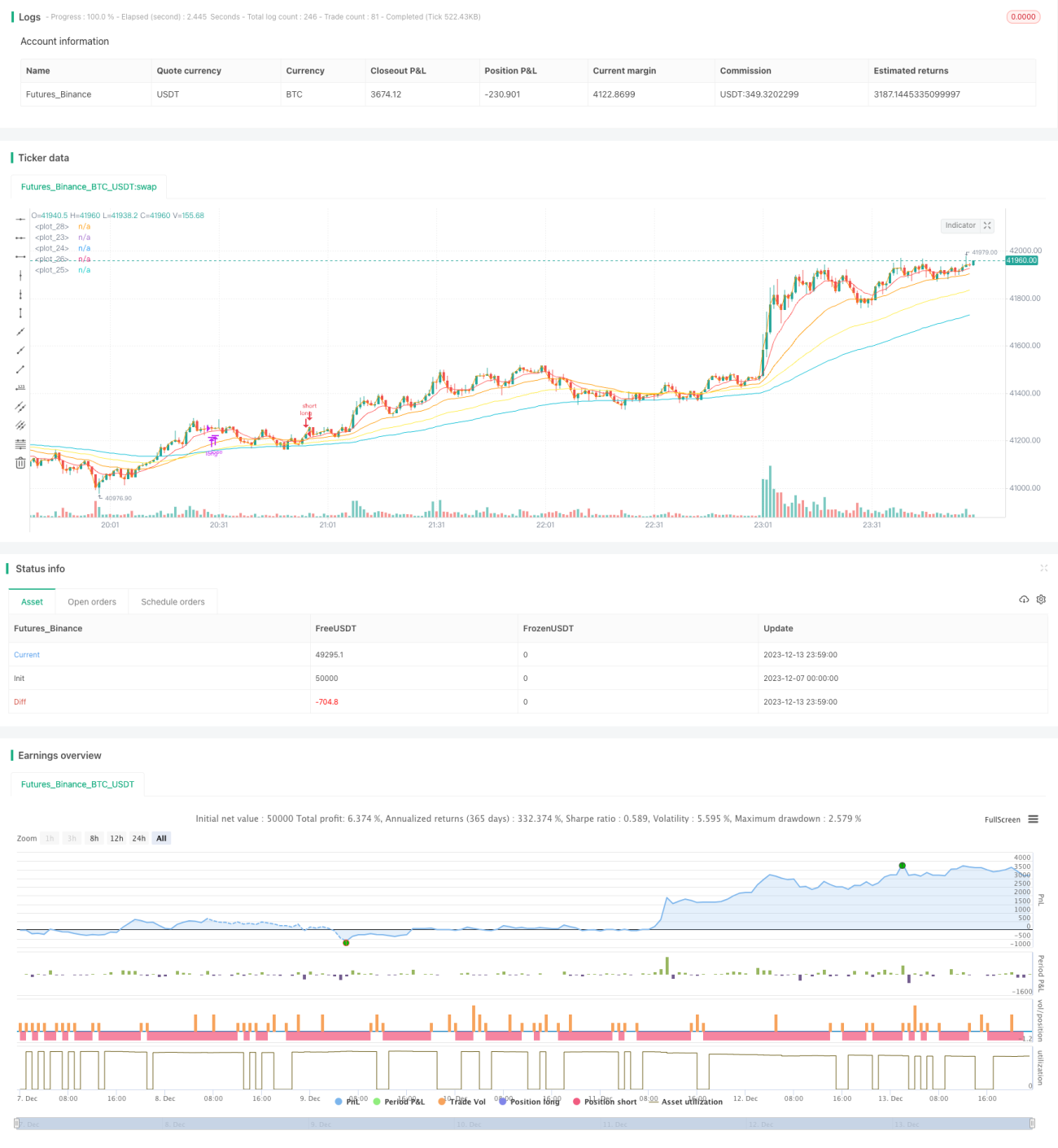

The EMA golden cross short-term trading strategy is a short-term trading strategy based on the EMA indicator. It uses EMA lines of different cycles to judge golden cross and dead cross trading signals, adopts shorter cycle EMA lines as entry signals, and longer cycle EMA lines as stop loss signals to realize a fast in and fast out short-term trading mode.

Strategy Principle

The strategy uses 4 EMA lines of different cycles, specifically 9, 26, 100 and 55 cycle EMA lines. The entry signal is to go long when the 9 cycle EMA line crosses over the 26 cycle EMA line; The exit stop loss signal is to close positions when the 100 cycle EMA line crosses below the 55 cycle EMA line. This allows fast entry and fast exit to avoid being trapped.

Advantage Analysis

- Using the EMA indicator to determine trends is reliable to avoid false signals.

- Adopting EMA combos of different cycles can capture short-term opportunities.

- The fast in and fast out short-term trading method avoids long-term bearing of losses.

Risk Analysis

- EMA lines themselves have laggingness which may miss the best entry timing.

- Short-term trading can easily increase trading frequency and commission burdens.

- Short-term trading requires higher psychological control skills from traders.

Optimization Directions

- EMA line cycle parameters can be adjusted to optimize profitability.

- Other indicators can be added to filter signals and improve win rate.

- Stop loss and take profit conditions can be set to control single trade risks.

Summary

In general, the EMA golden cross short-term trading strategy has the characteristics of simplicity, ease of operation and quick response. Through parameter optimization and signal filtering, its stability and profit level can be further improved. But short-term trading also raises higher requirements for traders' control capabilities. In conclusion, this strategy is suitable for investors with some trading experience to use in live trading.

- 1