策略原理

该策略使用三条低时延移动平均线,包括12周期、26周期和55周期的低时延tema均线。这三条均线分别代表:快速均线、中速均线和慢速均线。当快速均线上穿中速均线时产生买入信号;当快速均线下穿中速均线时产生卖出信号。这样通过三条均线的交叉来判断市场买卖点,实现高频交易。

代码中定义了模板函数tema()来计算低时延tema均线。其计算公式为:TEMA = 2*EMA - EMA(EMA),使用二次指数移动平均线EWMA来计算,本质上是一种双重指数平滑移动平均线,主要优点是大大降低了滞后。这样可以更快速地响应价格变化,提高交易信号判断的实时性。

具体来说,该策略的入场判断为:快速均线上穿中速均线且快速均线高于慢速均线时产生买入信号;快速均线下穿中速均线且快速均线低于慢速均线时产生卖出信号。

优势分析

该策略最大的优势在于出入场判断快速准确。三均线低时延设计大大减小了滞后,能够快速响应价格变化。同时使用三均线进行交叉判定,避免了误判。

另外,该策略适合高频交易,可以捕捉短线价格波动获利。通过快进快出的操作模式,可以在波动较大的市场中获利。

风险分析

该策略最大的风险在于可能出现超短线套利。三均线低时延设计决定了它对价格变化极为敏感,在某些市场中会出现超短线震荡。这时就很容易被套住。

另外,高频交易需要支付较多的手续费和滑点。如果获利能力不足,很容易被交易费用反向套利。

此外,该策略对交易者的实时监控能力要求较高,需要及时更新止损点和止盈点。

优化方向

该策略可以从以下几个方面进行优化:

-

优化三均线的周期参数,使其更好地适应不同市场的特点;

-

增加波动性指标或者交易量指标来确认信号,避免在震荡行情中被套;

-

结合更多因子来设定止损止盈机制,实现动态跟踪;

-

优化仓位管理,通过资金管理手段控制单笔风险;

-

结合机器学习算法来动态优化策略参数。

总结

本策略为三均线低时延快速交易策略。其通过低时延设计,实现快进快出,适合高频交易捕捉短线机会。该策略最大优势是信号判断快速准确,最大劣势是容易在震荡行情中被套。本文通过详细的原理剖析、优势分析、风险分析和优化探讨,全面概述了该交易策略。

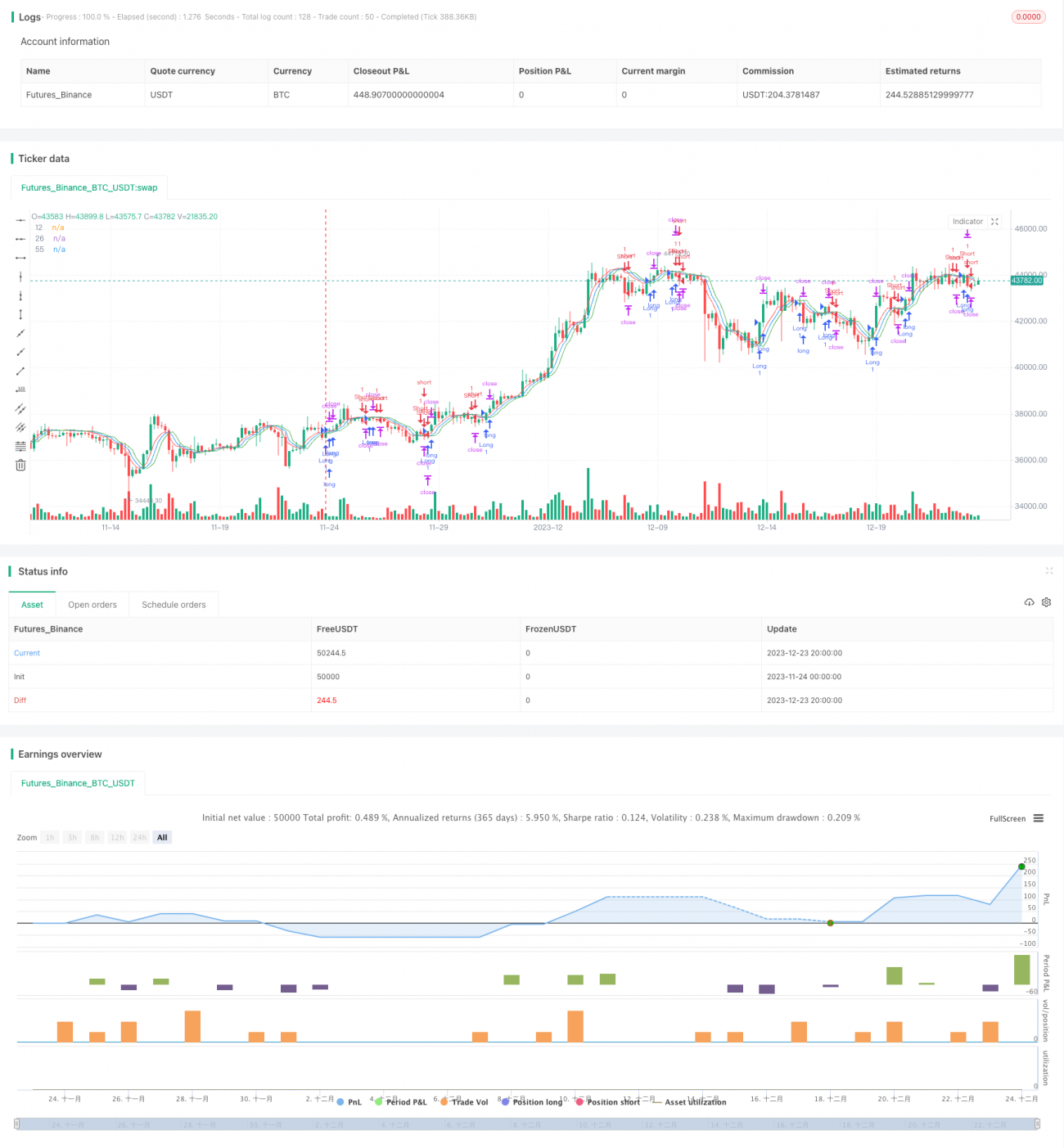

/*backtest

start: 2023-11-24 00:00:00

end: 2023-12-24 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("scalping low lag tema etal", shorttitle="Scalping tema",initial_capital=10000, overlay=true)

mav = input(title="Moving Average Type", defval="temadelay", options=["nkclose", "ema", "emadelay", "fastema", "tema", "temadelay"])

lenb = 3- 1