Dual-factor Quantitative Reversal Tracking Strategy

Overview

This strategy combines the 123 reversal pattern and the Awesome Oscillator indicator to implement dual-factor quantitative reversal tracking trading. The basic idea is to determine market reversal while combining the signal from the Awesome Oscillator to achieve more accurate entry timing.

The strategy is mainly suitable for medium-short term reversal trading. By multi-factor confirmation, it can effectively filter out false reversals and improve signal quality.

Strategy Principle

-

123 Reversal Pattern

Judge the relationship between the closing prices of the previous two days and the current closing price to form a "high-high-low" or "low-low-high" pattern, indicating a possible reversal signal.

At the same time, require the Stochastic indicator to be in the overbought or oversold area to further confirm the reversal signal and filter out false reversals.

-

Awesome Oscillator

The Awesome Oscillator is a momentum indicator built based on the difference between medium-term moving average and short-term moving average. When the fast line crosses the slow line downward, it is a sell signal; when it crosses upward, it is a buy signal.

This strategy adopts the indicator's judgment of bullish or bearish state to determine buy and sell points.

-

Dual-factor Confirmation

Through the dual confirmation of the 123 reversal pattern and Awesome Oscillator, false reversals can be effectively filtered out and the accuracy of entry timing can be improved.

Advantages of the Strategy

-

Using dual factors to determine reversal points can effectively filter out false reversal signals.

-

As a momentum indicator, the Awesome Oscillator can improve the accuracy of entry timing.

-

The addition of the Stochastic indicator can avoid the risk of buying at the peak and selling at the bottom.

-

Reversal strategies themselves have advantages in higher winning rate and risk-reward ratio.

Risks of the Strategy

-

The risk of reversal failure still exists. Using dual factors can reduce the probability, but cannot completely avoid this risk.

-

Over-optimization risk. Indicator parameters need to be tested and optimized for different markets to prevent over-optimization.

-

Risk of trading against the market trend. In a strong trending market, reversal strategies are prone to contrarian losses. Stop loss can be set to control risks.

Optimization Directions

-

Test and optimize combinations of indicator parameters to improve robustness.

-

Add stop loss strategy to control single loss.

-

Combine industry and sector selections to avoid inappropriate stock picking.

-

Optimize holding period to prevent blind trend following.

-

Test different moving average systems as auxiliary conditions.

Conclusion

In summary, while ensuring a certain profit probability and risk-reward ratio, this dual-factor quantitative reversal tracking strategy uses Awesome Oscillator as an entry timing tool, and avoids buying at the peak through the Stochastic indicator, which can effectively control the risks of reversal trading and has strong practicality.

However, the inherent risks of reversal strategies cannot be ignored. It is still necessary to optimize indicator parameters, set stop loss conditions, etc. to control risks. If used properly, this strategy can bring investors stable excess returns.

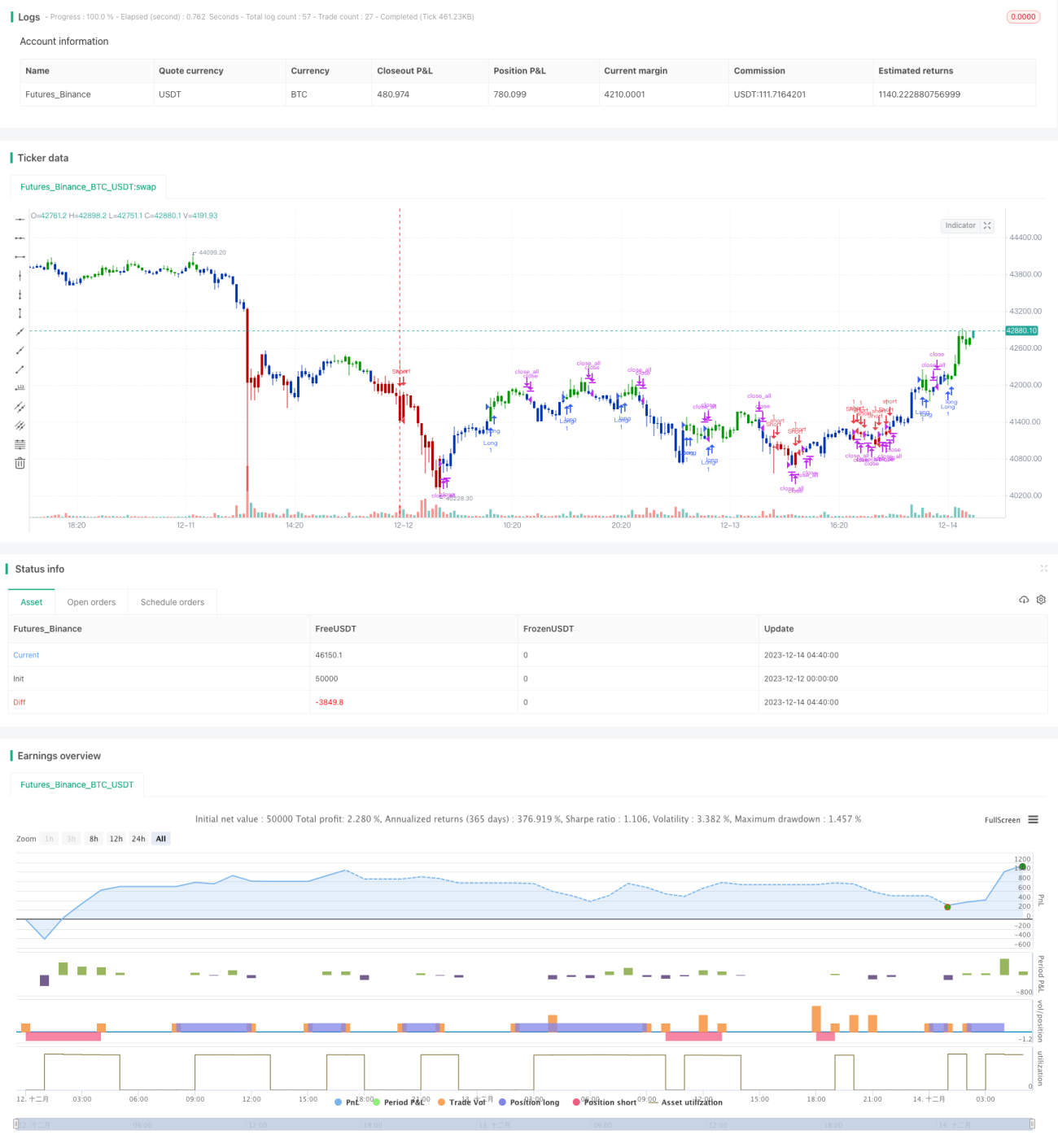

/*backtest

start: 2023-12-12 00:00:00

end: 2023-12-14 05:00:00

period: 20m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 12/08/2021

// This is combo strategies for get a cumulative signal. - 1