Gradient MACD Quant Strategy

Overview

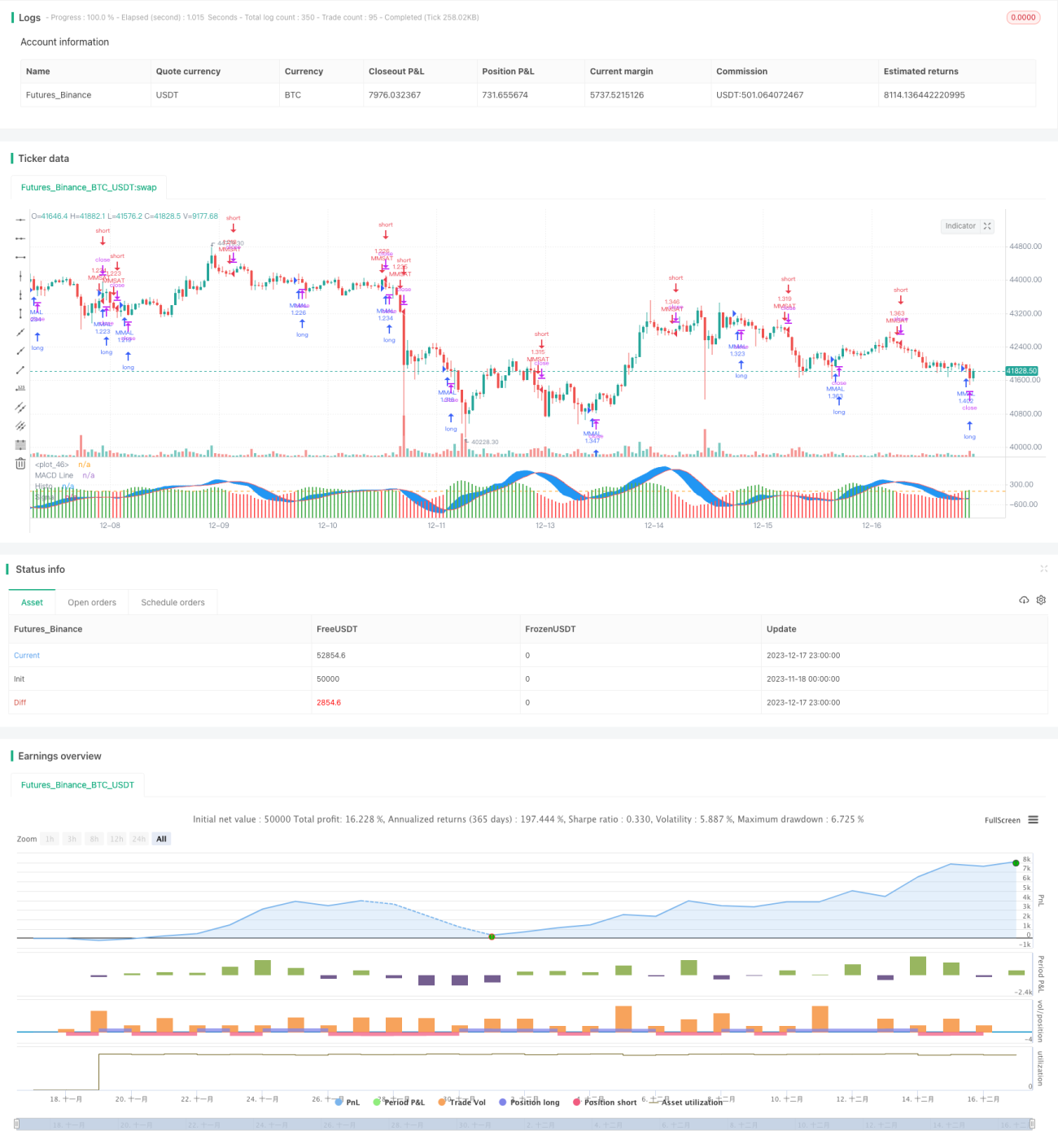

This strategy calculates Heikin-Ashi candlesticks to smooth price lines and combines MACD indicator to generate trading signals, implementing a quantitative strategy that tracks medium-to-long term trends.

Strategy Logic

-

Calculate Heikin-Ashi open, close, high and low prices to plot Heikin-Ashi candlesticks and smooth price trends.

-

Set MACD parameters: fast length 12, slow length 26, signal length 9.

-

Calculate DEA slow line, DEA fast line and MACD histogram. Plot MACD histogram.

-

Go long when MACD histogram crosses above 0; Go short when crossing below 0.

-

Add year, month and day filters to limit trading to specified time range.

Advantage Analysis

-

Heikin-Ashi candlesticks filter out market noise effectively to identify trends.

-

MACD provides clear trend trading signals.

-

Combining Heikin-Ashi and MACD improves signal quality and profitability.

-

Time filters help optimize trading schedule based on historical performance.

Risk Analysis

-

Potential large losses during trend reversal.

-

Improper MACD parameters may generate excessive worthless signals.

-

Rigid time filters may miss good trading opportunities.

Countermeasures:

-

Set stop loss/take profit to limit losses.

-

Optimize MACD parameters to determine best combination.

-

Add indicators to determine local trends.

Optimization Directions

-

Test different parameter combinations to find optimum.

-

Add stop loss mechanisms like trailing stop loss.

-

Add indicators like EMA, KDJ to determine reversal points.

-

Add volume indicators to avoid divergence.

Summary

This strategy smoothes price action with Heikin-Ashi candlesticks and determines trend direction and entry signals with MACD Tradingview indicator to implement a trend-following quant strategy. Compared with regular MACD strategies, it filters out some noise for clearer trend identification. Further enhancements on parameter optimization, stop loss, and combo indicators can improve its stability and profitability.

/*backtest

start: 2023-11-18 00:00:00

end: 2023-12-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("MACD ASHI BARS .v1 ", overlay=false,default_qty_type = strategy.percent_of_equity, default_qty_value = 100,commission_type=strategy.commission.percent,commission_value=0.1,slippage=1)

// Calculation HA Values - 1