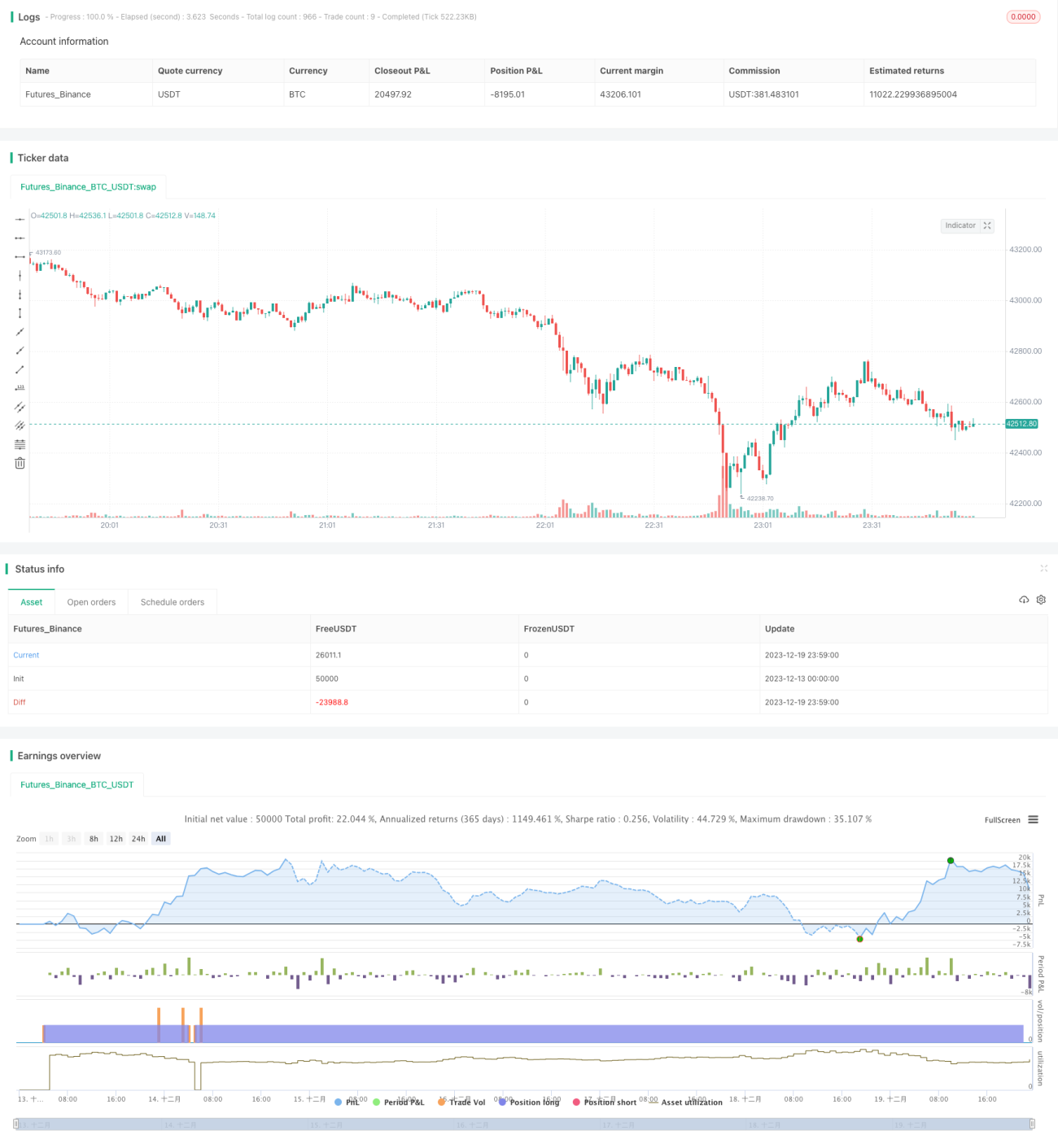

Mean Reversion Reverse Strategy Based on Moving Average

The strategy is named "Mean Reversion Reverse Strategy Based on Moving Average". The main idea is to buy when price breaks through key moving averages and take profit when reaching preset targets.

The main principle of this strategy is to capture rebound opportunities in range-bound markets by using the reversion of short-term moving averages. Specifically, when prices break through longer cycle moving averages (such as 20-day and 50-day MAs) and show signs of strong overselling, prices tend to rebound to some extent due to the mean reversion characteristic of market fluctuations. At this time, if shorter cycle moving averages (such as 10-day MA) show upward reversal signal, it would be a good timing to buy. In this strategy, it will buy when the close price is below 20-day MA while above 50-day MA, in order to capture its rebound with short-term MA reversal.

The specific entry logic is: Buy 1 lot when price breaks through 20-day MA, add 1 lot when breaking through 50-day MA, continue to add 1 lot when breaking through 100-day MA, and add up to 1 lot when breaking through 200-day MA, for a maximum of 4 lots. Take profit after reaching the preset targets. It also sets time and stop loss conditions.

Advantage Analysis

- Effectively identify short-term rebound opportunities by using the reversal characteristics of moving averages

- Reduce risks of single point by pyramiding orders

- Lock in profits by setting take profit targets

- Avoid false breakouts by using open price and previous low price filters

Risk Analysis

- May face reversal risks in long holding periods. Losses would expand if market continues to fall.

- MA signals may give false signals, leading to losses

- May fail to fully or partially take profits if profit target is not reached

Optimization Directions

- Test profitability and stability under different parameter settings

- Consider combining other indicators like MACD, KD to decide entries

- Choose suitable MA periods based on characteristics of different products

- Introduce machine learning algorithms to dynamically optimize parameters

Summary

In general, this is a classic and universal MA trading strategy. It correctly utilizes the smoothing feature of MAs, combined with multiple MAs to identify short-term buying opportunities. It controls risks by pyramiding orders and timely profit taking. But its response to market events like significant policy news may be more passive. This is something that can be further optimized. Overall, with appropriate improvements in parameter optimization and risk control, this strategy can obtain steady excess returns.

- 1