Quantitative Trading Strategy Based on RSI Indicator and Moving Average

Overview

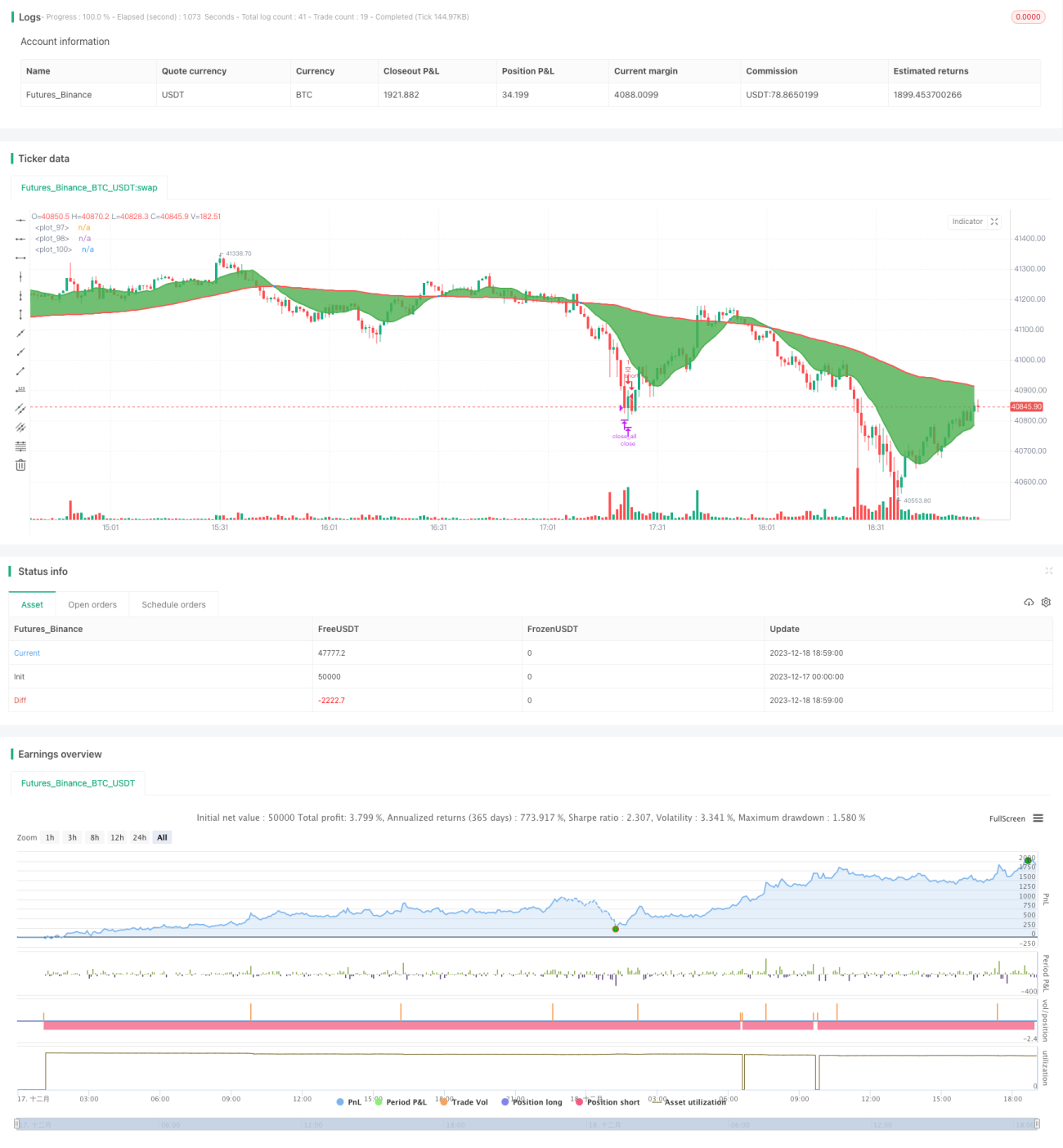

The strategy is named "Quantitative Trading Strategy Based on RSI Indicator and Moving Average". It utilizes RSI indicator and moving averages as trading signals to implement a quantitative trading strategy that makes reversal operations under trend background. Its core idea is to open positions when price reversal signals occur and take profit when overbought or oversold.

Strategy Principle

The strategy mainly uses RSI indicator and fast/slow moving averages to determine price trends and reversal timing. Specifically, it firstly calculates the fast moving average (SMA) and slow moving average. When the fast SMA crosses over the slow SMA, a buy signal is generated. When the fast SMA crosses below the slow SMA, a sell signal is generated. This indicates the trend of the price is changing.

At the same time, this strategy calculates the RSI indicator to determine whether the price is in an overbought or oversold state. Before opening positions, it will judge whether the RSI indicator is normal. If the RSI exceeds the set threshold, it will suspend opening positions and wait for the RSI to fall back before opening positions. This can avoid establishing positions at unfavorable overbought and oversold timing. On the other hand, after taking positions, if the RSI exceeds the set take profit threshold, it will close positions to take profits. This can lock trading gains.

By collaborating RSI indicator with moving averages, positions can be opened when price reversal signals occur. And by taking profit when overbought or oversold, a quantitative trading strategy that makes reversal operations for profits under price trend background can be implemented.

Advantages

The strategy has the following advantages:

-

Accurately open positions when price reversal occurs. Using moving average golden cross as buy signal and death cross as sell signal can accurately capture price trend reversal opportunities.

-

Avoid unfavorable opening positions timing. By judging overbought and oversold conditions through RSI indicator, it can effectively prevent establishing positions when price fluctuates excessively in the short term, avoiding unnecessary floating losses.

-

Risks can be well controlled. RSI take profit can keep positions within reasonable profit range and effectively control trading risks.

-

Easy to optimize parameters. SMA periods, RSI parameters etc. can be flexibly adjusted to adapt to different market environments.

-

High capital utilization efficiency. Frequent trading can be carried out during trend consolidation and shock stages, making efficient use of capital.

Risk Analysis

The strategy also has the following risks:

-

Tracking error risk. Moving averages as trend judgment indicators have certain lags, which may lead to inaccurate timing of opening positions.

-

Frequent trading risk. In oscillating markets, it may lead to excessively frequent openings and closings of positions.

-

Parameter tuning risk. SMA periods and RSI parameters need repeated testing and adjustment to adapt to markets. Improper settings may affect strategy performance.

-

Take profit risk. Improper RSI take profit settings may also lead to premature exit of positions or continued rise after take profit exit.

Optimization Directions

The optimization directions are as follows:

-

Try using MACD, Bollinger Bands and other indicators combined with RSI to make signals more accurate and reliable.

-

Increase machine learning algorithms to automatically adjust parameters based on historical data, reducing parameter tuning risks.

-

Increase optimization mechanisms for take profit strategies to make take profit more intelligent and adaptable to market changes.

-

Optimize position management strategies by dynamically adjusting position sizes to reduce risks of single trades.

-

Combine high-frequency data and use tick-level real-time data for high-frequency trading to improve strategy frequency.

Conclusion

In summary, this strategy uses trading signals generated by RSI indicator and moving averages to implement a quantitative strategy that makes reversal operations during trend runs. Compared to using moving averages alone, by adding RSI indicator judgments, this strategy can effectively prevent unfavorable opening positions timing and control trading risks through RSI take profit. To some extent, it improves the stability of the strategy. Of course, there are still room for improvements for this strategy. In the future, it can be optimized in aspects like more indicator combinations, automatic parameter optimization, position management, etc. to make strategy performance even better.

- 1