Dynamic Buying Selling Volume Breakout Strategy

1

Follow

1802

Followers

Overview

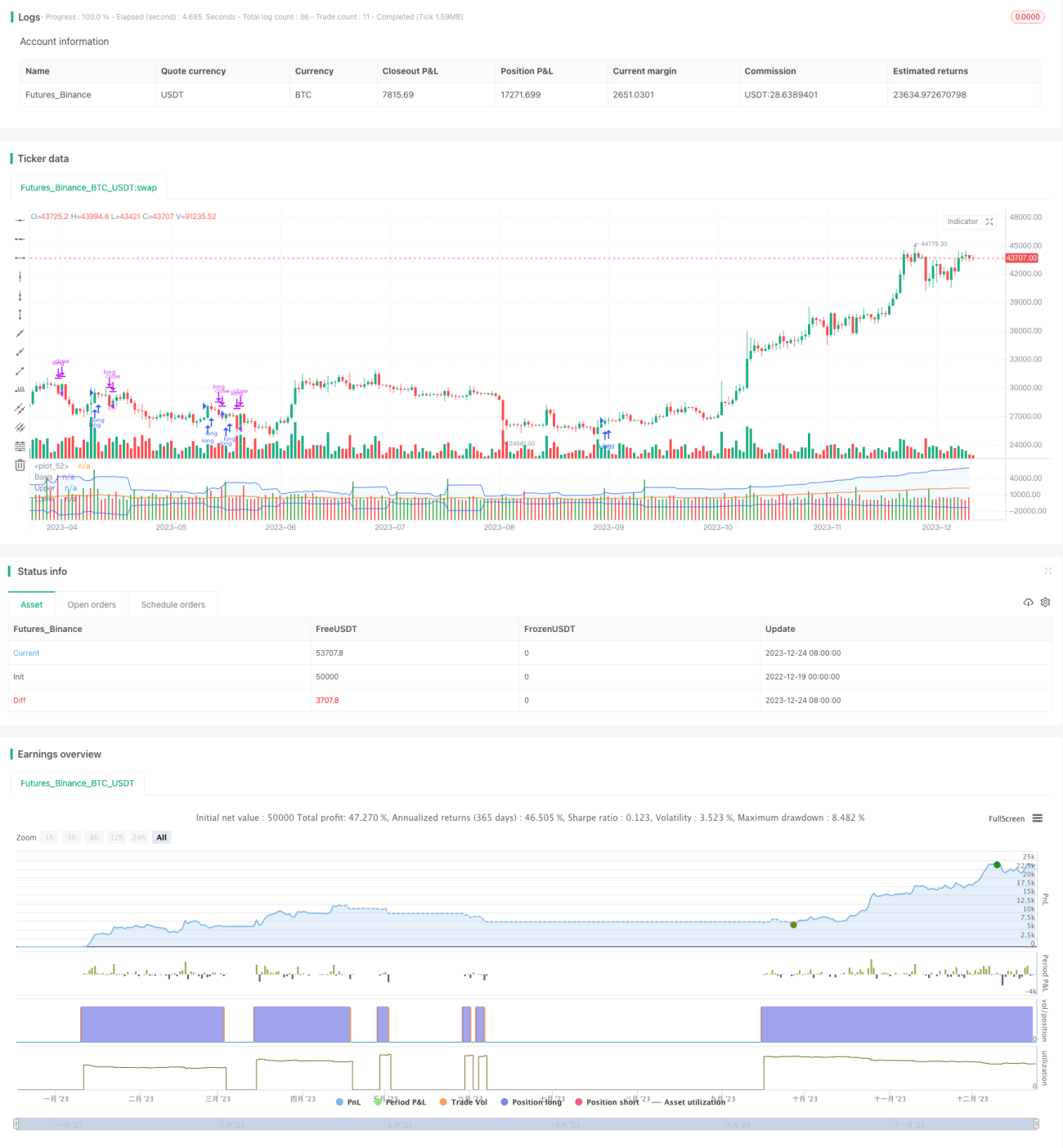

This strategy determines long and short through customized timeframe buying and selling volume, combined with weekly VWAP and Bollinger Bands for filtering, to realize high probability trend tracking. It also introduces dynamic take profit and stop loss mechanism to effectively control one-sided risk.

Strategy Principle

- Calculate buying and selling volume indicators within customized timeframe

- BV: Buying volume, caused by buying at low point

- SV: Selling volume, caused by selling at high point

- Process buying and selling volume

- Smooth by 20-period EMA

- Separate processed buying and selling volume into positive and negative

- Judge indicator direction

- Greater than 0 is bullish, less than 0 is bearish

- Determine divergence combined with weekly VWAP and Bollinger Bands

- Price above VWAP and indicator bullish is long signal

- Price below VWAP and indicator bearish is short signal

- Dynamic take profit and stop loss

- Set percentage of take profit and stop loss based on daily ATR

Advantages

- Buying and selling volume reflects real market momentum, captures potential energy of trends

- Weekly VWAP judges longer timeframe trend direction, Bollinger Bands determine breakout signals

- Dynamic ATR sets take profit and stop loss, maximizes profit locking and avoids overtuning

Risks

- Buying and selling volume data has certain errors, may cause misjudgement

- Single indicator combined judgement tends to generate false signals

- Improper Bollinger Bands parameter settings narrow down valid breakouts

Optimization Directions

- Optimize with multiple timeframe buying and selling volume indicators

- Add trading volume and other auxiliary indicators for filtering

- Dynamically adjust Bollinger Bands parameters to improve breakout efficiency

Conclusion

This strategy makes full use of the predictability of buying and selling volume, generating high probability signals supplemented by VWAP and Bollinger Bands, while effectively controlling risk through dynamic take profit and stop loss. As parameters and rules continue to be optimized, performance is expected to become more significant.

Source

Pine

/*backtest

start: 2022-12-19 00:00:00

end: 2023-12-25 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © original author ceyhun

//@ exlux99 update

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1