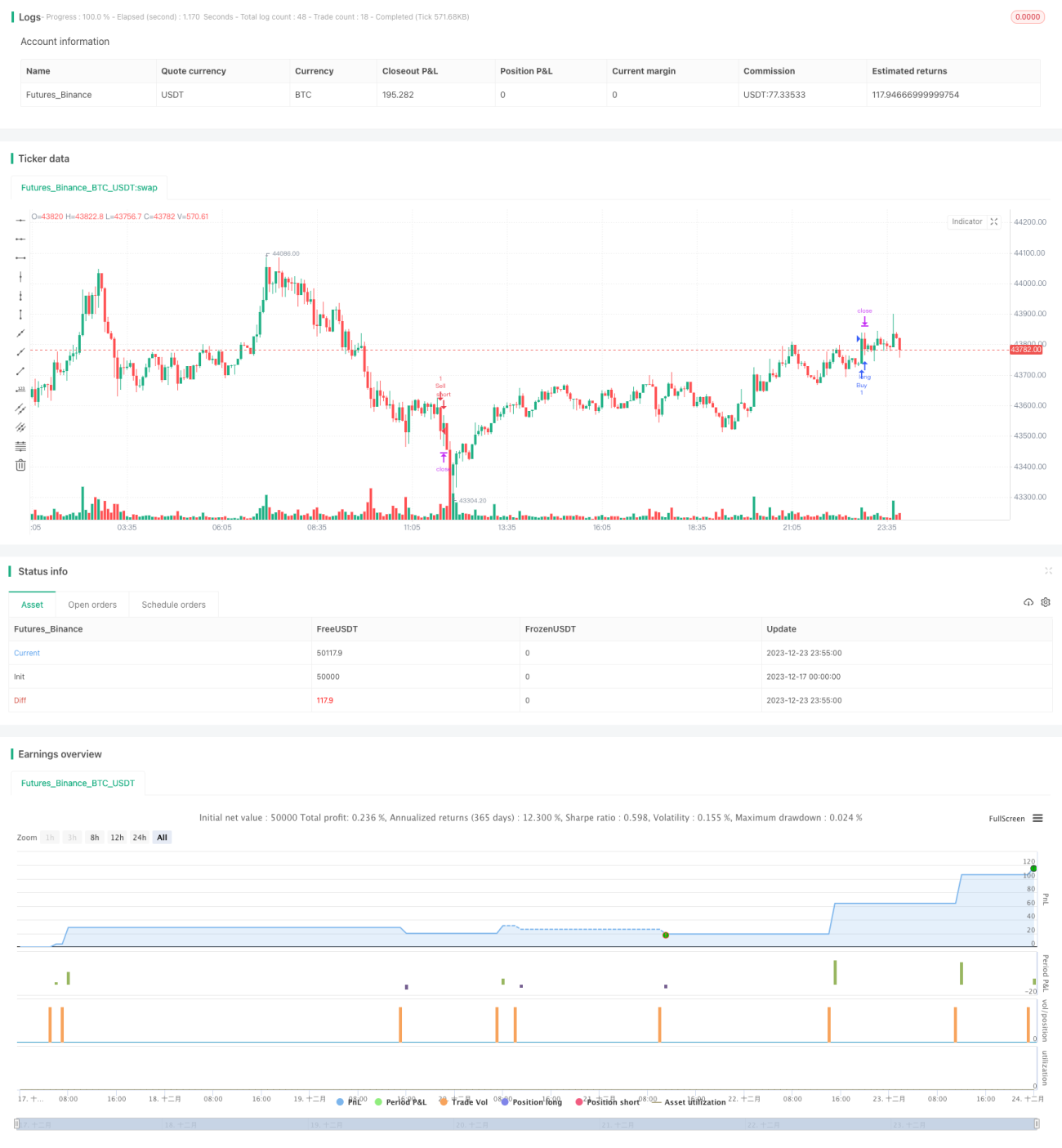

BBMA Breakthrough Strategy

Overview

The BBMA breakthrough strategy is a strategy that uses a combination of Bollinger Bands and moving averages to generate trading signals. The strategy uses both the upper and lower rails of the Bollinger Bands and the crossovers between the fast moving average and the ordinary moving average as entry signals. Go long when the price breaks through the upper rail of the Bollinger Bands and the fast moving average crosses above the ordinary moving average, and go short when the price breaks through the lower rail of the Bollinger Bands and the fast moving average crosses below the ordinary moving average.

Strategy Principle

This strategy is mainly based on the theory of Bollinger Bands and the theory of moving averages. Bollinger Bands are widely used in quantitative trading, consisting of middle rail, upper rail and lower rail. The middle rail is the simple moving average of closing prices over a certain period, and the upper and lower rails are respectively one standard deviation away from the middle rail. If the price is close to the upper rail, it indicates that the market may be overbought. If the price is close to the lower rail, it indicates that the market may be oversold.

The moving average is also a commonly used technical indicator, mainly used to judge the trend and judge the inflow and outflow of main funds. The fast moving average can capture price changes faster, and the ordinary moving average is more stable. When the fast moving average crosses above the ordinary moving average, it is called the golden cross, indicating that the market may enter an upward trend.

This strategy takes into account both Bollinger Bands theory and moving averages theory. It determines market entry and exit points through the combination signal of price breaking through the upper and lower rails of Bollinger Bands and special crossovers between fast and slow moving averages, and uses it as the entry signal to guide trading direction.

Advantages of the Strategy

-

Using Bollinger Bands theory to determine market entry and exit points is conducive to capturing price reversal opportunities.

-

Comprehensively considering the crossover signals of fast and ordinary moving averages avoids false breakouts.

-

Establishing stop loss and take profit points helps to strictly control risks.

-

Sufficient backtest data, high rate of return, good win rate.

Risks of the Strategy

-

Improper parameter settings of Bollinger Bands may cause wrong trading signals.

-

The lag of moving average cross signals may lead to unnecessary losses.

-

The stop loss point is set too loose to effectively control single losses.

-

Extreme market conditions may break through stop loss points.

Optimization Directions of the Strategy

-

Optimize Bollinger Bands parameters to find the best combination.

-

Evaluate whether to introduce other auxiliary indicators to filter signals.

-

Test and optimize moving stop loss strategies to further control risks.

-

Evaluate whether to use time or price breakthrough methods for stop loss.

Summary

The BBMA breakthrough strategy integrates the use of Bollinger Bands and moving average theory to judge trading signals. This strategy has good stability, high returns, and controllable risk levels. Parameters optimization and risk control measures can further improve the win rate and return on investment of the strategy. The strategy is suitable for medium and long term position holders.

- 1