Automated Quantitative Trading Strategy Based on Inside Bar and Moving Average

Overview

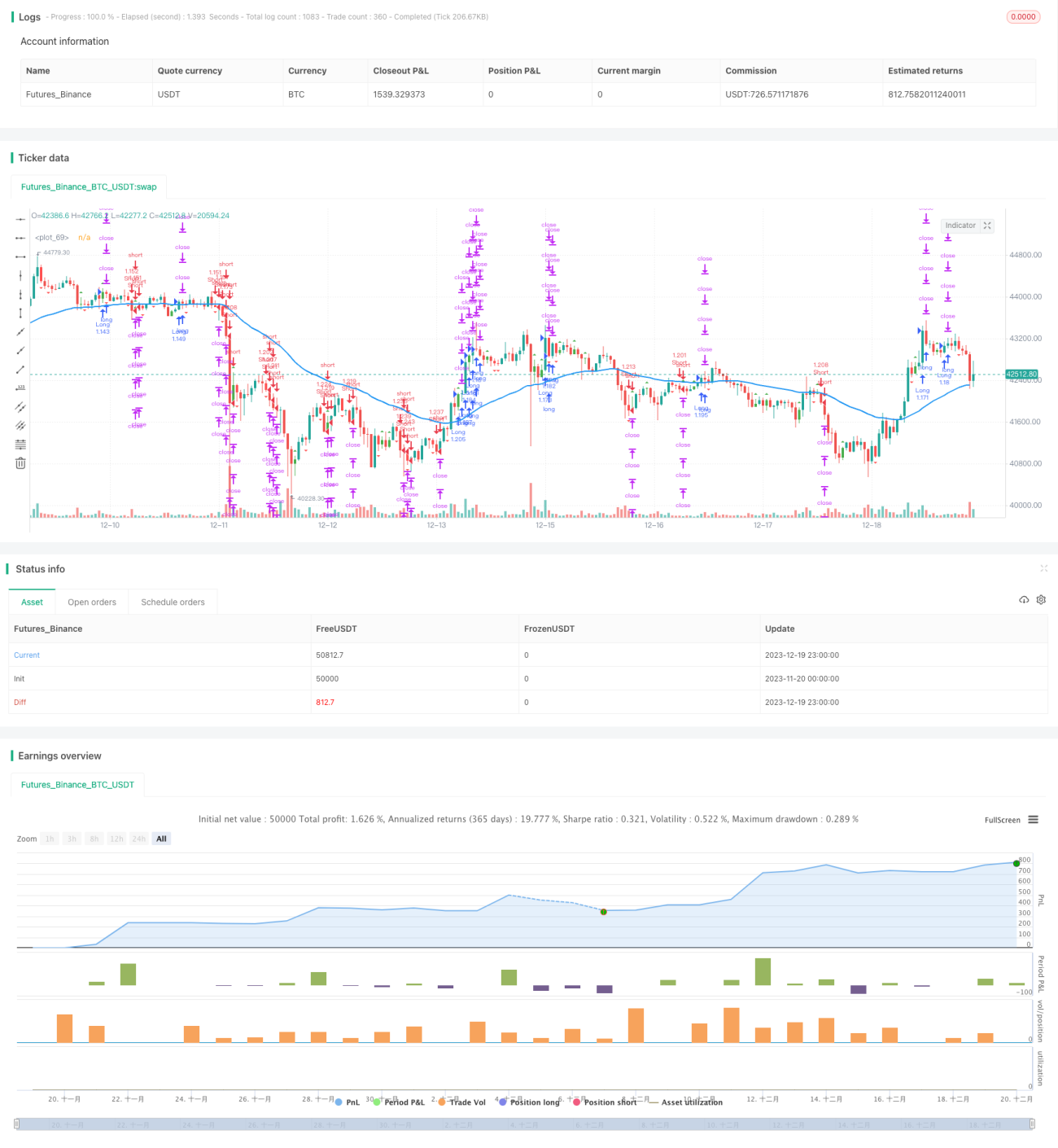

The core idea of this strategy is to combine inside bar patterns and moving average indicators to implement automated trading. When an inside bar pattern appears, it indicates that the current trend may be reversing. At this point, we use the position of the moving average line to determine the final trading direction.

Strategy Principle

-

Identify inside bar patterns. An inside bar refers to a candlestick where both the high and the low are within the real body of the previous bar. Based on the color of the real body, we can judge if it is a bullish or bearish inside bar.

-

Check the position of the moving average line. When an inside bar is found, if the price is above the moving average line, it is a bullish signal. If the price is below the moving average line, it is a bearish signal.

-

Combine the inside bar pattern and the moving average signal to determine the final trading direction. That is going short when the bearish inside bar breaks below the moving average line, and going long when the bullish inside bar breaks above the line.

Advantages of the Strategy

-

Combining technical indicators and price patterns improves the accuracy of trading decisions.

-

Inside bars themselves contain strong price reversal signals that can identify trend reversal points early.

-

The moving average filters out some noise and avoids getting caught in range-bound oscillations.

-

Fully automated trading greatly reduces the time and effort costs of manual trading.

Risks of the Strategy & Solutions

-

When prices oscillate around the moving average line, more false signals may appear, leading to over-trading. This can be reduced by optimizing the moving average parameters or adding filtering conditions.

-

This strategy works better in markets with clear trends. The performance may suffer in oscillating markets. Trend-judging indicators like ADX can be added to control the algorithm activation.

-

There is some time lag. Shortening parameters or optimizing moving average calculation methods may reduce the lag.

-

The risk of large drawdowns is considerable. Stop loss can control downside risk. Position sizing optimization also helps decrease drawdowns.

Directions for Strategy Optimization

-

Optimize inside bar determination period parameters to find the best combination.

-

Try different types of moving averages, like EMA and SMA, to decide the most suitable one.

-

Add auxiliary indicators like MACD and KDJ to enrich trading signals and improve accuracy.

-

Incorporate filtering indicators like ADX and ATR to control algorithm activation in unsuitable market environments.

-

Optimize position management, such as risk-based sizing, pullback sizing etc. to better control risk and pursue higher returns.

Conclusion

This strategy implements a fully-automated quantitative trading solution by dynamically tracking inside bar signals and moving average indicators. The signal generation is simple and clear for easy understanding and tracking. It performs well in markets with obvious trends. Further optimization of parameters and rules can enhance the stability and profitability.

- 1