AO Indicator Based Trend Following Strategy

Overview

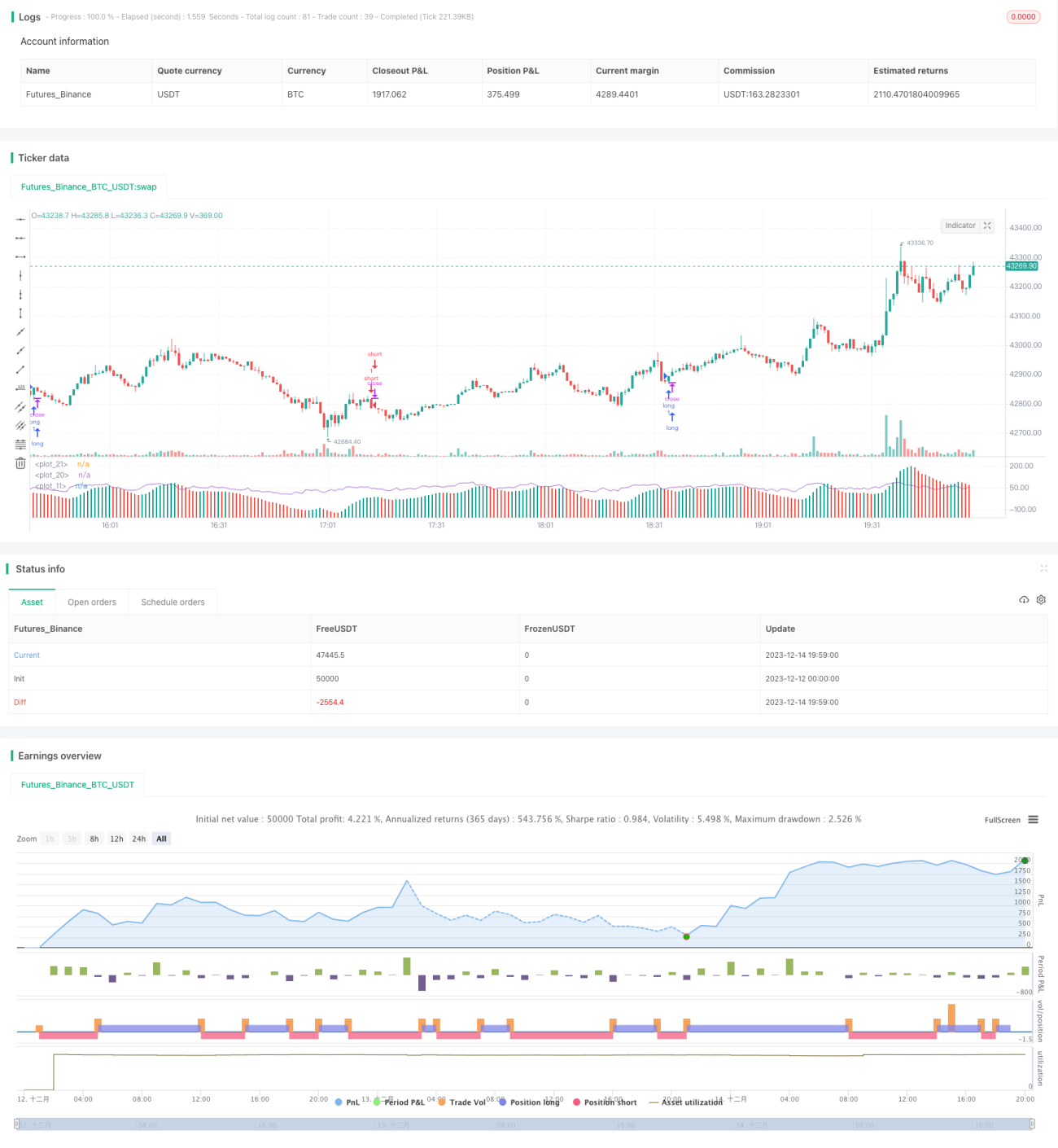

This strategy uses the Awesome Oscillator (AO) indicator to determine the trend direction and moving averages to confirm the trend. It belongs to the trend following strategy. It goes long when the AO indicator crosses above the 0 level and the fast MA crosses above the slow MA, and goes short when the AO crosses below the 0 level and the fast MA crosses below the slow MA, taking advantage of the directionality of trends to profit.

Strategy Logic

This strategy mainly relies on the AO indicator to determine the short-term trend direction. The AO indicator is calculated based on the difference between the 5-period and 34-period simple moving averages of the mid-price. It belongs to the Momentum category of indicators. When the AO is positive, it means the short-term MA is above the long-term MA, which should be interpreted as a bullish sign. When the AO is negative, it means the short-term MA is below the long-term MA, which should be interpreted as a bearish sign.

Therefore, the AO indicator can effectively determine the direction of the trend. When the AO crosses above the 0 level, it signals that the market trend has turned bullish and we should go long. When the AO crosses below the 0 level, it signals that the market trend has turned bearish and we should go short.

In addition, this strategy also incorporates the 20-period and 200-period moving averages. The slope of these two MAs represents the direction of the medium to long-term trend. Judging only by the AO indicator for the short-term trend direction is not enough, confirmation from the mid-long term trend is also needed, hence the addition of the MA crossover rules.

When the fast MA crosses above the slow MA, the mid-long term trend turns bullish, we go long when the AO crosses above 0 to ride the uptrend. When the fast MA crosses below the slow MA, the mid-long term trend turns bearish, we go short when the AO crosses below 0 to ride the downtrend.

Advantages

- Accurately determining short-term trend direction using the AO indicator

- Adding MA filters to confirm mid-long term trend, effectively avoiding false breakouts

- Fast profits, suitable for short-term trading

Risk Analysis

- Risk of failed entry when going short. Price may continue going up for some time after AO crosses below 0 and MA signals sell before turning down.

- Risk of failed entry when going long. Price may continue going down for some time after AO crosses above 0 and MA signals buy before turning up.

- Risk of distorted AO signals at major technical levels.

Improvement Directions

- Test different MA combinations to find better settings, e.g. 10- and 50-period MAs

- Add other indicators like RSI for signal confirmation

- Optimize stop loss percentage for better risk/reward ratio

Conclusion

This is a simple trend following strategy. Using the AO to determine short-term trend direction confirmed by mid-long term MAs is logically sound. The combination of AO and MAs sees widespread usage and is relatively mature. This strategy is also very reliable. Further optimization of parameters and other indicators can improve strategy performance.

- 1