YinYang RSI Volume Trend Trading Strategy

Overview

This strategy is a trend following strategy that utilizes a combination of Relative Strength Index (RSI) and volume to identify trend direction and follow trends. Key points include:

- Using Volume Weighted Moving Average to calculate midline and incorporate volume information to determine trend midpoint

- Setting up buy zone and sell zone based on midline

- Using RSI information to adjust range of buy zone and sell zone

- Setting stop loss and take profit after entering buy/sell zones

- Having re-entry mechanism

Strategy Logic

This strategy uses the following indicators and parameters:

- Midline: Volume Weighted Moving Average of highest and lowest prices in certain periods to determine midpoint of the trend

- RSI: Relative Strength Index calculated over certain periods, converted into 0-1 range

- Buy Zone: Midline plus RSI adjusted amount at certain ratio, long entry when price enters

- Sell Zone: Midline minus RSI adjusted amount at certain ratio, short entry when price enters

- Take Profit Line: Midline

- Stop Loss Line: Certain percentage below buy zone/above sell zone

When price enters buy or sell zone, a corresponding direction order will be opened. Stop loss and take profit lines are then set. When take profit or stop loss is triggered, position will be closed. A re-entry mechanism is also set so that new orders can be opened when signal triggers again if configured.

Advantages

The advantages of this strategy include:

- Using both RSI and volume to identify trends, improving accuracy

- RSI parameterized adjustment makes buy/sell zone adapt better to actual trend

- Volume information assigns higher weight to price actions, making midline more accurate

- Having stop loss mechanism to control risks

- Allows re-entry, reducing risks of false breakouts

Risks

There are also some risks:

- Improper RSI and volume parameters may affect buy/sell zone accuracy

- Midline may fail to accurately determine trend, causing false breakout

- Stop loss too wide may lead to higher losses

- Re-entry may cause over-trading

Solutions:

- Adjust RSI and volume cycle to fit market conditions

- Use other indicators to verify buy/sell signals

- Tighten stop loss to limit losses

- Limit trades per day to prevent over-trading

Optimization

This strategy can be optimized by:

- Trying other indicators to verify signals e.g. candlestick, volatility indicators etc

- Adding position sizing mechanisms e.g. pyramiding winners

- Using machine learning algorithms to improve buy/sell zone accuracy

- Evaluating optimum parameters for stop loss and take profit

- Parameters need separate test and optimization for different products

Conclusion

In conclusion, this is a quantitative trend following strategy utilizing RSI and volume indicators. It has dual verification system to identify signals, stop loss/profit take to control risks, and re-entry mechanism to improve profitability. With parameter tuning and algorithm optimization, it can become a very practical trend trading strategy.

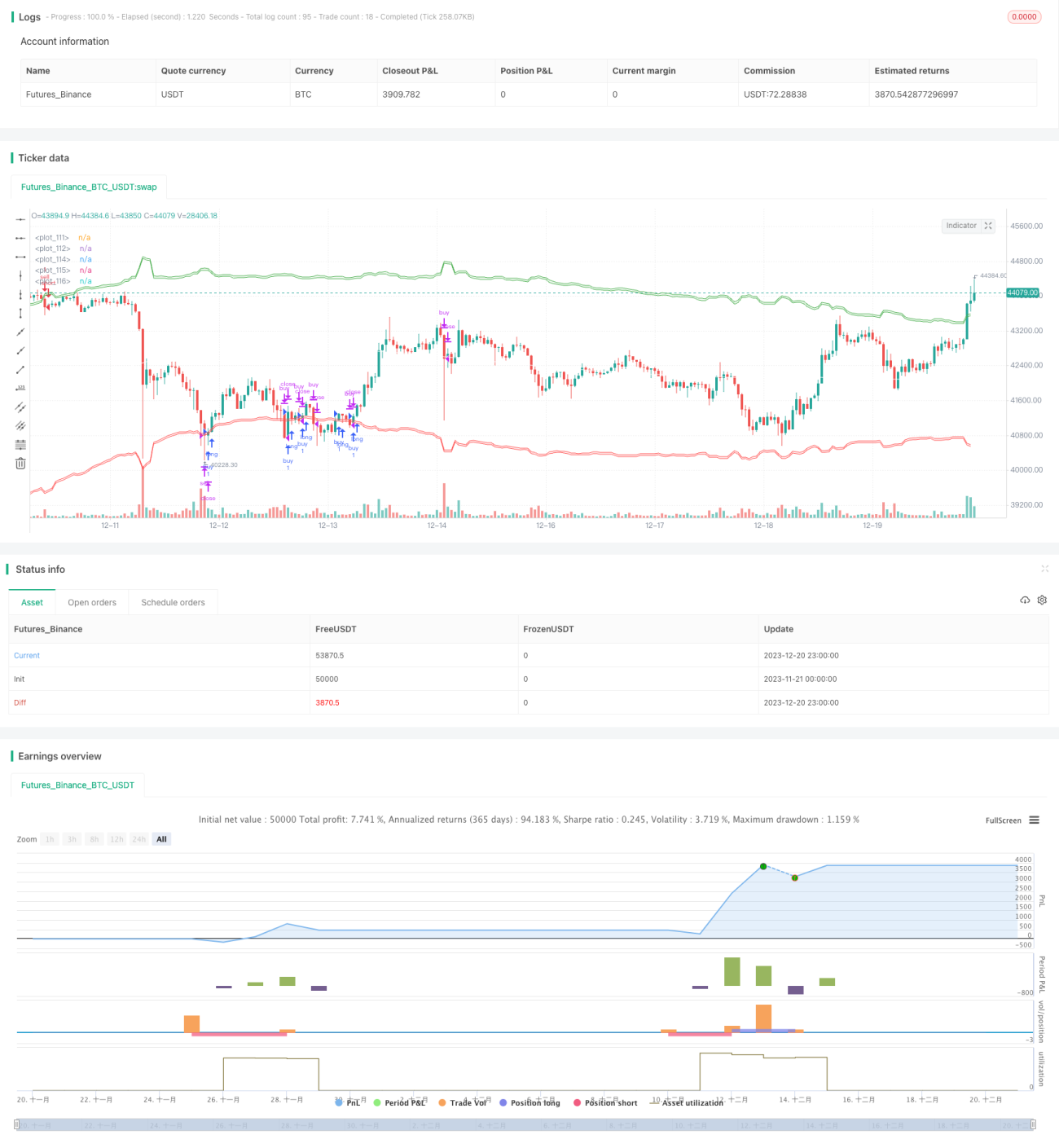

/*backtest

start: 2023-11-21 00:00:00

end: 2023-12-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

// @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@ @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

// @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@ ,@@@@@@@@@@@@@@@@@@@@@@@- 1