X48 - DayLight Hunter Strategy Optimization and Adaptation

Overview

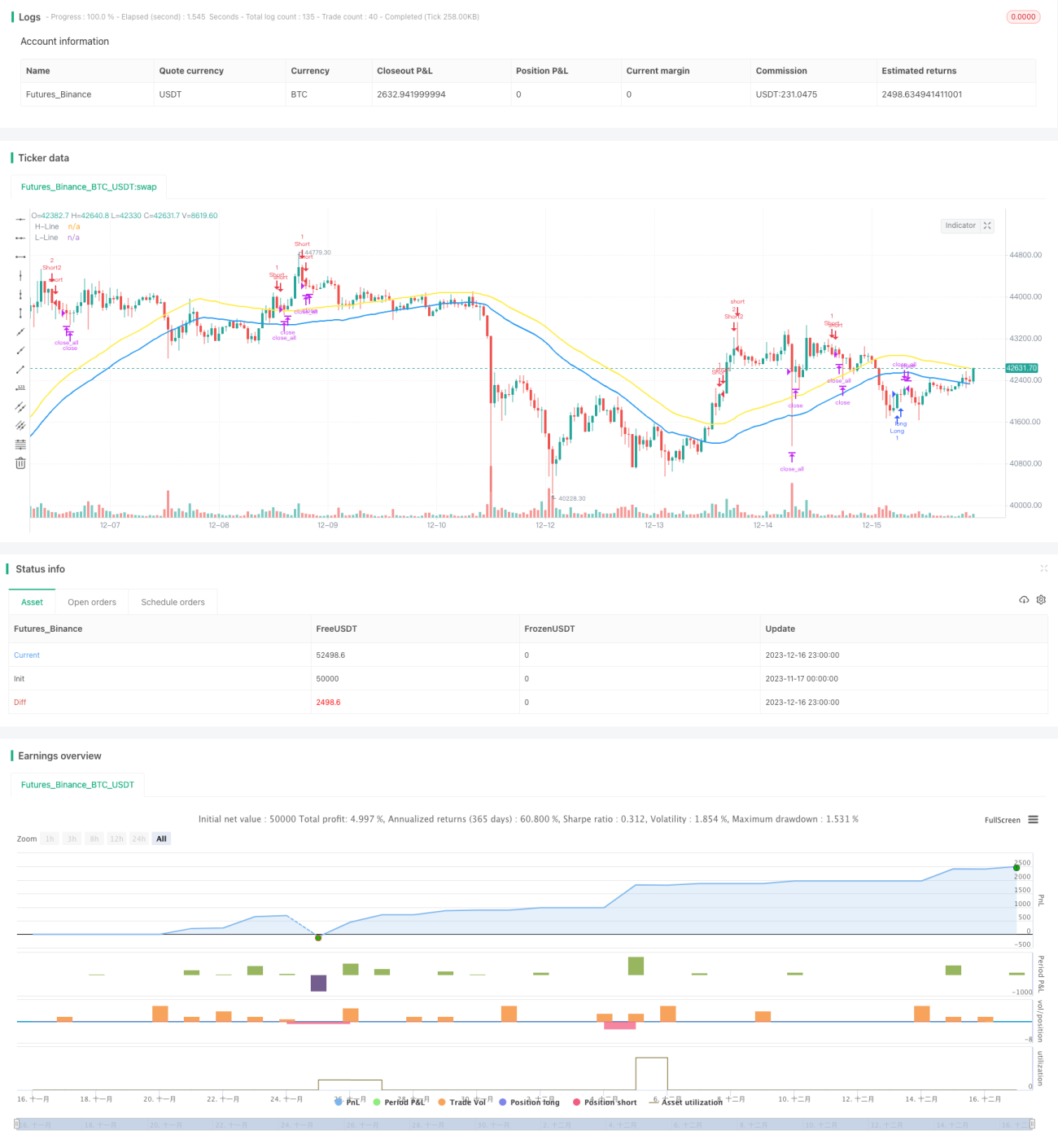

This strategy combines the classic Stochastic indicator and SMA indicator to achieve strong trend tracking capability. The core idea of the strategy is to identify trend direction signals with Stochastic indicator and filter with SMA indicator to improve signal quality. It also provides different risk modes to dynamically adjust risk and reward. In addition, the multi-timeframe judgement is utilized to optimize the entry timing and control trading risk.

Strategy Logic

- The strategy adopts an enhanced version of Stochastic indicator. The parameters include %K period, %K smoothing and %D smoothing to control the sensitivity.

- The SMA indicator parameters include Upper SMA and Lower SMA to filter signals for higher quality.

- Three risk modes are provided for selection based on risk preference, including Low Risk, Medium Risk and High Risk. The risk mode will impact the crossover threshold of Stochastic indicator to dynamically adjust risk and reward.

- Long signal is identified when Stoch crosses up the threshold and close price is below Lower SMA. Short signal is identified when Stoch crosses down the threshold and close price is above Upper SMA.

- Multi-timeframe judgement module verifies the signals across different time ranges to optimize entry timing and control trading risk.

Advantages

- The enhanced Stochastic indicator improves sensitivity for capturing market changes quickly.

- The dual SMA rail filtering mechanism effectively avoids fake signals and improves signal quality.

- Multiple risk modes allow users to flexibly adjust parameters based on their risk appetite.

- Multi-timeframe judgement optimizes the entry timing selection to reduce trading risk.

- The overall strategy framework is scientific, stable and adaptive.

Risks

- The strategy does not have a stop loss mechanism itself. Manual stop loss is needed to control the downside risk.

- High signal frequency may lead to over trading and increased transaction costs.

- The strategy is sensitive to parameters and risk mode settings which need optimization for best results.

- Large drawdowns may happen. It may not suitable for full position trading. Proper position sizing is important.

Solutions:

- Set proper stop loss ratio based on market volatility to maximize risk control.

- Adjust Stoch parameters to reduce signal frequency, or set minimum take profit to avoid unnecessary trades.

- Low Risk mode is recommended as baseline. Adjust other parameters based on backtest results.

- Control position sizing and average up exposure to reduce per trade risk.

Enhancement Opportunities

- Comprehensive parametric optimization on Stoch and SMA to find the optimal parameter combination.

- Increase the number of multi-timeframe judgements for more reference and better entry decisions.

- Introduce dynamic stop loss mechanisms like ATR Trailing Stop to better limit downside risk.

- Build signal filtration and confirmation mechanisms like volume to avoid traps.

- Add position sizing module to actively adjust position size based on market conditions to lower per trade risk exposure.

Summary

This strategy combines the strengths of Stochastic and SMA indicators to achieve strong trend tracking capability. The framework is solid and indicator application is fluid. By controlling parameters and risk modes, the nature of the indicators is restored for better stability. The multi-timeframe judgement also enhances adaptiveness across products and timeframes. Overall it has good versatility and huge potential for further optimizations and enhancements.

- 1