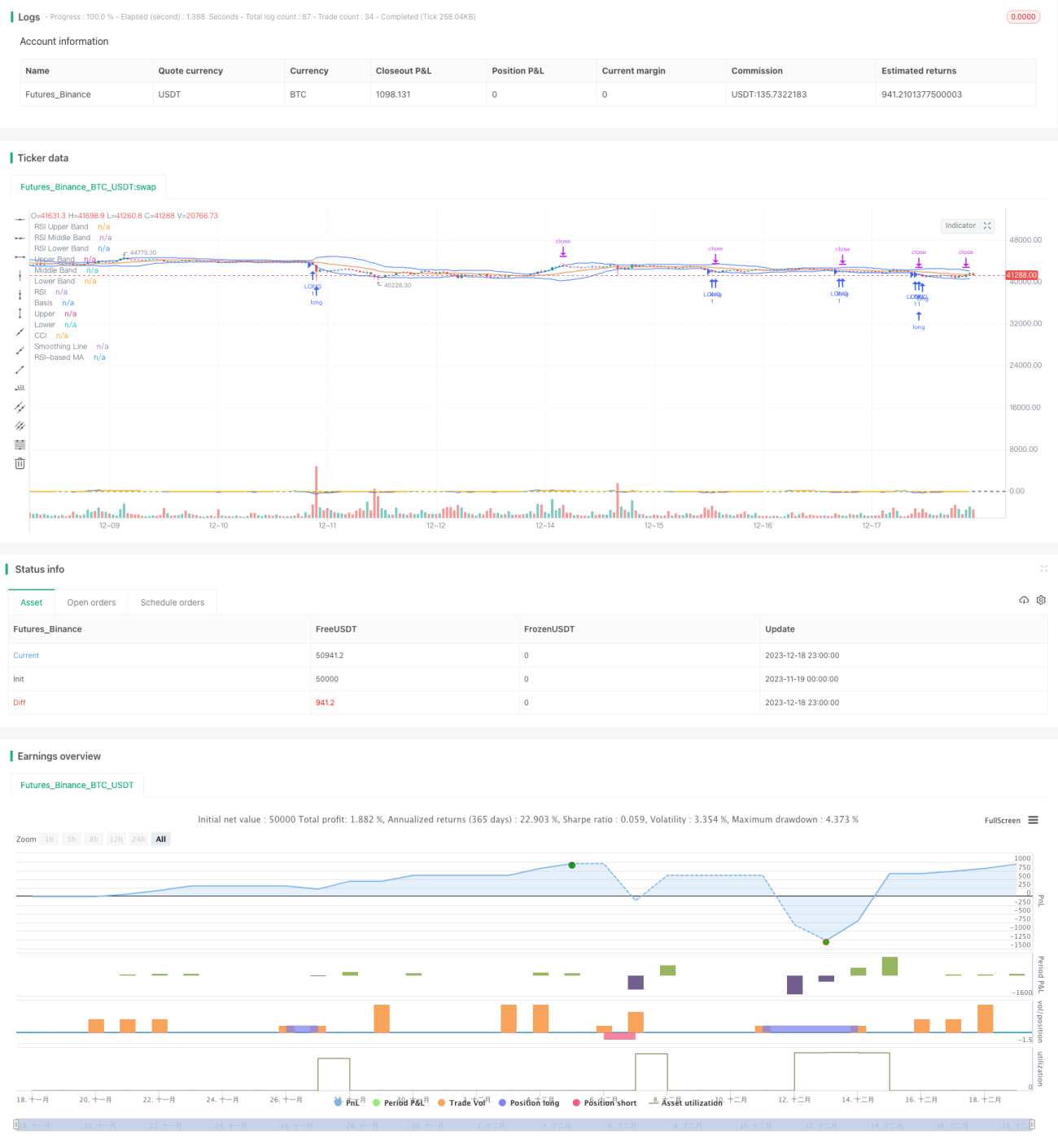

概述

本策略结合使用布林带、相对强弱指数(RSI)和商品路径指数(CCI)三个指标,寻找其交叉信号,发出买入和卖出信号。该策略旨在发现市场的超买超卖现象,在反转点入场,以期获得较好的投资回报。

策略原理

布林带

布林带由中轨、上轨和下轨组成。中轨通常采用20日移动平均线。上轨和下轨分别是中轨之上和之下两个标准差的位置。如果价格接近下轨时,被视为超卖信号。如果价格接近上轨时,被视为超买信号。

RSI指标

RSI指标反映了一段时间内收盘价格上涨和下跌的速度变化,用来测量买盘和卖盘的力量对比。RSI值在0至30时为超卖区,在70至100时为超买区。当RSI从超买区下降时可以作为卖出信号,当RSI从超卖区上涨时可以作为买入信号。

CCI指标

CCI指标用来衡量股票价格偏离其平均价格的程度。其中,+100代表价格远高于平均价,为超买;-100代表价格远低于平均价,为超卖。CCI能反映价格的极端情况。

策略交叉信号

本策略以布林带判断价格短期内是否超买超卖,以RSI指标判断买卖盘力量均衡情况,以CCI指标判断价格偏离程度。布林带、RSI和CCI指标同时给出买入/卖出信号时,发出交易指令。

策略优势

- 结合多种指标判断,减少假信号,提高信号准确度

- 发现市场转折点,捕捉反转趋势 的机会

- 各参数可自定义调整,适应不同市场环境

- 采用均线过滤CCI指标,减少噪声,提高稳定性

风险及解决方案

- 布林带、RSI和CCI指标都可能产生错误信号,造成交易亏损。可适当宽松参数,或增加其他指标进行验证。

- CCI指标对于曲折行情不太适用,可采用均线或波动率指标替代。

- 交易指令只有止损,没有止盈。可增加移动止盈来锁定部分利润。

优化方向

- 测试更多参数组合,找到最佳参数;

- 增加机器学习算法,实时优化参数;

- 增加止盈策略,设定目标利润;

- 结合更多指标,如MACD、KD等判断信号可靠性。

总结

本策略综合考虑了短期、中期和长期市场状况,通过布林带、RSI和CCI三个指标的交叉信号,判断市场反转的时机,属于较为稳健的反转跟踪策略。可通过参数调整、止盈方式等进一步优化,适用于多种市场环境。

策略源码

Pine

/*backtest

start: 2023-11-19 00:00:00

end: 2023-12-19 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(shorttitle="BBRSIstr", title="Bollinger Bands", overlay=true)

length = input.int(20, minval=1)

maType = input.string("SMA", "Basis MA Type", options = ["SMA", "EMA", "SMMA (RMA)", "WMA", "VWMA"])策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1