Flexible MA/VWAP Crossover Strategy with Stop Loss/Take Profit

Overview

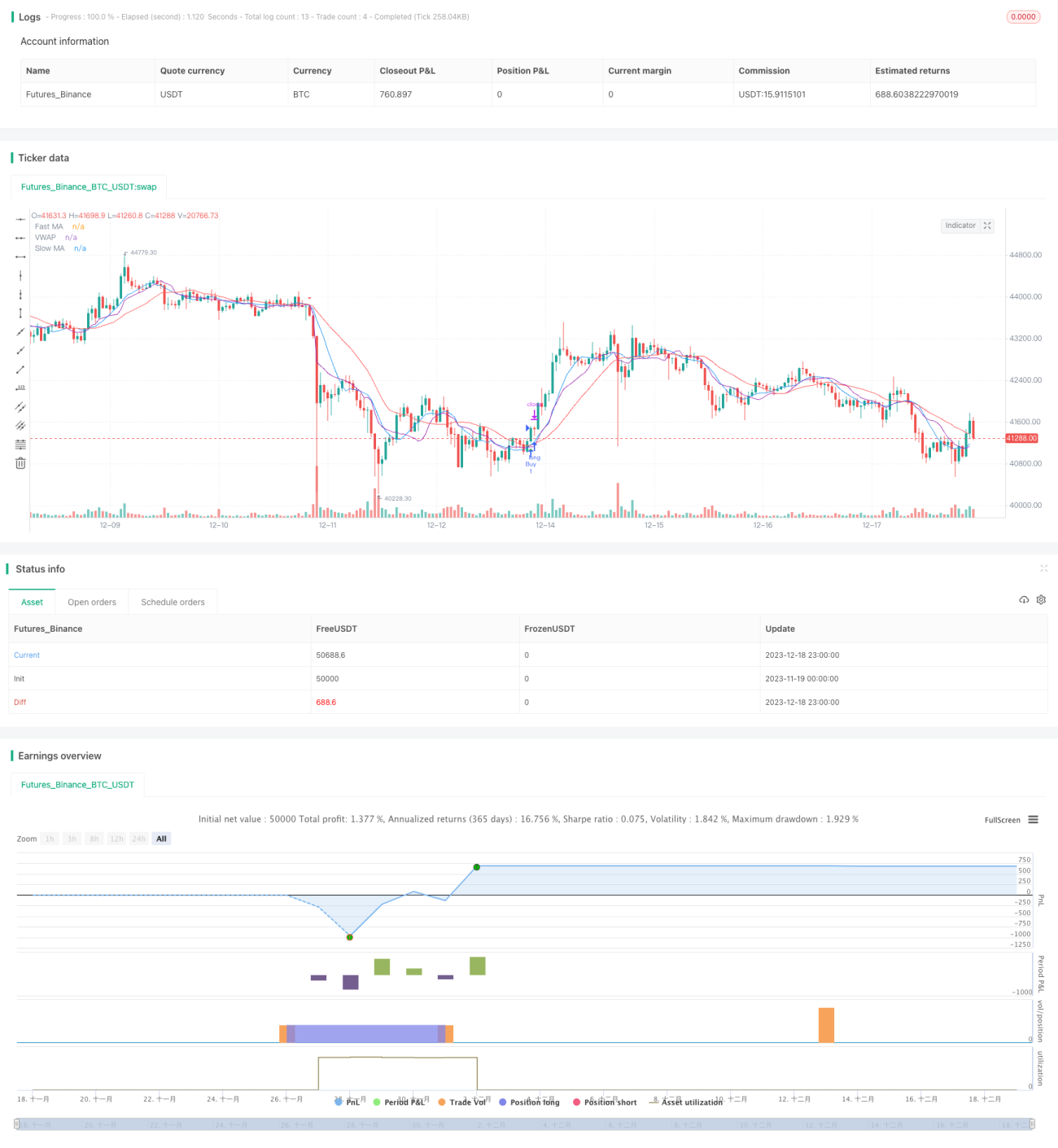

This strategy identifies crossovers between fast moving average, slow moving average and volume weighted average price (VWAP) to capture potential price movements. It triggers buy signals when fast MA crosses above VWAP and slow MA, and sell signals when fast MA crosses below VWAP and slow MA.

Strategy Logic

The strategy combines the strengths of moving averages and VWAP. Moving averages can effectively filter out market noise and determine trend direction. VWAP reflects intentions of big money more precisely. Fast MA captures short-term trend while slow MA filters out false signals. When fast MA crosses above slow MA and VWAP, it indicates bullish short-term trend and triggers buy signals. Below crossover triggers sell signals.

Advantage Analysis

- Dual MA filter reduces false signals

- VWAP accurately judges intentions of big money

- Flexible MA parameters adapt to different periods

- Effective risk control with stop loss/take profit

Risk Analysis

- Whipsaw markets may generate multiple false signals

- Inaccurate VWAP parameters fail to judge fund intent

- Stop loss too tight unable to trace trends, too loose risks excess

Optimization Directions

- Optimize MA and VWAP parameters for different market conditions

- Additional filter signals with RSI

- Dynamic stop loss/take profit ratios

Conclusion

This strategy integrates the strengths of moving averages and VWAP, identifies crossover signals through dual filtering, and effectively controls risks with flexible stop loss/take profit mechanisms. It is a recommended trend following strategy.

- 1