Oscillating Long-Short RSI Crypto Switching Strategy

Overview

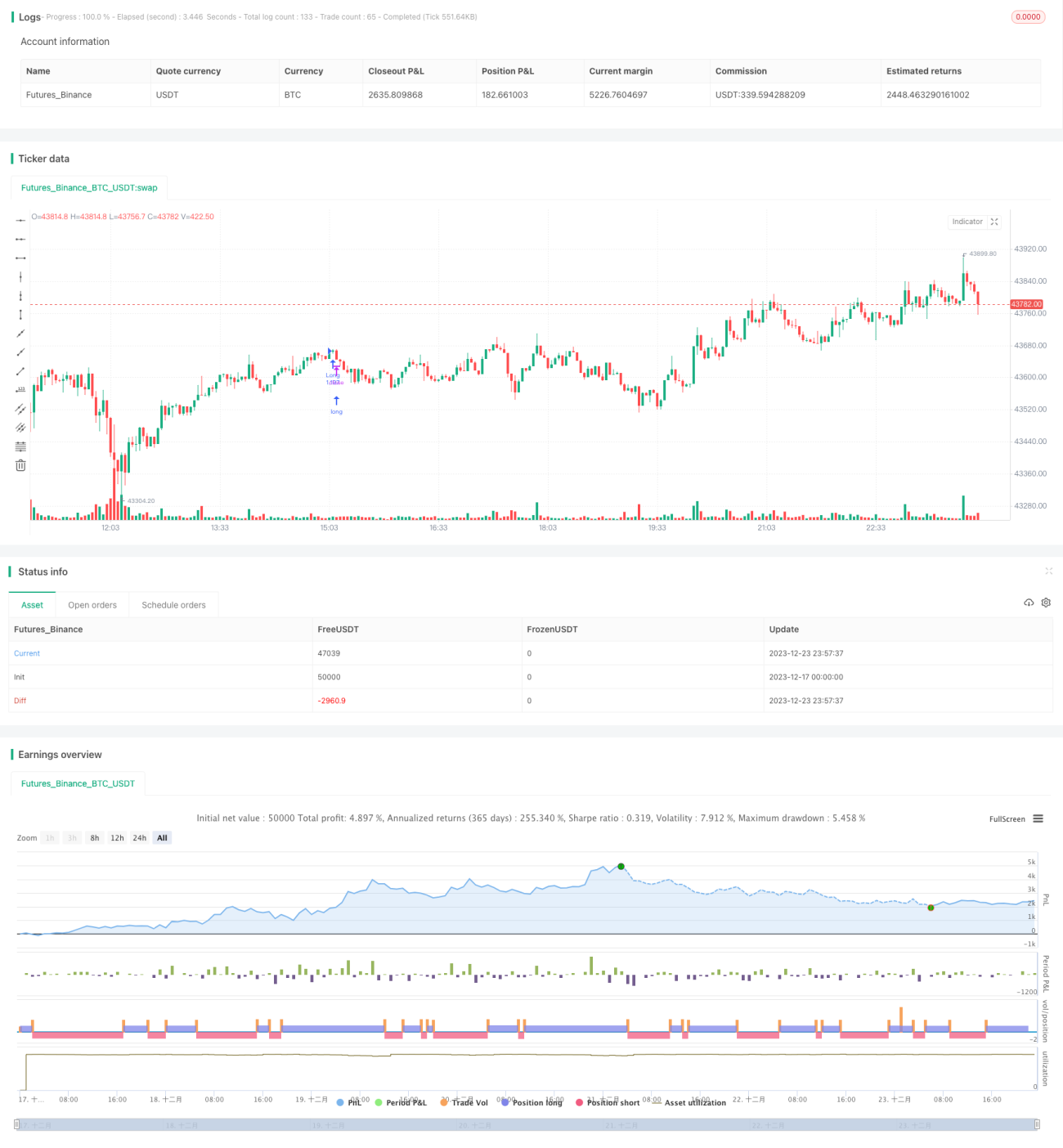

The Oscillating Long-Short RSI Crypto Switching Strategy is a quantitative trading strategy designed for cryptocurrencies. It combines the technical indicator RSI with the ICHIMOKU indicator to identify long and short signals during price oscillations and achieve buying low and selling high. It is suitable for medium to long term timeframes such as 3-4 hours or longer.

Strategy Logic

The strategy is mainly based on the following indicators and rules:

ICHIMOKU Indicator

- Tenkan Line: Midpoint of highest and lowest price of last 20 bars

- Kijun Line: Midpoint of highest and lowest price of last 50 bars

- Senkou A Line: Midpoint of Tenkan and Kijun Line

- Senkou B Line: Midpoint of highest and lowest price of last 120 bars

- Chikou Line: Closing price of 30 bars ago

RSI Indicator

- Range from 0 to 100

- Above 50 indicates bullish signal, below 50 indicates bearish signal

Entry Rules

Long entry: Tenkan cross above Kijun (golden cross) and price breaks through Senkou A&B Lines, with RSI above 50 at the same time

Short entry: Tenkan cross below Kijun (death cross) and price breaks down Senkou A&B Lines, with RSI below 50 at the same time

Exit Rules

Exit with opposite signal

The strategy takes into account the medium to long term trend, short term capital flow and overbought/oversold conditions to capture reversal opportunities during oscillation. It also sets stop loss rules to avoid huge losses.

Advantage Analysis

1. Judgment based on multiple indicators ensures high certainty

The strategy considers ICHIMOKU’s trend and support/resistance judgment, RSI’s overbought/oversold conditions, as well as capital flow based on the direction of candle body. This ensures reliable signals.

2. Suitable for oscillation, frequent profit-taking

Cryptocurrency market has large fluctuations. This strategy can fully capture reversal opportunities during oscillations and achieve frequent buying low and selling high.

3. Prevent chasing rises and beating retreats, controllable risk

The strategy comprehensively considers medium and long term trends and short term situations to avoid the risk of chasing rises and beating retreats. Meanwhile, stop loss prevents risk.

Risk Analysis

1. May miss some trending opportunities

The strategy focuses mainly on reversal, which may lead to frequent whipsaws during prolonged trending phases.

2. Single symbol, unable to diversify risk

The strategy trades only a single symbol and cannot diversify against systematic market risk.

3. Stop loss triggered during extreme moves

During extreme market conditions like gap or spikes, stop loss may be triggered forcing exit.

Optimization Directions

1. Add stop loss for lower single loss

Moving stop loss or percentage stop loss can be used to lock in profits and prevent full retracement.

2. Correlate with indexes to diversify market risk

Look for trading opportunities among highly correlated symbols to diversify systematic market risk.

3. Additional filters to reduce invalid trades

Filters like price volatility or volume changes can be added to avoid invalid reversal signals and improve profitability rate.

Conclusion

The Oscillating Long-Short RSI Crypto Switching Strategy combines ICHIMOKU and RSI indicators to identify reversal points for cryptocurrencies, suitable for buying low and selling high profit-taking during oscillations. It also sets stop loss rules to control risk. The strategy can be further enhanced by optimizing stop loss mechanism, diversifying risks through correlation and adding conditional filters, worth live testing.

- 1